Croatia’s economy has experienced robust and resilient GDP growth and improved living standards over the past decade. Yet a rapidly shrinking and ageing population threatens future growth and fiscal sustainability. Advancing pension, health care and labour market reforms will be essential to extend working lives, improve healthy ageing and raise labour force participation.

By Federica De Pace and Oliver Roehn, OECD Economics Department

In the past decade, Croatia’s economy has experienced strong and resilient GDP growth, outpacing OECD and euro area averages. Wide-ranging structural reforms as well as the integration into the EU, euro and Schengen areas all helped boost living standards. However, Croatia’s population is shrinking and ageing rapidly, a combination that bodes ill for future economic growth and public finances. According to UN projections, the working age population will decline by about 25% between 2024 and 2050 (Figure 1). Moreover, for every ten working-age Croatians, there are about four people older than 65 today; by 2050 there will be nearly six. A smaller workforce will drag down growth. According to the OECD Long-Term Economic Model, GDP growth is projected to fall from over 3% per year on average in the last decade to 0.5% by 2050. At the same time, spending on pensions, health care and long-term care will come under increasing pressure.

According to the 2026 Economic Survey of Croatia, addressing demographic challenges requires pension, health care, and labour market reforms to extend working lives, bring more people into the labour force, improve the health of the ageing population, and enhance the efficiency of public spending.

Average pensions of the current generation of pensioners are low, mainly due to short contribution periods. In 2024 the expected duration of working life was just 34.8 years, compared with an EU average of 37.2 years. Short working lives and hence pension contribution periods help explain why relative poverty among older people is nearly twice the OECD average. A recent pension reform aims to increase pension incomes, but comes at a significant fiscal cost. Further tightening early retirement options and increasing the retirement age in line with gains in life expectancy would prolong working lives and help improve pension income without jeopardising the sustainability of the pension system.

Health outcomes also need to improve to enable longer working lives. A higher share of adults aged 65 and over than in most OECD countries report long-standing limitations in their daily activities due to health problems. Improving health outcomes in a cost-effective way requires stronger prevention policies and higher taxes on unhealthy products, more accessible primary care, and higher quality and efficiency of hospital care, including by centralising complex care in specialised facilities.

Population ageing will strain the long-term care system. Today, care relies heavily on informal family caregivers—mainly women—creating significant physical and emotional burdens and limiting their labour-market participation. As care needs grow, this model will become unsustainable. Reforms are needed to expand the formal long-term-care workforce, by improving working conditions and formalising work contracts. Spending on long-term care must rise to improve access and quality of care. Insurance-based models, like those in Germany, Japan, the Netherlands, and Slovenia, can be a solution to ensure adequate funding. Better integration of health and social services would make long-term care more efficient and sustainable.

Bringing younger and older people into the labour force is essential to mitigate the impact of ageing (Figure 2). Stronger work-based learning in vocational education could ease school-to-work transitions. Expanding affordable childcare and formal long-term care would lift employment among women. Among older workers, disability and poor health are major barriers. The employment gap for people with disabilities—36 percentage points in 2024, more than double the EU average—suggests that earlier intervention and broader access to professional rehabilitation are needed. Removing age limits on rehabilitation and linking disability benefits to participation in rehabilitation, would help retain more workers.

Well-designed immigration policy can help ease skills shortages. Croatia has recently seen higher immigration, reversing decades of net emigration, as living standards improved and entry procedures were streamlined. To maximise the gains, however, more efforts are needed to better align migrants’ skills with current and future labour-market needs. Regular assessments and forecasts of skills shortages, more favourable permit conditions for workers in high-demand occupations, and stronger integration services, would improve the country’s ability to attract and retain the workers it needs the most.

Unlocking Peru’s untapped talent by turning education into social mobility

Category: Peru

written by oecdecoscope | March 17, 2026

Peru’s young population is full of potential, but too much of it remains underused. Intergenerational mobility has improved in education but remains weak in incomes. This disconnect explains why a young and increasingly educated population has not translated into stronger productivity growth or broader economic opportunity.

Despite rising educational attainment across generations, weak learning outcomes and school-to-work transitions, widespread informality, and persistent gender gaps limit upward mobility and prevent human capital from being fully used. Addressing these constraints would lift productivity, expand formal employment, and raise Peru’s long-term growth potential. Peru’s young population is full of potential, but too much of it remains underused. Intergenerational mobility has improved in education but remains weak in incomes. This disconnect explains why a young and increasingly educated population has not translated into stronger productivity growth or broader economic opportunity. Despite rising educational attainment across generations, weak learning outcomes and school-to-work transitions, widespread informality, and persistent gender gaps limit upward mobility and prevent human capital from being fully used. Addressing these constraints would lift productivity, expand formal employment, and raise Peru’s long-term growth potential.

Access to education has improved, but outcomes remain weak

Educational attainment has improved substantially across generations. Intergenerational educational mobility, that measures whether children reach higher levels of education than their parents, has increased by 56% between cohorts born in the 1940s and those born in the 1980s (Figure 1). This improvement is larger than in most Latin American peers and reflects sustained expansion of access to school over several decades.

But progress has been uneven. Only 59% of 15–19-year-olds are enrolled in school reflecting high dropout rates, especially in rural areas, where long commutes, financial pressures, and early entry into the labour market pull students out of school.

Progress in education has not translated into similar income mobility. Intergenerational income mobility, that measures whether children earn more than their parents as adults, has risen by only 15%, far less than education mobility, showing that higher education has not led to proportional income gains across generations. Where a child grows up and whether their parents work informally continue to strongly shape earnings prospects in adulthood. Rural residents, women, and children of informal workers remain significantly less likely to surpass their parents’ income, constraining both equity and aggregate growth.

When schooling does not lead to better earnings

Learning outcomes remain weak despite higher enrolment. Peru’s PISA scores are well below the OECD average, placing the country close to the bottom among participating economies. Students from poorer households perform substantially worse than their peers, reflecting gaps in teacher quality, infrastructure, and access to basic services, particularly in rural schools.

Weak learning outcomes contribute to difficult school-to-work transitions. Around one in five young Peruvians is not in employment, education, or training. NEET rates are higher among women, driven in part by early motherhood and limited access to childcare, which restricts labour market attachment at the start of working life.

Even those who do work are often trapped in informal jobs. Over 71% of all workers, and over 85% of young workers, are informal (Figure 2). Informal jobs offer limited training, low wages, and no social protection, reducing incentives for skill accumulation. As a result, informality is frequently transmitted across generations, locking families into low-productivity employment and weakening aggregate productivity growth.

Gender disparities reinforce these dynamics. Women have largely closed education gaps relative to men but still face a 17 percentage point employment gap and earn 19% less on average. Unequal care responsibilities and limited childcare and eldercare services push many women into informal or part-time jobs, lowering lifetime earnings and reducing labour supply.

Policy priorities to boost intergenerational mobility

Unlocking Peru’s full potential requires action on several fronts:

Improve education quality and early foundations. Expanding access for children under three, especially in rural and vulnerable areas, would improve cognitive outcomes and support higher female labour force participation. Strengthening teacher training, enforcing merit-based recruitment, and upgrading rural school infrastructure are essential to close learning gaps and reduce dropout rates.

Strengthen school-to-formal-work transition. Vocational education and training remains underdeveloped. Only 2% of youth are enrolled in VET programmes, far below OECD benchmarks. Expanding VET, improving governance, and aligning curricula with labour market needs would ease entry into formal employment. Second-chance education combined with employment services and targeted social support can help re-engage NEET youth.

Create formal jobs. Improving skills as outlined above would help reduce informality, but a comprehensive agenda combining skills, labour, and business reforms is needed to make formality the norm. Shifting social security contributions away from firm-size thresholds toward progressive labour-income-based contributions would reduce incentives to remain small or informal, especially for low-wage workers. Streamlining labour and business regulations, strengthening enforcement, and improving SME productivity and access to finance would support higher-quality job creation.

Improving intergenerational mobility is a driver of economic growth. When children can reach their full potential regardless of their family background, the country benefits from a larger, better-skilled workforce. By improving education quality, expanding formal jobs, and reducing gender disparities, Peru can turn its young population into the engine of stronger, broadly shared growth.

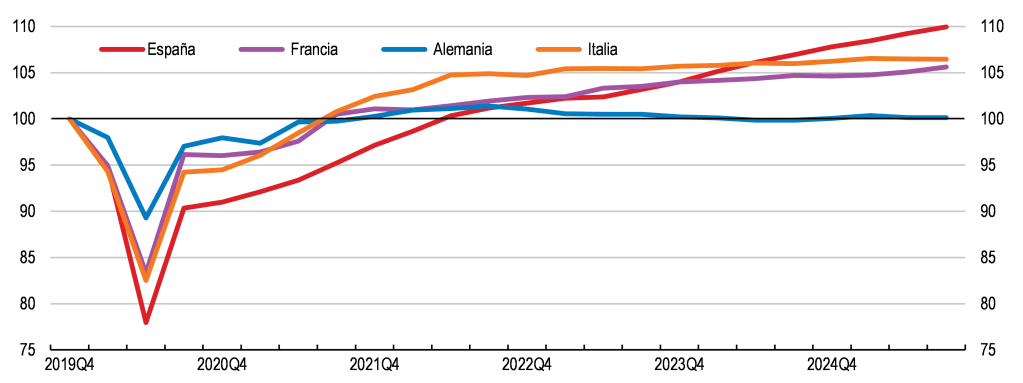

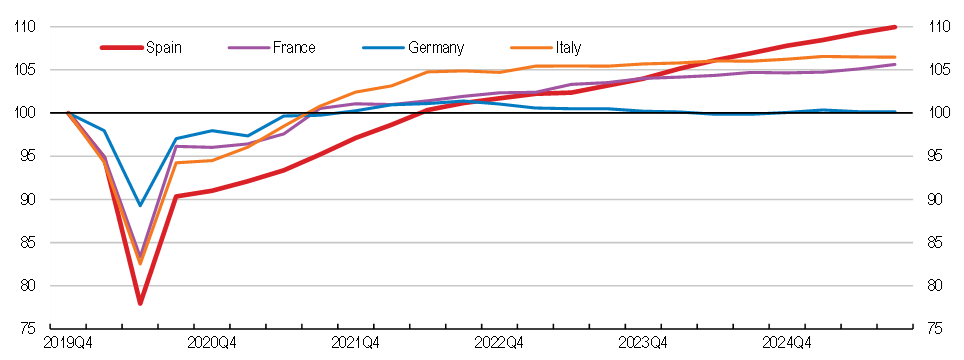

Desde la pandemia, la economía española ha crecido de manera firme y más rápido que muchos de sus pares europeos (Gráfico 1). El crecimiento se ha visto respaldado por una fuerte inversión, principalmente pública, el aumento de las exportaciones de servicios y una rápida expansión de la fuerza laboral ya que muchos inmigrantes, principalmente procedentes de América Latina, se han integrado rápidamente en el mercado laboral. El empleo está creciendo en todos los sectores, mientras que el desempleo ha descendido de alrededor del 15% en 2021 al 10,5% en septiembre de 2025, aunque sigue siendo el más alto de la Unión Europea. Los contratos temporales, que durante mucho tiempo han sido el punto débil de España, han descendido de más del 25% a aproximadamente el 16% en los tres años posteriores a la reforma del mercado laboral de 2021.

Más allá de estos encabezados alentadores, un desafío en materia de productividad amenaza con debilitar la prosperidad a largo plazo de España, como se destaca en el recientemente publicado Estudio Económico de España de 2025. El crecimiento sostenido y la convergencia de los ingresos con otros países similares de la OCDE dependen de la aceleración del crecimiento de la productividad y del aprovechamiento de los recursos sin explotar.

Gráfico 1. El crecimiento del PIB ha superado recientemente al de otros países europeos

Producto interior bruto, volumen, datos ajustados por estacionalidad y efecto calendario, índice 2019T4 = 100

Fuente: Eurostat.

Le reto de la productividad

España está creando empleo a un ritmo más rápido que la mayor parte de Europa, y la productividad por trabajador ha crecido desde 2022, especialmente en los sectores del comercio, el transporte y la hostelería. A pesar de esta mejora, el PIB por hora trabajada en España seguía estando un 7% por debajo de la media de la UE en 2024 (Gráfico 2, Panel A). Este déficit de productividad no se limita a un solo sector rezagado, sino que afecta tanto a las actividades comercializables como a las no comercializables, así como a empresas de todos los tamaños.

El crecimiento del PIB se mantendrá sólido, con un 2,9% en 2025, un 2,2% en 2026 y un 1,8% en 2027, a medida que se normalice la expansión del turismo y se moderen los flujos migratorios. Para mantener este impulso de crecimiento y acelerar la convergencia de los ingresos, será fundamental reforzar el crecimiento de la productividad.

La oportunidad de las pymes

Las pequeñas y medianas empresas son el centro del desafío de productividad de España, y son igual de importantes para superarlo. Las pymes son el 99% de todas las empresas españolas y emplean a casi dos tercios de la fuerza laboral, lo que las coloca en el centro del motor económico del país. Sin embargo, comparado con pares de otros países, las pymes españolas tienden a ser más pequeñas, crecer más lentamente y operan a niveles de productividad significativamente más bajos que los países con mejor rendimiento de la OCDE (Gráfico 2, Panel B). Estas diferencias reflejan las mayores restricciones financieras a las que se enfrentan las pymes, sus menores índices de innovación y las desproporcionadas cargas normativas y de cumplimiento que este grupo de empresas soportan en comparación con las pymes de muchas otras economías europeas.

Consciente de estos retos, España ha puesto en marcha una ambiciosa agenda para las pymes respaldada por el Plan de Recuperación, Transformación y Resiliencia, que destina alrededor del 40% de los fondos en subvenciones al emprendimiento, la digitalización y la internacionalización. Sin embargo, aún se puede hacer más para liberar el potencial de las pymes:

Mejorar el acceso a la financiación mediante el fortalecimiento de los canales de financiación basados en el mercado y la conexión de las pequeñas empresas con los participantes en los mercados de capitales, al tiempo que se sensibiliza a las pequeñas empresas sobre las opciones de financiación no bancaria disponibles.

Simplificar la regulación y los procedimientos administrativos que más afectan a las empresas más pequeñas, incluyendo la introducción gradual de umbrales regulatorios que provocan aumentos repentinos en los costes de cumplimiento cuando las empresas crecen.

Simplificar los procedimientos de solicitud y reembolso de las ayudas públicas a la I+D, entre otras cosas mediante la creación de una plataforma digital única.

Cerrar las brechas de competencias mediante ofertas de formación más accesibles, procedimientos simplificados y una mayor divulgación, de modo que las pymes puedan invertir sistemáticamente en la mejora de las competencias y el reciclaje profesional de su personal.

Cuando se combinan, estas iniciativas pueden ayudar a las empresas más pequeñas a desarrollar todo su potencial. Incluso modestas ganancias de productividad en miles de pymes se traducirían en efectos agregados considerables y una convergencia sostenida de los ingresos.

Gráfico 2. A pesar de mejoras recientes, la productividad laboral se mantiene por debajo del promedio europeo

Nota: En el panel B, los cinco países con mejores resultados para las grandes empresas excluyen a Irlanda y Noruega, donde la productividad laboral supera los 416 000 USD en 2023. Fuente: Estadísticas de niveles de productividad de la OCDE; Estadísticas estructurales de empresas de la OCDE.

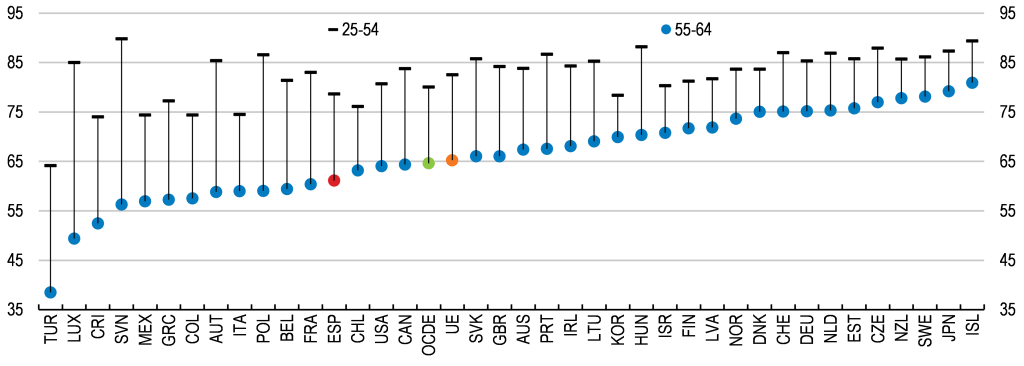

Aprovechar el potencial de trabajadores mayores y migrantes

La urgencia del reto de la productividad en España se hace aún más evidente cuando se tiene en cuenta la demografía. El envejecimiento de la población y las bajas tasas de empleo entre los trabajadores de más edad (Gráfico 3) pueden reducir la oferta de mano de obra, ralentizar el crecimiento potencial y aumentar las presiones fiscales, a pesar de los vientos favorables que ha supuesto el aumento de la migración en los últimos años. España se enfrenta a una de las transiciones demográficas más pronunciadas de la OCDE, con un aumento previsto de la tasa de dependencia de las personas mayores de alrededor de 41 puntos porcentuales entre 2024 y 2054. Sin embargo, estos retos encierran un potencial sin explotar que puede convertirse en beneficio si se adoptan medidas decididas:

Reformar las ayudas por desempleo no contributivas para mayores de 52 años, que actualmente funcionan como una jubilación anticipada de facto. Esto puede abordarse limitando la duración, restringiendo la acumulación de pensiones únicamente a la fase de seguro de desempleo, introduciendo la comprobación de recursos económicos y reforzando los requisitos de activación.

Prolongar la vida laboral alineando más estrechamente los incentivos de jubilación con la mayor esperanza de vida, al tiempo que se mejoran las condiciones de trabajo y las opciones de formación para los trabajadores de más edad, por ejemplo, mediante bonos de formación individuales cofinanciados con los empleadores.

Aprovechar mejor la migración. Los trabajadores nacidos en el extranjero ya representan una gran parte de la creación de empleo reciente, pero muchos están sobrecalificados para sus puestos de trabajo. Simplificar y agilizar el reconocimiento de títulos y hacer que los canales de migración respondan mejor a las necesidades del mercado laboral aumentaría tanto la eficiencia como la equidad.

Gráfico 3. Elevar las tasas de empleo de los trabajadores mayores es crucial para abordar el reto demográfico de España

Tasas de Empleo por edades, %, 2024

Fuente: Estadísticas de la OCDE sobre la población activa.

El resultado final

El crecimiento económico reciente de España ha sido sólido. Para mantener este impulso, es necesario cambiar el enfoque de la creación de empleo al crecimiento sostenido de la productividad. Las prioridades políticas deben seguir empoderando a las pymes mediante una mejor financiación y una menor burocracia, activar a los desempleados de más edad, prolongar la vida laboral y aprovechar el talento de los inmigrantes. España tiene ahora una oportunidad para impulsar las reformas. Las decisiones que se tomen en esta fase determinarán si la resiliencia actual se convierte en la convergencia del futuro.

Since the pandemic, Spain’s economy has grown robustly and faster than most peer countries in the Euro Area (Figure 1). Growth has been supported by strong investment, particularly public investment, rising exports in services and a rapid expansion of the labour force, as many migrants, mainly from Latin America, have integrated quickly into work. Employment is growing across sectors, while unemployment dropped from around 15% in 2021 to 10.5% in September 2025, although it remains the highest in the European Union. Temporary contracts—long Spain’s vulnerability— have fallen from over 25% to roughly 16% in the three years after the 2021 labour market reform.

Beneath these encouraging headlines a productivity challenge threatens to undermine Spain’s long-term prosperity, as highlighted in the recently released 2025 Economic Survey of Spain. Sustained growth and income convergence with other OECD peers depend on accelerating productivity growth and harnessing untapped resources.

Figure 1. GDP growth has surpassed European peers recently

Gross domestic product, volume, seasonally and calendar adjusted data, index 2019Q4 = 100

Source: Eurostat.

The productivity challenge

Spain is creating jobs faster than most of Europe, and productivity per worker has grown since 2022, notably in commerce, transport, and hospitality. Despite this improvement, GDP per hour worked in Spain was still 7% below the EU average in 2024 (Figure 2, Panel A). This productivity shortfall isn’t confined to one lagging sector—it affects tradable and non-tradable activities alike, as well as firms of all sizes.

GDP growth will remain robust at 2.9% in 2025, 2.2% in 2026 and 1.8% in 2027, as the expansion of tourism normalizes, and immigration flows moderate. To sustain this growth momentum, and accelerate income convergence, strengthening productivity growth will be key.

The SME opportunity

Small and medium-sized enterprises lie at the centre of Spain’s productivity challenge, and they are equally central to overcoming it. SMEs make up 99% of all Spanish firms and employ nearly two-thirds of the workforce, placing them at the centre of the country’s economic engine. Yet, compared with their counterparts in peer countries, Spanish SMEs tend to be smaller, grow more slowly, and operate at significantly lower productivity levels than OECD top performers (Figure 2, Panel B). These gaps reflect the tighter financing constraints SMEs face, their lower rates of innovation, and the disproportionate regulatory and compliance burdens they bear relative to SMEs in many other European economies.

Aware of these challenges, Spain has launched an ambitious SME agenda backed by the Recovery, Transformation and Resilience Plan, which allocates about 40% of the funds in grants to entrepreneurship, digitalisation, and internationalisation. Yet, more can be done to unlock SME potential:

Improving access to finance by strengthening market-based funding channels and connecting small firms with capital market participants, while raising awareness among smaller businesses of available non-bank financing options.

Streamlining regulation and administrative procedures costs that weigh heaviest on smaller firms, including phasing-in regulatory thresholds that lead to sudden increases in compliance costs when firms grow.

Simplifying application and reimbursement procedures for R&D public support, including by creating a “one-stop-shop” digital platform.

Closing skills gaps through more accessible training offers, simplified procedures and better outreach so SMEs can systematically invest in workforce upskilling and reskilling.

When combined, these initiatives can help smaller firms realize their full potential. Even modest productivity gains across thousands of SMEs would translate into sizeable aggregate effects and sustained income convergence.

Figure 2. Despite recent improvements, labour productivity remains below EU

Note: In Panel B, 5 best performers for large firms excludes Ireland and Norway where labour productivity exceeds 416,000 USD in 2023. Source: OECD Productivity levels Statistics; OECD Structural Business Statistics.

Harnessing the potential of older workers and migrants

The urgency of Spain’s productivity challenge becomes even clearer when demographics enter the picture. An ageing population and low employment rates among older workers (Figure 3) risk reducing labour supply, slowing potential growth, and increasing fiscal pressures, despite supportive tailwinds from rising migration in recent years. Spain faces one of the steepest demographic transitions in the OECD, with the old-age dependency ratio projected to rise by about 41 percentage points between 2024 and 2054. Yet, within these challenges lies untapped potential that can be turned into gains if bold responses are undertaken:

Reforming non‑contributory unemployment assistance for over‑52s, which currently acts as a de facto early retirement. This can be addressed by limiting duration, restricting pension accrual to the unemployment insurance phase only, introducing means‑testing and strengthening activation requirements.

Extending working lives by aligning pension incentives more closely with longer life expectancy, while improving working‑conditions and training options for older workers—for example via individual training vouchers co‑funded with employers.

Making better use of migration: foreign‑born workers already represent a large share of recent job creation, but many are overqualified for their jobs. Simplifying and speeding up degree recognition and making migration channels more responsive to labour‑market needs would raise both efficiency and equity.

Figure 3. Raising employment at older ages is central to meet Spain’s demographic challenges

Employment rates by age, %, 2024

Source: OECD Labour force statistics.

The bottom line

Spain’s recent economic performance has been strong. Maintaining this momentum requires shifting gears from job creation to sustained productivity growth. Policy priorities should continue to empower SMEs through better finance and less red tape, activate the older unemployed, extend working lives, and unlock migrant talent. Spain now has a window of opportunity to push ahead with reforms. The choices made in this phase will determine whether today’s resilience becomes tomorrow’s convergence.

By Claudia RamírezBulos and Aida Caldera Sánchez, OECD

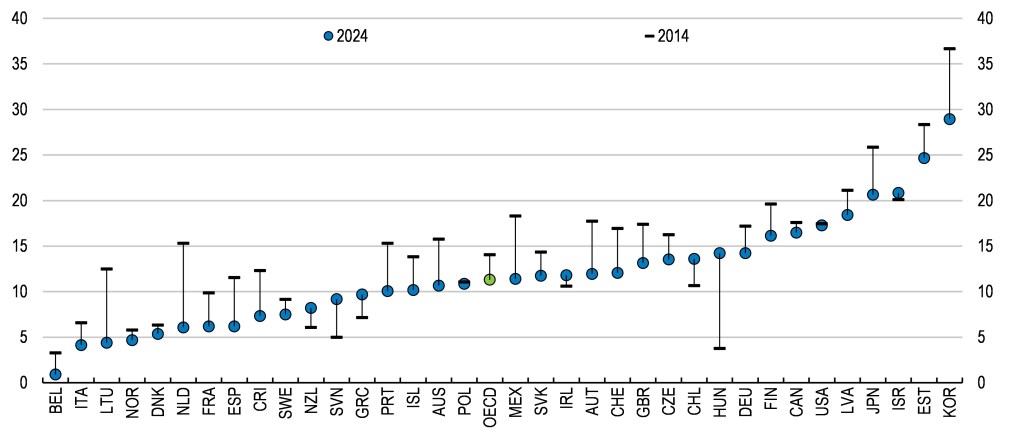

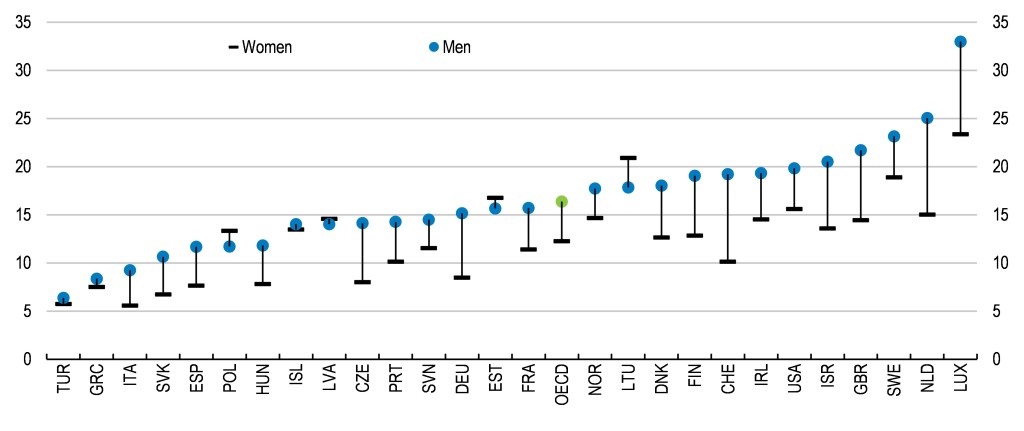

In 2024, a woman working full-time in the average OECD country took home just 89 cents for every dollar earned by a man. But the picture varies significantly by country: in South Korea, women earned 29% less than men, in Japan 22%, while in Italy and Lithuania the difference was closer to 4% (Figure 1). Despite these disparities, one thing is clear: reaching equal pay between men and women is still a pending job across OECD countries.

This picture also emerges clearly in OECD Economic Surveys, which track country-specific progress on gender equality as part of their broader assessment of labour markets and growth. From Germany to Japan, from Korea to Spain, the Surveys show that persistent pay gaps reflect not only individual choices, but structural barriers that limit women’s opportunities to participate fully in the labour market.

Figure 1. The gender wage gap remains large in most OECD countries

Difference in median full-time earnings between men and women, % of the level for men, 2014 and 2024

Note: The data for 2014 refer to 2013 for Chile. The data for 2024 refer to 2023 for Austria, Chile, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Latvia, Netherlands, Poland, Portugal, Slovakia, Slovenia, Spain, the EU-27, and the OECD. The data for 2024 refer to 2022 for Belgium, Iceland, Israel, Switzerland. For Luxembourg the latest data refer to 2020 (0.4); for Türkiye the latest data refer to 2018 (10.0). Source: OECD Gender wage gap statistics.

Why equal pay matter

Equal pay isn’t just about fairness, it’s about unlocking economic potential. Paying women fairly for equal work drives higher workforce participation, fuels economic growth, and helps lift families out of poverty. OECD Economic Surveys consistently underline that more equal labour markets are also more productive. Closing today’s gender pay gap builds tomorrow’s gender pension equity, ensuring women enjoy the same financial security in retirement as men.

What is behind the wage gap between men and women?

The gender wage gap reflects unequal responsibilities and unequal opportunities. OECD analysis shows that three-quarters of the gap comes from men and women with similar qualifications being paid differently within the same firm, often reflecting differences in tasks and responsibilities, or simply discrimination. The remaining quarter reflects the tendency for women to be clustered in lower-paid firms and industries such as care, health and education, while far fewer make it into high-paying, fast-growing fields like information, communications and technology (Figure 2) (OECD, 2021[1]).

In Germany, high marginal tax rates on second earners, often women, discourage full time work (OECD, 2025[2]).

In Japan, the Surveys stress that limited uptake of parental leave by fathers and unequal career progression for women slows efforts to close the gap (OECD, 2025[3]).

In Korea, pay transparency and stronger enforcement of anti-discrimination laws are flagged as priorities to tackle one of the largest gender pay gaps in the OECD (OECD, 2024[4]).

These structural obstacles are compounded by women still bearing a disproportionate share of unpaid household and care work — about four hours a day on average in OECD countries, twice as much as men (Figure 3), leaving less time for paid work, training, or promotions. Also, women’s greater likelihood of working part-time or fewer hours (voluntary and involuntary) limits their experience, career advancement, and access to higher-paying jobs. Hence women not only earn less per hour worked but work less hours on average.

Figure 2. Fewer women work in high-paid jobs than men

ICT specialists and users in their job by gender, % of all jobs, 2022

Source: OECD Going Digital Toolkit gender indicators.

Figure 3. Women assign more time to unpaid household and care work than men

Average time spent by women on unpaid care and domestic work, female to male ratio

Note: “Unpaid care and domestic work” includes routine housework and care for household and non-household members. Source: OECD Time use database 2024.

Progress and policy lessons

The gender pay gap has narrowed by around three percentage points across the OECD in the last decade (Figure 1), thanks to reforms in education, labour market and social policies. OECD Economic Surveys show how tailored policy packages deliver results.

Austria reduced its gap through a mix of measures that strengthened pay transparency and reporting laws, reinforced equal treatment and anti-discrimination legislation, and supported women with mentoring programs and initiatives to balance family and work responsibilities — all while encouraging more women to take on leadership roles.

Spain has also made significant progress, reducing its pay gap by 5.3 points over the past decade. This improvement reflects higher labour market participation, more women moving into full-time roles and higher-paying industries, and the implementation of stronger pay transparency rules to target gender discrimination, which apply to companies with more than 50 employees.

Australia narrowed its gap through expanded parental leave, subsidised childcare, growth of more flexible work arrangements, wage setting reforms and mandatory pay reporting.

These cases illustrate that progress is possible, but also that achieving pay equity requires a comprehensive approach that tackles barriers at home and in the workplace.

The road ahead

A consistent message across OECD Economic Surveys is that progress requires coordinated action on childcare, family leave, tax design, and workplace practices (Gonne and Trincão, 2024[5]):

Expanding affordable childcare, improving shared and flexible parental leave.

Reforming tax and benefit systems to remove disincentives to work for second earners, often women.

Making fair wage-setting practices including mandatory pay transparency policies, requiring employers to publish gender wage gaps and giving workers the right to know what colleagues in comparable roles earn the norm.

Supporting women’s access to leadership and decision-making roles such as temporary quotas, mentorship programs, and women’s networks.

Awareness campaigns and data collection to monitor, evaluate, and improve the effectiveness of policies.

Equal pay will not come automatically. It requires deliberate policy action, sustained monitoring, and a commitment to use all the available talent to strengthen economies and societies.

OECD Economic Surveys will continue to track country-specific progress, helping governments design and implement reforms ensuring that equal pay is not only a principle, but a reality.

References

Gonne, N. and M. Trincão (2024), “Gender mainstreaming in OECD Economic Surveys”, OECD Economics Department Working Papers No. 1831, https://dx.doi.org/10.1787/4d7041d7-en.

OECD (2021), “The Role of Firms in Wage Inequality: Policy Lessons from a Large Scale Cross-Country Study”, https://doi.org/10.1787/7d9b2208-en.

[1]

Overcoming persistent obstacles to growth in South Africa

Category: South Africa

written by oecdecoscope | March 17, 2026

By Nikki Kergozou and Lilas Demmou, OECD.

South Africa, under the Presidency’s Operation Vulindlela, has embarked on bold reforms to address key obstacles to economic growth. Keeping this reform momentum is critical: GDP growth has averaged only 0.7% per year over the past decade. The persistently sluggish pace of GDP growth has failed to significantly raise GDP per capita, expand labour market participation, or improve living standards for the majority of South Africans. The economy’s high emissions intensity presents an additional challenge, as renewed growth may amplify environmental pressures.

The macro-economic policy framework needs to be strengthened to make the economy more resilient.

Transforming the electricity sector to ensure energy security is vital for economic growth and would, in addition, facilitate the green transition.

Greater inclusion of South Africans in the labour market is essential for social cohesion and poverty reduction.

The prospect of higher growth requires speeding up reforms to reduce emissions.

An enhanced macro-economic framework is a prerequisite for stronger sustainable growth. South Africa’s 3-6% inflation target is high and its mid-point is well-above that of other major trading partners. Lowering the inflation target and considering reducing the band around it would help achieve lower inflation and support competitiveness. Public debt has surged from 31.5% of GDP in 2010 to a projected 77% in 2025 (National Treasury, 2025) and rising debt-servicing costs of around 5% are squeezingfiscal space, limiting the government’s capacity to finance social programmes and public investment. Stricter spending controls through reinforced spending rules, and improved governance would help improve the fiscal position and eventually reduce debt. Enhancing the efficiency of tax services, while raising value-added and property taxes, would also contribute to increase revenue collection.

A key structural reform to ensure that growth can be higher in a sustainable way is to ensure that electricity provision is sufficient for businesses to operate. Power outages, or “loadshedding” were estimated to have reduced economic growth by 1.5 percentage points in 2023 (SARB 2024). In addition to directly reducing efficiency, a loss of confidence in the electricity system weakens incentives to invest and deters new market entrants. Significant progress has been made but a lot remains to be done to put electricity outages behind us. Priority should be given to establishing a competitive wholesale electricity market, expanding the transmission grid, and improving municipality’s capacities to deliver electricity effectively. Reforms to municipal management and financing should prioritise earmarking electricity revenues to reduce cross-subsidisation, enhancing property tax collection and exploring distribution concessions.

Many South Africans struggle to find work: the country has the lowest employment rate and the highest unemployment rate among G20 economies. Reforms are needed to help firms create more jobs and to also help workers better connect with job opportunities. Restrictive regulations constrain firms’ ability to enter the market and expand, limiting job creation. Urban sprawl and insufficient public transport lead to lengthy, expensive commutes that pose challenges for workers to connect with employment. Promoting densification, and prioritising housing near public transport and development corridors would help.

As reforms leading to higher growth would put upward pressure on greenhouse gas emissions, South Africa will face additional challenges in meeting its climate goals. In addition, the country is highly vulnerable to the changing climate. A greener economy requires higher carbon prices, an enhanced policy framework for faster implementation of policies, and improved public transport so that people use their cars less often. In parallel, adaptation to climate change needs to be accelerated, notably by reducing the severe under resourcing of municipalities, who have a key role to play in climate policies.

Convertir la incertidumbre global en oportunidad: Una agenda de competitividad para América Latina

Category: Argentina,Brazil,chile,Colombia,Costa Rica,Latin America,Mexico,Peru,Posts in Spanish

written by oecdecoscope | March 17, 2026

Por Jens Arnold, Aida Caldera, Priscilla Fialho, Paula Garda, Alberto González Pandiella, Michael Koelle, Alessandro Maravalle, Dimitris Mavridis, Claudia Ramírez yAdolfo Rodriguez-Vargas, OCDE.

El contexto global, marcado por una alta incertidumbre política y fragmentación, plantea nuevos desafíos para América Latina, pero también abre nuevas oportunidades para fortalecer su competitividad y reducir vulnerabilidades.

Se espera que el PIB en América Latina crecerá 2.1% en 2025 y 2% en 2026, lo que refleja una desaceleración generalizada en la región. Estas cifras son más bajas que las previstas a fines del año pasado y se sitúan por debajo del promedio de otras economías emergentes. Aunque se espera una fuerte recuperación en Argentina, el crecimiento se mantiene débil en la mayoría de los países, con revisiones a la baja para Brasil, México y Colombia (Tabla), en un contexto generalizado de una débil demanda externa y la alta incertidumbre.

Cuadro. Perspectivas económicas para los países de América Latina

Nota: América Latina 7 es la media ponderada por el PIB a valores de paridad del poder de compra de los 7 países en la tabla para el PIB. América Latina 6 es la media simple de los países incluidos en el cuadro para la inflación excluyendo a Argentina. Fuente: OCDE Perspectivas Económicas No. 117, junio de 2025.

La desinflación avanza, pero persisten las presiones inflacionarias. La inflación se mantiene por encima del objetivo en muchos países. En cambio, Argentina ha logrado avances significativos gracias a una combinación de consolidación fiscal y una política monetaria más restrictiva. Con la excepción de Argentina y Brasil, los bancos centrales de la región deberían continuar con su flexibilización monetaria prudente y gradual para asegurarse que la inflación se acerque al objetivo, manteniéndose alerta ante riesgos de salidas de capitales y nuevas presiones inflacionarias.

Los riesgos para las perspectivas son a la baja. Un aumento de los aranceles comerciales y menor dinamismo al previsto en socios comerciales clave podría debilitar aún más las exportaciones y presionar a la baja los precios de las materias primas. Los costos comerciales podrían ralentizar más de lo esperado la desinflación en las economías avanzadas y prolongar tasas de interés globales más altas. Una elevada deuda pública y unas condiciones financieras globales más restrictivas de lo previsto, podrían retrasar la tan necesaria inversión. Si se intensifican las salidas de capital, los bancos centrales podrían tener menos margen de maniobra para flexibilizar la política monetaria.

Una agenda de competitividad para tiempos inciertos

En este complejo entorno global, la región necesita más que nunca mejorar sus políticas domésticas. Un área donde es posible avanzar, y urgentemente necesario, es en competitividad, comercio e inversión. Estas no son prioridades nuevas, pero los cambios globales en el comercio, las cadenas de suministro y la transición hacia economías más sostenibles aumentan su relevancia estratégica. Los países que ofrezcan estabilidad institucional, apertura y baja carga administrativa estarán mejor posicionados para atraer inversión y expandir sus mercados.

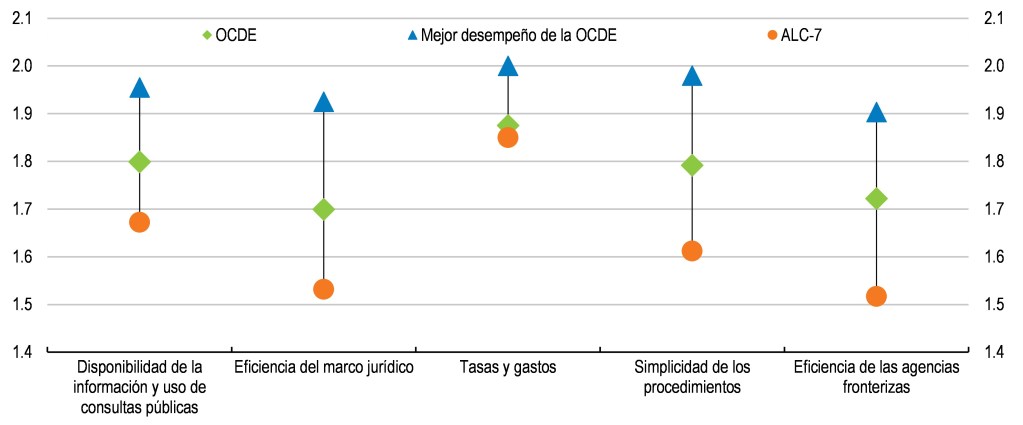

Mejorar los procedimientos aduaneros representa una oportunidad clara. Según los Indicadores de Facilitación del Comercio de la OCDE, América Latina aún enfrenta altos costos comerciales debido a procedimientos aduaneros complejos, inspecciones redundantes y poca coordinación entre agencias fronterizas (Figura). Hay amplio margen para mejorar el procesamiento, levante y despacho de mercancías, en particular mediante una mayor automatización y una mejor coordinación entre las agencias aduaneras, sanitarias, tributarias y otras agencias fronterizas. Medidas prácticas como la cooperación entre agencias de distintos países en la frontera, la agilización de los procesos judiciales y una mayor digitalización pueden beneficiar a los exportadores, especialmente a las pequeñas empresas, y atraer inversión. Además, estas medidas reducen los costos de operar formalmente, lo que incentiva a más empresas a salir de la informalidad.

Figura. Las políticas de facilitación del comercio pueden mejorarse en América Latina

2 = Mejor desempeño

Nota: Disponibilidad de la información y uso de consultas públicas es la media de los indicadores de la facilitación del comercio (TFI, por sus siglas en inglés) A y B. Eficiencia del marco jurídico es la media de los indicadores TFI C y D. Simplicidad de los procedimientos es la media de los indicadores TFI F, G y H. Eficacia de las agencias fronterizas es la media de los indicadores TFI I, J y K. ALC-7 es la media de Argentina, Brasil, Chile, Colombia, Costa Rica, México y Perú. Fuente: Estadísticas sobre los Indicadores de Facilitación del Comercio de la OCDE (TFI, por sus siglas en inglés).

La facilitación del comercio debe ir acompañada de reformas más amplias que fomenten la productividad. Impulsar la competitividad de las exportaciones y la productividad empresarial también requiere un entorno empresarial más dinámico, una mayor competencia doméstica, un mejor acceso a la financiación, más capacitación y capacidad de innovación. Estas reformas se refuerzan mutuamente: las empresas más productivas tienen mayor probabilidad de exportar, invertir y formalizarse.

El fortalecimiento de la integración regional sigue siendo relevante en América Latina, especialmente en un mundo donde las cadenas de valor están cambiando y los centros regionales cobran mayor importancia. El enfoque debe centrarse en la cooperación: mejorar la cooperación entre organismos fronterizos, el reconocimiento mutuo de normas, el intercambio de datos, los sistemas interoperables y el reconocimiento de estándares técnicos comunes. La región también cuenta con un potencial sin explotar en el comercio de servicios, gracias a idiomas compartidos y husos horarios similares; sin embargo, el comercio interregional de servicios sigue siendo bajo en comparación con los estándares mundiales.

América Latina debe adoptar una visión más orientada hacia el exterior. Acuerdos comerciales como el de la UE-Mercosur, y la participación en marcos plurilaterales como la Alianza del Pacífico o el CPTPP pueden ayudar a diversificar mercados de exportación, atraer inversión, fortalecer la participación en las cadenas globales de valor y aprovechar nuevas tecnologías. Sin embargo, para aprovechar al máximo los beneficios de estas iniciativas, los países deben mejorar su capacidad de implementación y garantizar la coherencia entre las políticas comerciales, de inversión y regulatorias.

América Latina cuenta con ventajas reales: vastas reservas de minerales críticos, abundante energía renovable, una fuerza laboral joven y cada vez más cualificada, y proximidad a mercados clave. Al impulsar reformas concretas que mejoren la competitividad, reduzcan las barreras comerciales y atraigan inversión de calidad, la región puede convertir los desafíos actuales en oportunidades y sentar las bases para un crecimiento más sólido y resiliente.

Referencias:

OECD (2025), OECD Economic Outlook, Volume 2025 Issue 1, OECD Publishing, Paris, doi – Reporte completo en inglés con las proyecciones macroeconómicas, los principales desafíos estructurales e información detallada por país.

Extending trade benefits to more firms and workers

Category: Costa Rica

written by oecdecoscope | March 17, 2026

By Aida Caldera, Alberto Gonzalez Pandiella and Alessandro Maravalle

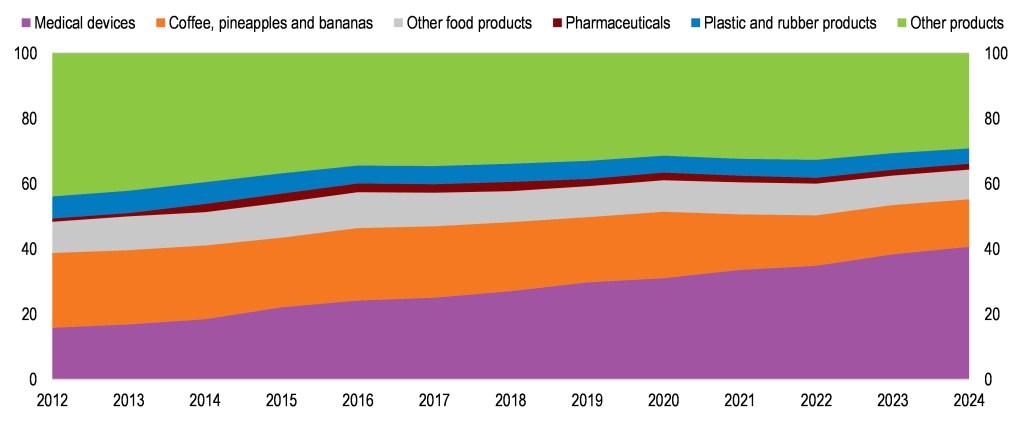

At the beginning of the 1990s, Costa Rica was primarily known for exporting agricultural products like bananas and coffee, along with its thriving tourism sector. Today, places like Alajuela have become global hubs for advanced manufacturing, particularly in the medical devices sector. A strong and sustained commitment with open trade explains this remarkable transformation. Thanks to a more diversified export basket and a shift towards higher value-added goods and services (Figure 1), Costa Rica’s economy has grown more than other OECD countries and regional peers over the last three years and was more resilient to recent shocks. This success story is not without clouds or challenges, as detailed in the 2025 OECD Economic Survey. A long-standing challenge is that not all workers, companies and regions have so far benefited from trade.

Figure 1. High-tech products are a growing share of Costa Rica’s exports

Exports by type of product, % of total good exports

Source: Banco Central de Costa Rica.

Maximising trade benefits

There remain ample opportunities for Costa Rica to capitalize on its trade openness and FDI attractiveness. With Costa Rica’s exports remaining concentrated in a few destinations ongoing efforts to diversity trade agreements and enhance trade facilitation, which have regained considerable impetus since 2022, will facilitate stronger integration into global and regional value chains. Nearshoring offers new opportunities for Costa Rica to extend trade benefits to more workers, firms and regions. However, several barriers might prevent these opportunities from materializing. Continuing the path of reform to enhance education, foster innovation, improve infrastructure and promote stronger competition would help Costa Rica seize maximise trade benefits.

Costa Rica’s well-educated workforce has been traditionally key to attract FDI and develop value added exports. However, now large skills shortages pose a critical threat to Costa Rica’s FDI attractiveness. A comprehensive education reform is underway, but key timelines and milestones are still unclear. The ongoing efforts to reform education should prioritise the increase in the number of technicians and graduates in STEM areas and ensure that university education is better aligned with labour market demands.

Boosting innovation is crucial for Costa Rican firms to access international markets. However, interactions between public universities and businesses are weak, and most innovation funding goes directly to universities without impact evaluations. Competitive performance-based funding is limited, compared to other OECD countries. Strengthening interaction between public universities and businesses, and introducing impact evaluations to innovation funding, would help boost firms’ innovation.

Infrastructure bottlenecks are large, driving up trade costs and limiting the participation of remote regions and SMEs in international trade. Key issues include poor-quality roads and overcrowded ports. The low quality of transport infrastructure can be attributed to underspending, deficient strategic planning and inefficient capital project execution, with only 30% of budgeted capital spending getting executed. Strengthening planning and design of transport projects and enhancing budget management would reduce delays and cost overruns and contribute solve Costa Rica’s large infrastructure gaps.

Finally, boosting competition in domestic markets would help Costa Rican firms access better inputs at lower costs. Despite ongoing efforts to improve competition in some areas, , such as removing anticompetitive practices in professional services and reducing the large and complex stock of regulations, Costa Rica still has some of the strictest regulations in the OECD. Continuing to increase the Competition Authority’s budget is crucial for identifying and addressing anticompetitive practices.

By Falilou Fall, Priscillia Fialho, and Jens Arnold, OECD Economic Department

Brazil’s economy has recovered strongly from the consecutive shocks of the last years says the latest OECD Economic Survey of Brazil. This year, buoyed by good weather and a record-high harvest, the economy is expected to grow at 3%, which is far above its long-term growth trend over the last decade. Unemployment is at its lowest level since 2015, while inflation has returned to the central bank’s target after having risen to almost 12% in mid-2022. Even if in the next years growth will fall short of the exceptional performance of 2023, the current OECD projections of 1.8% in 2024 and 2.0% in 2025 are strong in historical comparison, and are largely driven by expanding domestic demand.

The time has now come to re-focus on the pressing structural challenges that Brazil is facing. These include limited fiscal capacity that hampers necessary investments, weak productivity performance, and the need to end deforestation in the Amazon, after visible increases during 2018-2022.

Building fiscal space will help to focus on policy priorities

With gross public debt exceeding 80% of GDP (Figure 1), rebuilding fiscal buffers is important to ensure that the public sector can undertake the necessary investments in education, social protection and infrastructure in the future. This will require credible deficit targets that guide fiscal policy over the next years. A recently legislated new fiscal framework is expected to become an essential tool in this context, as it combines a clear path for fiscal outcomes with safeguards for public investment, which has all too often fallen victim to fiscal adjustments in the past.

Figure 1. Rebuilding fiscal space is important Evolution of public debt

Source: CEIC; Central Bank of Brazil.

Making the most out of scarce fiscal space will also require more agile budgeting processes. These are currently characterised by widespread revenue earmarking and mandatory spending floors that commit 91% of the budget. This limits the government’s ability to address priority policy challenges.

Further important fiscal reforms are either ongoing or planned. A fundamental overhaul of Brazil’s notoriously complex system of consumption taxes has just been approved by Congress. Moving from a fragmented system of consumption taxes towards a unified value-added tax system will make tax compliance much easier for firms and reduce a number of tax-induced distortions that hold back growth. Beyond consumption taxes, there is scope to reform personal income taxes, including with a view towards making them more progressive.

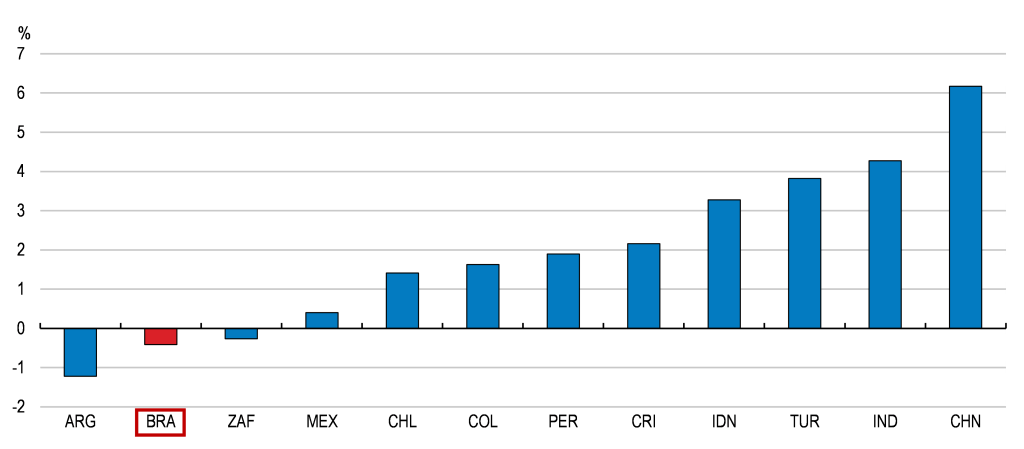

Raising productivity and growth inclusiveness

Productivity has been on a declining trend since 2010, and compared to other emerging market economies, Brazil’s per capita growth has been substantially weaker (Figure 2). This is particularly worrying in light of rapid population ageing. A young population has underpinned economic growth in the past, as more and more people were joining the labour force. Over the next 25 years, however, population ageing is expected to reverse the entire growth dividend that Brazil has reaped from more favourable demographics since the turn of the millenium.

Figure 2. Weak productivity performance and infrastructure competitiveness are impeding stronger growth Average annual GDP per capita growth, 2012-2021

Source: World Bank; and OECD calculations.

Years of insufficient infrastructure investment have given rise to logistics bottlenecks and high transportation costs, which are one factor behind Brazil’s weak productivity performance. But scarce resources are not the only challenge. Improvements in planning and project execution could substantially improve the performance of many infrastructure projects. As a result of challenges in project management, public infrastructure investment has delivered results that have often fallen short of expectations.

Competition, another key driver of productivity growth, has been held back by complex regulations and administrative burdens, some of which shield incumbent firms from potential new market entrants. Recent regulatory reforms have led to improvements in this area, but market entry barriers in services sectors remain above the OECD average. Further regulatory reforms in professional services, including the abolition of exclusive rights for certain ancillary tasks, can stimulate competition in crucial markets. Manufactured goods remain subject to elevated trade barriers, with average import tariffs approximately eight times higher than in Mexico. Lowering these trade barriers can facilitate access to foreign markets and foster a deeper integration into global value chains.

Mobilising currently underutilised labour resources and improving education outcomes is equally essential for sustaining stronger long-term economic growth. Womens’ labour force participation and employment rates lag approximately 20 percentage points behind those of men. The pandemic has exacerbated educational disparities by leaving a stronger mark on children from disadvantaged backgrounds. Prioritising investments in the early years of schooling and expanding access to early childhood education, especially for children from disadvantaged backgrounds, have the potential to reduce gender inequality and equip children with better opportunities later in life.

Making growth more sustainable

Deforestation, the largest contributor to greenhouse gas emissions, has increased since 2018, but policy priorities have changed and early indicators now suggest a decline in 2023. Strengthening enforcement of the Forest Code, coupled with allocating more resources to enforcement agencies, will aid in tackling deforestation. Emissions from agriculture, the second-largest source of greenhouse gas emissions, primarily arise from livestock (Figure 3). Better regulations and stronger incentives for more sustainable production hold significant potential for reducing these emissions. Energy emissions are already fairly low given the significant share of hydroelectric energy sources, but also solar and wind energy, where Brazil’s still untapped potential could turn into a major competitive advantage in the future. The planned introduction of carbon pricing mechanisms will be a milestone in the transition towards a lower-carbon economy.

Figure 3. Deforestation and agriculture are the main sources of greenhouse gas emissions Million tonnes of CO2 equivalent, 2021 or latest

Source: OECD environment database; Estimativas Anuais de Emissões de Gases de Efeito Estuda no Brasil (6ª Edição), Ministério da Ciência, Tecnologia e Inovação; and OECD calculations.

by Laurence Boone, Aida Caldera Sanchez, Nikki Kergozou, Stefano Scarpetta

As some G20 countries are gradually re-opening their economies after a period of strict confinement measures, governments have the opportunity to build back better and make growth more inclusive. The COVID-19 crisis is generating new sources of inequality but also exacerbating the inequalities that existed before the crisis. Already disadvantaged groups, low-paid workers, those in non-standard forms of employment, including those in the informal sector, as well youth and many women have been disproportionally affected by the economic and social shock of the pandemic. These groups have been particularly exposed because of the nature of their jobs and because they suffer from weaker coverage by social protection tools. G20 Governments have acted quickly and boldly to provide immediate support for people and businesses, but building back better involves tackling these inequalities. Our new report prepared for the G20 discusses why these groups are disadvantaged and which levers governments can use to enhance access to opportunities for groups in more urgent need of support, including young people, women, informal and non-standard workers, low-income, low-skilled workers and SMEs (OECD, 2020[1]).

The pandemic is increasing the risk that children and young people struggle to access learning opportunities and potentially do not graduate, while those who do will find it harder to find work experience and jobs. There is a risk that confinement measures compound the inequalities in children’s learning linked to their family’s socio-economic status as parents with higher levels of education and higher income have more opportunities to telework or arrange their work schedules to spend time with their children. In the lead-up to the crisis many young people already struggled to gain a solid foothold in the labour market, with around 19% of 15-29 year-olds not in employment, education or training (NEET) on average across G20 economies (Figure 1). Young people are also often among the most affected during labour market downturns as they generally hold less secure jobs (Figure 2) (OECD, 2020[2]). While the effects of the pandemic on the labour market are just starting, the increase in the youth unemployment rate was almost double that for the entire working-age population. The youth unemployment rate increased from 14.3 to 18.6 percent between February and May across G20 countries for which data is available, compared to an increase from 6.0 to 8.2% for the working-age population1.

The first experiences of young people in the labour market is crucial: youth unemployment can have long-lasting scarring effects in terms of lower pay and higher unemployment (Bell and Blanchflower, 2011[3]; Schmillen and Umkehrer, 2017[4]). After the global financial crisis it took a whole decade, until 2017, before the youth unemployment rate returned to its pre-2008 level (OECD, 2020[2]). We can promote more equal access to opportunities for children and young people by targeting resources to disadvantaged schools and students, investing in high-quality teachers and school leaders and ensuring qualified educational staff and high staff-child ratios. Effective employment and social support, such as job search assistance and counselling, and work experience opportunities are important to help young people in their transition to the labour market. Targeted employment support and screening for barriers to access opportunities can help ensure that all young people, and particularly the most disadvantaged, receive the type and intensity of employment and welfare support that they need. Close collaboration between schools and the public and private employment services can help increase the effectiveness of these services.

Low-income, low-skill workers are being hit hard by the pandemic on multiple fronts. Low-income workers are less able to work from home, are more likely to be working in sectors affected by shutdowns and are more likely to have suffered job or earnings loss. Even in the years leading up to the crisis, low-income, low-skill workers faced the risk of being replaced by digital and automated solutions (Nedelkoska and Quintini, 2018[5]). The crisis has pushed societies even more towards greater online sales and remote working. This push is likely to speed up digitalisation and automation trends, resulting in an even larger change in the demand for skilled jobs over the coming years. Building a sustainable and inclusive recovery means investing in people. Through upskilling and reskilling, especially in digital technologies, we can make digitalisation an enabler rather than competition for these workers. This calls, however, for reducing financial, time and scheduling barriers to participation in adult learning and for making sure that education and training programmes respond to the demand for skills in today’s and future labour markets. Online training offers many opportunities to expand access to adult learning, but low-skill workers may lack the skills to make the most of this kind of training and may need extra support.

The pandemic recession has affected labour market prospects for women more than men so far. Many of the sectors most directly affected by COVID-19 are major employers of women. Even at the onset of the pandemic, women already faced difficulties accessing the same labour market opportunities as men. Women are less likely to participate in the labour market (Figure 3), and those who do work on average in jobs of poorer quality, with lower earnings and a greater incidence of part-time and informal work. These gender differences in employment rates, hours worked and hourly earnings cumulate over people’s lives into a substantial gender gap in labour income. Across advanced G20 countries with available data, this gap ranges from around 30% in Canada to over 70% in Turkey. Outside of their paid job, the COVID-19 crisis likely amplified women’s unpaid workload at home (OECD, 2020[2]). G20 countries have made significant progress to reducing the gender gap in labour force participation but the pandemic has rolled some of this back. Recovery policies need to double down on reducing gender gaps in labour force participation by expanding access to quality formal childcare, reforming paid family-leave policies and strengthening long-term care systems. Further efforts will be needed to reduce the gender gap in earnings and the incidence of low pay among women by fighting gender biases and stereotypes, by attracting more women into careers in science, technology, engineering and mathematics, and by increasing the representation of women in leadership positions.

Informal and non-standard workers, including workers on temporary contracts, in part-time jobs and the self-employed, are particularly exposed to job and income losses in any crisis (OECD, 2020[2]). At the same time, these workers often benefit less, or do not benefit at all, from social protection measures and health coverage. A sizeable share of workers undertake non-standard work (OECD, 2020[6]), while informal workers make up 33 to 91 percent of all workers in emerging G20 economies with available data (Figure 4). The crisis has highlighted the extent of this vulnerability by forcing some non-standard and informal workers to choose between protecting themselves from the virus and having an income. Many countries have recognised this difficult situation and have put in place emergency income support, scaling up means-tested assistance of last resort, introducing new ad-hoc cash transfers and providing direct support for expenses. However, these disadvantages in labour market conditions have structural roots. These workers are often faced with lower job quality and fewer opportunities for training and career development. To ensure a more resilient and inclusive economy and society, we need to help more workers get good quality jobs and benefit from social protection systems. We can do this by encouraging formal job creation, in part by ensuring effective labour market regulation that avoids unnecessarily adding to the cost of formal employment, increasing the perceived benefits of formal employment, keeping labour taxes moderate and strengthening enforcement methods and compliance. We can improve access to training and career development for these workers by making training rights portable between jobs and available to all irrespective of employment status through individual learning schemes.

SMEs are facing dramatic revenue losses and severe liquidity shortages as a result of the pandemic. Small and medium-sized enterprises (SMEs) account for the majority of overall employment and have a considerable impact on employment growth (OECD, 2019[7]; Koirala, 2019[8]). The sudden loss of revenue could translate into insolvency problems and unnecessary bankruptcy for SMEs who in normal times are viable and sound businesses. Building back better also involves creating the right conditions for SMEs to thrive. We can create these by improving access to finance, creating a business-friendly environment that creates an equal playing field across businesses of all sizes, reducing regulatory barriers and supporting women and youth entrepreneurship.

We have a chance to build back better and make growth more inclusive. But to do this, we need to tackle the inequalities that existed well before this pandemic and are now getting worse. Governments have many levers to make this happen. G20 Governments need to keep acting boldly to make sure that the recovery benefits everyone.

References

Bell, D. and D. Blanchflower (2011), “Young people and the Great Recession”, Oxford Review of Economic Policy, Vol. 27/2, pp. 241-267, http://dx.doi.org/10.1093/oxrep/grr011. [3]

Koirala, S. (2019), “SMEs: Key drivers of green and inclusive growth”, OECD Green Growth Papers, No. 2019/03, OECD Publishing, Paris, https://dx.doi.org/10.1787/8a51fc0c-en. [8]

Nedelkoska, L. and G. Quintini (2018), “Automation, skills use and training”, OECD Social, Employment and Migration Working Papers, No. 202, OECD Publishing, Paris, https://dx.doi.org/10.1787/2e2f4eea-en. [5]

Schmillen, A. and M. Umkehrer (2017), “The scars of youth: Effects of early-career unemployment on future unemployment experience”, International Labour Review, Vol. 156/3-4, pp. 465-494, http://dx.doi.org/10.1111/ilr.12079. [4]