Decarbonising the Housing Sector: Pathways to Net-Zero Emissions by 2050

Category: Climate

written by oecdecoscope | March 28, 2023

By Volker Ziemann, OECD Economics Department

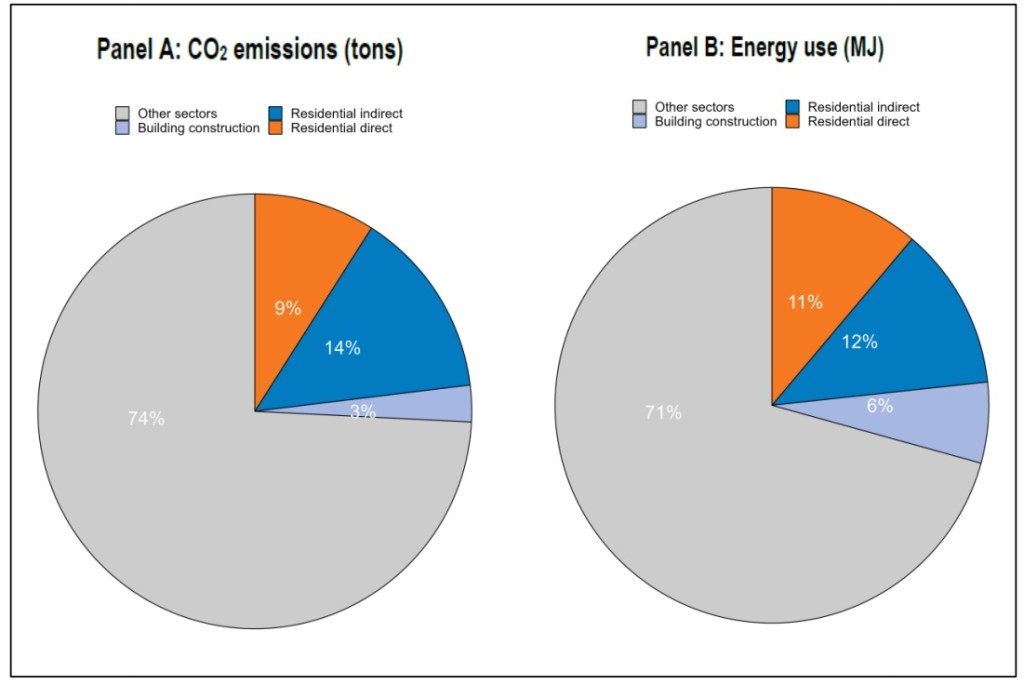

In 2020, over a quarter of total CO2 emissions in the OECD originated in the housing sector. These emissions are generated through space and water heating, cooling, ventilation, lighting, and the use of appliances and other electrical plug loads. Homebuilding is also emission-intensive, accounting for 6% of total CO2 emissions.

Figure 1. Housing accounts for a large share of CO2 emissions

Sectoral decomposition of OECD CO2 emissions and energy use, 2020

Source: Energy Efficiency Indicators (IEA, 2021[7]), Emission Factors database (IEA, 2021[8]), and OECD calculations.

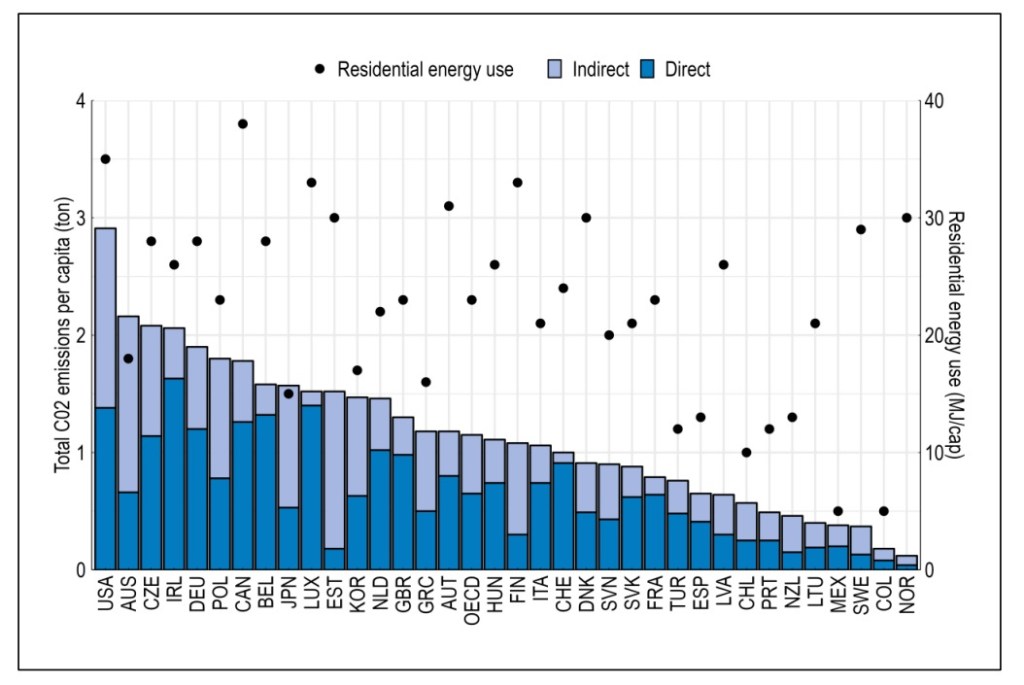

CO2 emission levels vary considerably across countries ranging from nearly three tonnes per capita in the United States to almost zero in Norway. These vast differences indicate that even countries with harsh climates can achieve low emission levels. One of the keys to decarbonising the housing sector is to reduce direct emissions from on-site combustion of fossil fuels such as oil and natural gas for heating and cooking. Electrification and energy efficiency improvements are the primary vehicles to get there. Reducing indirect emissions, those originating from electricity use, then hinges on decarbonising electricity production.

Figure 2. Several countries have high home energy needs, but low CO2 emissions

Total CO2 emissions and energy use of the residential sector, 2020

Source: Energy Efficiency Indicators (IEA, 2021[7]), Emission Factors database (IEA, 2021[8]), and OECD calculations.

Most OECD countries have pledged to reach net-zero emissions by 2050, and some have set even more ambitious targets to achieve this goal earlier. Bringing the housing sector on track to meet these targets requires stepping up efforts and going beyond environmental regulation and encompassing economic, social, innovation, tax, and spending policies.

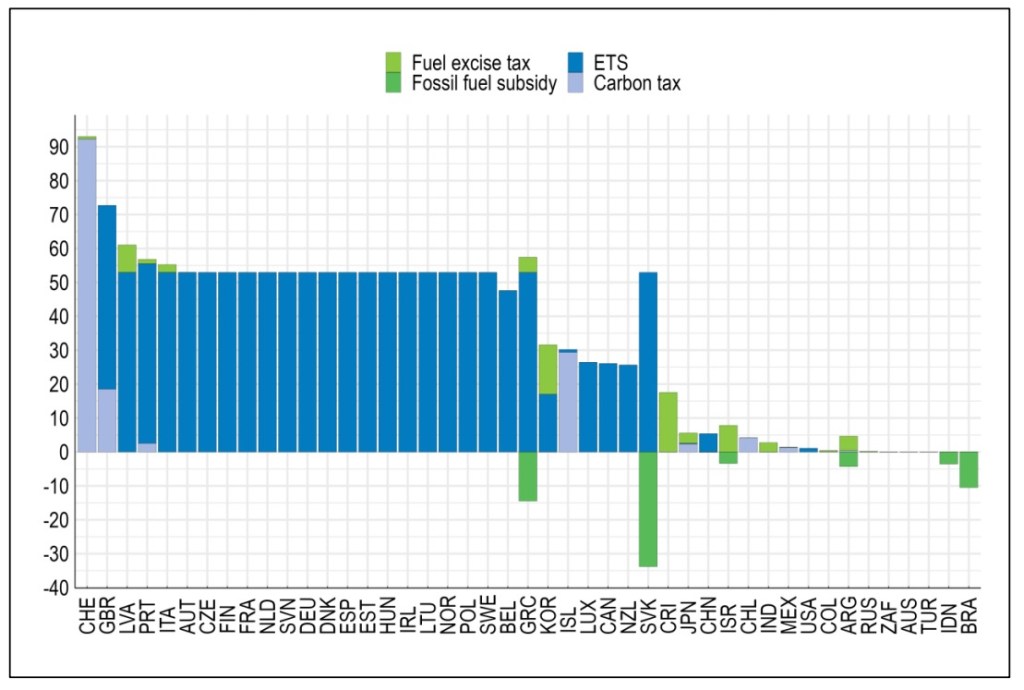

Align carbon prices of energy used in homes with those that apply to other sectors. This can be achieved by explicitly taxing the carbon content of energy sources or by emission trading (applied to energy suppliers).

Figure 3. Effective carbon rates are a long way from being similar across sectors and countries

Ensure carbon-free electricity generation, as a lot of the decarbonisation of homes will have to come from their electrification.

Overcome the split incentive problem between landlords and renters by allowing landlords to recover part of the energy bill saving from energy-efficiency improvements when rent levels are updated.

Extend energy performance certification to all properties, not only those for sale.

Strengthen energy efficiency standards on appliances and new buildings to align with the net-zero emission target.

Offset adverse effects of mitigation measureson vulnerable social groups without blunting incentives to save energy.

Focus on retrofitting the worst existing housing units.

Abolish remaining subsidies for fossil fuel boilers.

Lead the way by building new and retrofitting existing social housing units according to high environmental standards.

Promote greater international comparability and transparency of green building standards to facilitate alignment of green real estate assets with the net-zero target.

Ensure local-level regulations, spending power, and resources are consistent with national decarbonisation goals.

Implemented together, these policy instruments can decarbonise housing at a pace compatible with climate targets and in a way that is consistent with social-inclusion objectives while avoiding unnecessary economic costs.

References:

Hoeller, P. Ziemann, V. , Cournède, B. and M Bétin (2023), “Home, green home: Policies to decarbonise housing “, OECD Economics Department Working Papers, No. 1751, OECD Publishing, Paris, https://doi.org/10.1787/cbda8bad-en.

Securing the health of Ireland’s future

Category: Ireland

written by oecdecoscope | March 28, 2023

By Douglas Sutherland, Patrizio Sicari and Müge Adalet McGowan, OECD Economics Department

In recent decades, Ireland made impressive strides in developing its economy and raising living standards. This progress has allowed it to weather the COVID-19 pandemic and cope effectively with the repercussions from Russia’s war of aggression against Ukraine. Exports from the multinational part of the economy, benefiting from strong demand for medical and information communication technology goods and services, continue to support growth (Figure 1). The domestic economy, while moderating, also remains relatively resilient, despite strong headwinds from high inflation.

Figure 1. Exports continue to support growth

Gross domestic product, volume

1. Excludes those large transactions of foreign corporations that do not have a big impact on the domestic economy. Source: OECD, National Accounts database and Central Statistics Office.

The 2022 OECD Economic Survey shows that the current Irish fiscal situation is favourable, with budget balance expected in 2022, in contrast to many European countries. This is partly driven by high tax revenues, especially corporate tax receipts, which have provided room for government support to households and businesses in the face of rising energy prices. As part of these tax receipts are potentially transitory, there is a need to ensure that expenditure policy is decoupled from windfall tax revenues, rather than facilitating an upward creep of permanent spending.

Two recent measures have improved the fiscal framework. First, EUR 6 billion of the windfall corporate tax gains have been put in the National Reserve Fund in 2022-23. Upside revenue surprises should continue to be saved in this Fund to help prepare for future shocks and long-term fiscal challenges, such as ageing. Second, a spending rule setting an annual cap of 5% on increases in the value of permanent spending (broadly the sum of trend growth of an underlying measure of economic activity assumed to be 3% and the 2% inflation target) over the medium term was introduced in 2021. However, the planned increase in spending to cushion households from high inflation is temporarily pushing outlays above the new rule. Ensuring adherence to the 5% rule as soon as possible will be important to move fiscal policy onto a more stable spending path and enable greater resilience to future shocks.

Ireland faces a number of challenges to sustain growth, improve well-being and ensure fiscal sustainability over the longer term. The 2022 OECD Economic Survey assesses the government’s plans to reform the pension system, overhaul the health system to improve quality of care and value for money, ensure affordable housing and achieve a just carbon transition. As various spending pressures materialise, reforms are needed to ensure debt sustainability. For example, the Irish population is expected to age more rapidly than in most OECD member countries. OECD simulations suggest that public health, including long-term care, and pension costs could rise by 5.7 percentage points of potential GDP by 2060 (Figure 2).

Figure 2. Population ageing will increase pressures on the government budget

Projected change in expenditures from 2021 to 2060

Source: Simulations based on the OECD Economics Department Long-term Model.

The government is investing to boost housing supply and reduce greenhouse gas emissions, but regulatory and legal hurdles should also be tackled to reduce uncertainty and high transaction costs. Planning and permitting delays coupled with judicial review concerning major investments constrain housing supply and slow the development of renewable energy capacity. Increased uncertainty deters investment and raises prices. The availability of construction workers may present an additional constraint on progress, given competing demands from residential construction, including for retrofitting the existing housing stock, and infrastructure projects. In this regard, working to lift supply by increasing the inflow of workers will be important.

The government has initiated a far-reaching overhaul of the health sector, which suffers from legacy issues, such as past underinvestment, centralised decision-making and long waiting lists. The latter, in particular, contributed to a de facto two-tier system, in which buyers of voluntary private health insurance enjoy a faster access to several public hospital services than low-income patients eligible for free care. In this context, Sláintecare reforms will reconfigure the sector by moving away from an expensive largely hospital-based system, which does not offer universal coverage of primary care, towards a better integrated primary, community and long-term care system to enhance access and efficiency. The plans to increase decentralisation, with the creation of Regional Health Areas, and improve data availability and governance as well as financial reporting and management should be prioritised. Effective implementation should remove the burden on expensive hospital care and create the conditions for streamlining the complex interactions between the private and public elements of the system.

Addressing the housing challenges in Central and Eastern Europe

Category: Housing

written by oecdecoscope | March 28, 2023

By Federica De Pace, Francesca Papa and Filippo Cavassini, OECD Economics Department; Willem Adema and Marissa Plouin, OECD Directorate for Employment, Labour and Social Affairs.

The historical development of housing in Central and Eastern European (CEE) countries continues to have implications for the tenure, type, quality and affordability of housing today, calling for policy actions to address a looming affordability challenge.

An ageing and low-quality housing stock

CEE countries record some of the highest homeownership rates in the OECD, with over 70% of households owning their home outright. This is largely due to historical reasons, following the privatisation of state-owned housing in the transition to a market economy in the early 1990s. The formal rental market is generally thin and underdeveloped — only in the Czech Republic is the rental market home to more than 15% of households (19%).

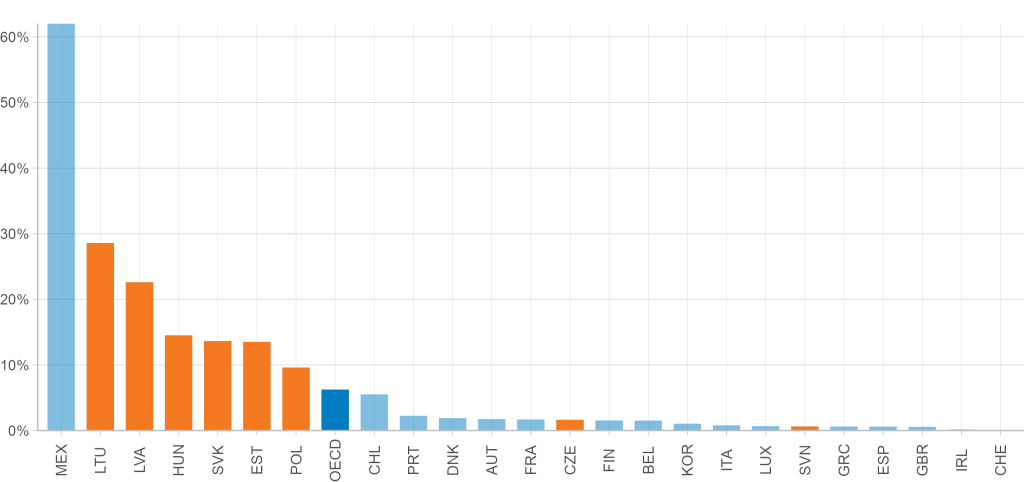

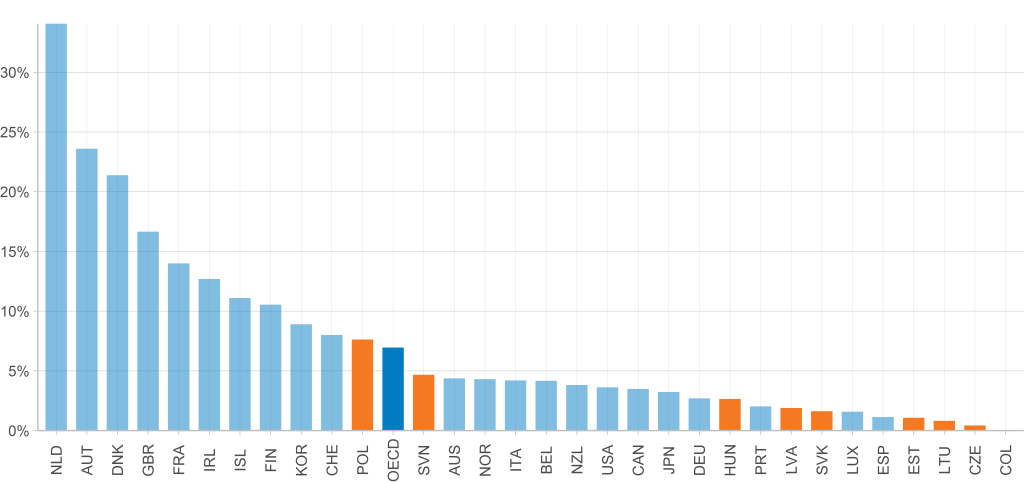

Multi-apartment buildings dominate the housing stock, many built during the communist period. As a result, the stock is ageing and of poor quality. Most households cannot afford to maintain or upgrade their dwellings according to environmental requirements. The share of poor households living in dwellings without access to indoor flushing toilets is well above OECD average in Lithuania, Latvia, Hungary, Slovakia, Estonia and Poland (Figure 1).

Figure 1. The housing stock is of poor quality for many households across the income distribution

Share of poor households1 without an indoor flushing toilet (2019)

1: Households with less than half of the median equivalised disposable income. Source: OECD, Affordable housing database.

A looming affordability issue

Although households in CEE countries spend less on housing than in other OECD countries (OECD Affordable Housing Database), housing prices in CEE have increased substantially over the past decade and faster than the OECD average (Figure 2).

This is not surprising. As in most OECD countries, the strong increase in housing demand in CEE – also fed by the steady increase in average income and abundant mortgage funding prior to the Global Financial Crisis – has not been accompanied by a corresponding increase in housing supply. Housing investment rates in CEE countries have been substantially lower than the OECD average.

Figure 2. Housing prices in CEE have increased substantially over the past decade and at a faster rate than the OECD average

Source: OECD, Analytical house price database.

Affording better quality housing is thus out of reach for many households in CEE countries. For example, an OECD housing affordability review of Latvia shows that 44% of all households – the “missing middle” — are too rich to qualify for social housing or a housing allowance yet too poor to reasonably afford a commercial mortgage (OECD, 2020a).

In parallel, the social housing supply in most CEE countries is well below the OECD average, with the exception of Poland and Slovenia (OECD, 2021). As in most OECD countries, the development of the social housing stock has not kept pace with overall housing construction (Figure 3).

Figure 3. The social housing stock in CEE countries is substantially smaller than the OECD average

Number of social rental dwellings as a share of the total number of dwellings, 2020

Source: OECD Affordable housing database.

What can be done?

OECD countries have taken different approaches to address some of the challenges, from reserving a share of new developments to social housing to tax incentives, among others. Establishing a dedicated funding instrument to boost investment in affordable housing whilst creating the institutional and policy environment to support such investments can be a particularly promising way to address some of the housing challenges in CEE countries.

Boosting sustainable, targeted support for affordable housing

Developing special-purpose funding instruments to channel resources towards affordable and social housing, such as dedicated housing funds, can be an important tool to address the quality, environmental and affordability challenges in CEE countries. Slovakia and Slovenia have already established dedicated housing funds; Latvia is working in this direction. Such funds hold important potential to increase the currently limited housing investment in the region and offer accessible long-term funding needed to bridge affordability and quality gaps (Figure 1 and 2). The OECD 2020 Economic Survey of Lithuania highlighted how the creation of a housing fund could be an effective strategy to improve quality and energy-efficiency of dwellings (OECD, 2020b).

Resources channelled through these funds can leverage public and private funding. In countries where these funds and funding mechanisms have been in place for decades, like Austria and Denmark, funding for social and affordable housing relies on a combination of market loans, guarantees and rental payments. State guarantees help keep borrowing costs low.

The “revolving” element of these funds helps ensure financial sustainability over time, as well as continuous improvements of the housing stock. In Denmark, 2.8% of tenants’ rents contribute to the loan repayment and, once the loan is repaid, are used to finance renovations and improvements. In Austria, tenant equity contributions (about 5-10%) enable low-profit housing associations to generate the surpluses needed to build up equity for future investments, functioning as an internal revolving fund for the associations’ activities. In Latvia, the proposed Housing Affordability Fund will be designed as a revolving fund in which rents paid by tenants are perpetually reinvested in the Fund to finance the construction of affordable rental housing and support upgrades and maintenance.

In Slovakia and Slovenia, the funds directly rely on public funding to construct, repair, and maintain dwellings. In Slovakia, the fund has become financially self-sustained and now relies primarily on the repayments of the loans it provides. The Slovakian State Housing Development Fund has helped support maintenance and refurbishments, responding to the quality gaps common in CEE countries. Half of the refurbished dwellings in Slovakia – a quarter of the overall stock – have been renovated using the Fund.

Creating an enabling environment for better housing quality and affordability

Establishing a fund is an important step – but it isn’t enough. OECD experience shows that funding mechanisms need to be supported by a larger institutional and policy environment – an “eco-system” – in which central and local governments, financial institutions and non-profit housing associations work together for a common purpose. This institutional and policy environment should accompany efforts in CEE countries to bolster sustainable funding for quality, affordable housing.

In Austria, Denmark and the Netherlands, for instance, housing associations have been active in developing and maintaining social and affordable housing. While such actors are less developed in CEE countries, opportunities to further develop such a sector could help meet demands and needs that are currently not met by existing market actors. In Slovakia, not-for-profit organisations are eligible for loans from the State Housing Development Fund. In Slovenia, the Housing Fund co-invests in local community housing programmes, working with municipalities and non-government organisations to meet local needs.

New funding mechanisms to channel investment in housing, bolstered by an enabling institutional environment, can support housing policy development and implementation and act as a catalyst for substantial improvements in housing quality and affordability in CEE countries.

Improving economic opportunities for all in Belgium

Category: Belgium,Housing

written by oecdecoscope | March 28, 2023

By Nicolas Gonne and Müge Adalet McGowan, OECD Economics Department.

Belgium has low income inequality overall, thanks to extensive tax and transfer policies and strong institutionalised social dialogue. However, as in other OECD countries, there is scope to improve equality of opportunities. Indeed, Belgium’s good overall performance regarding income distribution hides an unequal access to life chances, with considerable disparities according to, notably, parental background and country of origin.

Improving economic opportunities for all in Belgium would promote well-being and potential growth by better allocating talents, but also help alleviate fiscal sustainability challenges by reducing the need for redistribution. Based on new OECD evidence from survey microdata (Périlleux et al., forthcoming), the latest Economic Survey of Belgium identifies three key barriers to equal opportunities: low labour market transitions, inequity in compulsory education and a lack of affordable housing. The Survey discusses policies that can tackle these barriers, with a particular focus on the situation of vulnerable groups, such as the low-skilled, people with a migrant background and single mothers. As competencies concerning the labour market, education and housing spread across different levels of government, some recommendations are more relevant to specific regions and communities according to their policy needs and priorities.

Improving the labour market outcomes of vulnerable groups

Important reforms have contributed to increasing the participation of low wage earners and older workers in Belgium. Yet, employment gaps remain particularly large for disadvantaged groups, such as non-EU migrants, the low educated and people with disabilities (Figure 1), in part reflecting weak digital skills and low participation in training. Lifelong learning programmes and actors involved should be streamlined and vulnerable groups prioritised for face-to-face career guidance, as complexity is particularly detrimental to their participation.

Figure 1. Employment gaps are particularly large for disadvantaged groups

Note: Employment gap defined as the difference between the employment rate of prime-age men (aged 25-54) and that of the group, expressed as a percentage of the employment rate of prime-age men (more details). Source: OECD calculations based on OECD Employment database, OECD International Migration database, OECD Education Database and OECD Family database.

The planned introduction of the individual training account, as recommended in the previous Economic Survey of Belgium, is a major step in the direction of increasing lifelong learning efficiency and inclusiveness, but successful implementation requires the provision of high quality training in areas of skill needs and coordination across regions. Moreover, the use of statistical profiling tools for delivering employment services to target vulnerable groups should be expanded. As low employment rates also reflect gaps in individual support for sickness and disability beneficiaries, individual placement and support programmes should be scaled up further, conditional on their evaluation. Finally, introducing in-work benefits for low-wage workers with children would strengthen their work incentives, as low-income single parents and second earners with children face among the highest participation tax rates in the OECD.

Enhancing equal opportunities in compulsory education

Belgian students’ overall academic performance is at par with peer countries. However, student achievement strongly depends on parental background (Figure 2), leading to large disparities across schools and programmes due to a cumulative process of socio-economic self-sorting and academic selection. Schools are incentivised to diversify their student intake, but not to achieve good educational outcomes for weaker students. Reliable performance indicators and other data on successful study progression should be used to inform school funding based on educational improvements made with disadvantaged students. Moreover, schools should be further encouraged to organise programmes across the general and vocational tracks and to enable transfers between them, as low mobility between tracks reduces the prospects of students from disadvantaged backgrounds. Finally, stronger incentives and training for new teachers can reduce attrition and attract teachers to schools with a high concentration of disadvantaged pupils, through strengthening induction programmes and rewarding teaching in disadvantaged schools with financial incentives or improved and stable career prospects.

Figure 2. Student achievement strongly depends on parental background

Note: OECD calculations based on regressions of PISA test scores in reading on the index of economic, social and cultural status (ESCS). Source: OECD (2019), PISA 2018 Results (Volume II): Where All Students Can Succeed, OECD Publishing, Paris.

Promoting affordability and quality on the housing market

In Belgium, housing conditions overall are among the best in the OECD according to the OECD Better Life Index. However, access to affordable housing has become increasingly challenging for low-income households, who bear a high burden from housing costs (Figure 3). The supply of social housing is too low, especially in large cities, such as Brussels, and price differentials with the private housing market hinder moves, thereby distorting work incentives. The regions should expand rental allowances to cover low-income private market tenants, while proceeding to increase the social housing stock.

Figure 3. Low-income households bear a high burden from housing costs

Note: Households on the private rental market; low-income households belong to the bottom income quintile; overburden is more than 40% of disposable income on total housing costs (more details). Source: OECD Affordable Housing database.

Gonne N. (2022), “Improving economic opportunities for all in Belgium”, OECD Economics Department Working Papers, No. 1722, OECD Publishing, Paris, https://doi.org/10.1787/662d50d9-en

Périlleux, G., N. Gonne, S. Cassimon and M. Adalet McGowan (forthcoming), “Upward income mobility and vulnerable households in Belgium: Evidence from survey microdata”, OECD Economics Department Working Papers, OECD Publishing, Paris.

Statistical Insight: Location, location, location – House price developments across and within OECD countries

Category: Housing,Statistical Insights

written by oecdecoscope | March 28, 2023

by Pierre-Alain Pionnier, OECD Statistics and Data Directorate

Housing is key to wellbeing. Real estate typically forms the most important asset of households and their most important source of debt. Not surprisingly given their correlation with the economic cycle, house prices are also one of the most widely tracked economic indicators. However, despite their importance, including for macroeconomic policymaking, as the 2008-09 financial crisis well illustrated, there are few internationally comparable statistics to show how house price developments vary across regions and cities within countries. This is despite the common understanding that changes in house prices within countries are rarely uniform (e.g. there may be ‘ripple’ effects). Policies that target the ‘national’ therefore may miss differences across regions and in turn add to the geography of discontent. This Statistical Insights describes a new OECD database on national and regional house price indices that aims to fill this gap.

There are significant differences in house price developments across countries…

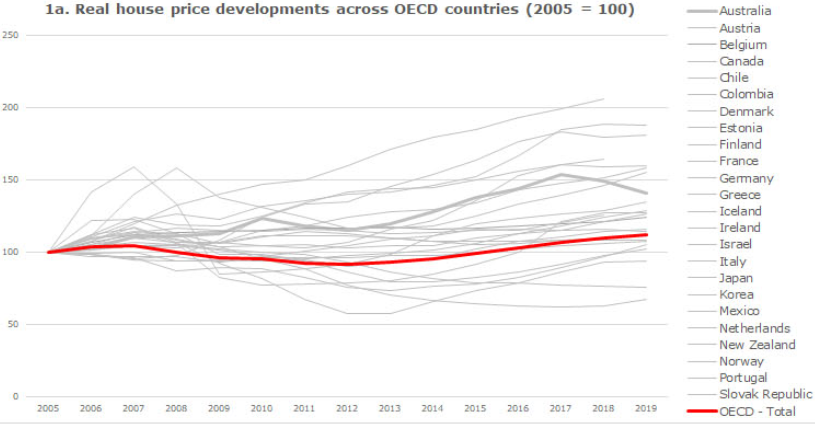

The bursting of the housing bubble in the United States played a key role in the 2008-09 financial crisis, which rapidly turned into a global recession. Even though real house prices (i.e. adjusted for general inflation) declined in several OECD countries, the extent of declines and subsequent ‘recoveries’ differed significantly across countries (Figure 1a). For example, in 2018, house prices in real terms in Colombia were double the levels in 2005, whereas they remained 40% lower in Greece.

This shows that beyond global factors such as those that drove the financial crisis, country-specific factors also matter. These include population growth, land-use restrictions, real household incomes, real interest rates, mortgage market regulations and supervision, lending patterns (at fixed or variable rates), tax relief on mortgage debt financing, and transaction costs such as stamp duty.

… but also within countries.

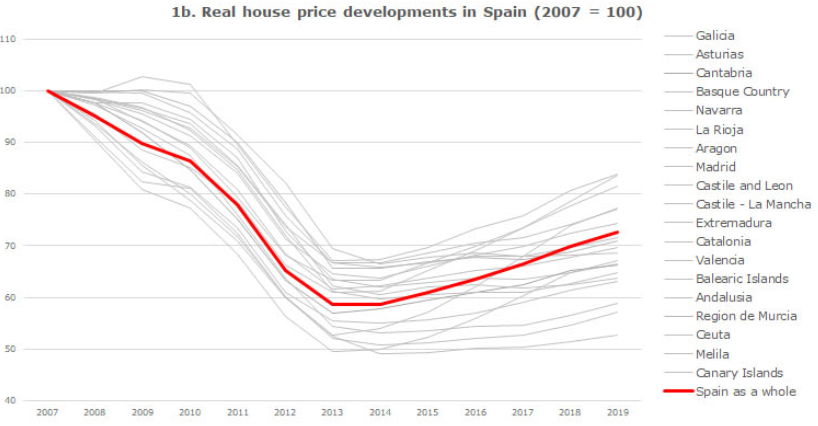

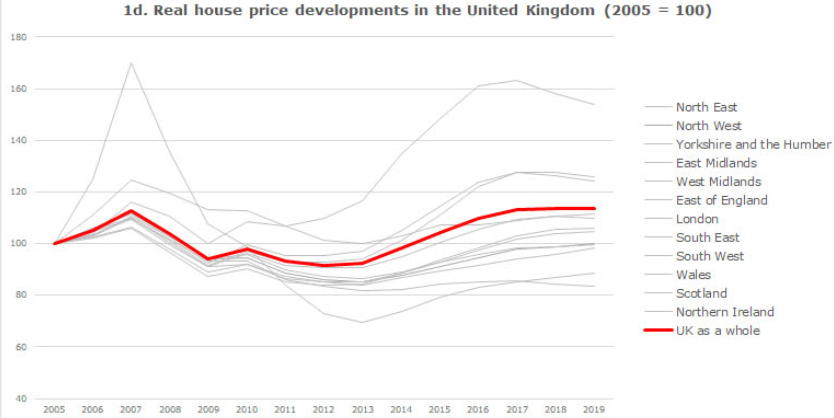

A focus on national price developments does not however tell the full story. Significant differences in the evolution of house prices also exist within countries. For example, while real house prices in Spain declined by 40% on average between 2007 and 2013, and then began to recover, in 2019 they remained nearly 50% lower in Navarra but only 15-20% lower in the Balearic Islands, Ceuta and Melila (Figure 1b). In Mexico, most regions show limited variation around the national average, with real increases ranging from around 10% in the Hidalgo region to around 30% in Yucatan between 2005 and 2018 but this is not universally true. The Federal District for example, which includes Mexico City, saw real prices rise by more than 70% over the same period (Figure 1c). In the UK, Northern Ireland and the region of London show much wider fluctuations in house prices than the rest of the country (Figure 1d).

Figure 1: Real house price developments across OECD countries, and within Spain, Mexico and the United Kingdom

Note: The evolution of real house prices is the difference between the evolution of (nominal) house prices and the evolution of consumer prices (i.e. general inflation). Sources: OECD database on national and regional house price indices, OECD national accounts database.

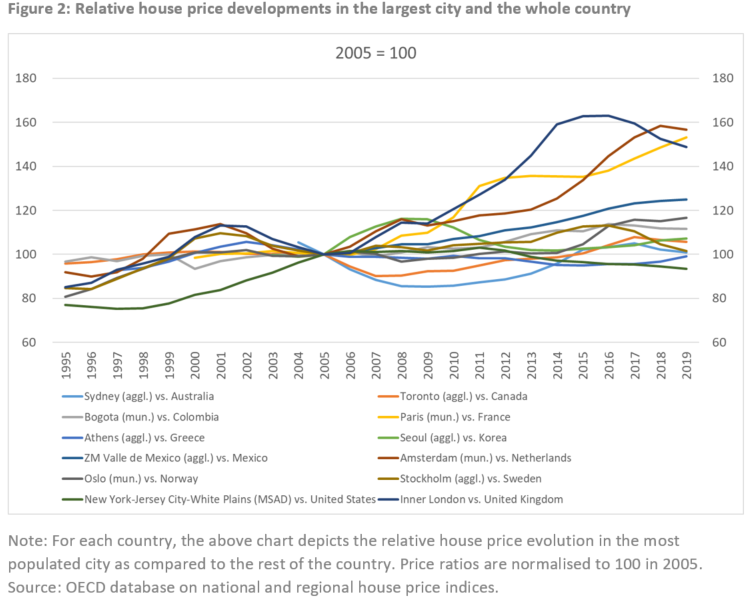

In recent decades, some large cities have seen significant growth in house prices.

In recent decades, an ‘urban resurgence’ (Glaeser 2020), driven in part by better-paid jobs within cities, the willingness to live closer to them, and better access to cultural amenities has led to gentrification and above (national) average house price growth in some of the largest cities. For example, house price inflation in Inner London was around double that of the rest of the United Kingdom between 1995 and 2019. Similarly, house price inflation in Paris between 2005 and 2019 was around 50% higher than in the rest of France (Figure 2).

Nevertheless, this does not exclude large differences across large cities within the same country. For example, the OECD database shows that house prices in the metropolitan area of Los Angeles have grown twice as fast as in the metropolitan area of Chicago since the mid-1990s. Moreover, Glaeser et al. (2012) also emphasise differences in house price developments within cities, with typically faster price growth in recent years in neighbourhoods closer to city centres.

Notwithstanding the fact that economic policy may be suboptimal if one ignores house price heterogeneity within a country, the impact of this heterogeneity on housing affordability may act as a barrier to mobility to households seeking employment in parts of the country where labour demand is higher but cannot always afford to do so due to differences in house prices.

In the years to come, it will be important to assess whether a more systematic use of digital tools to telework following the COVID-19 pandemic will reverse the gentrification of cities and ‘urban resurgence’ phenomena. Granular data on house price developments within countries and cities will become even more relevant for doing so.

The measure explained

House price indices are index numbers measuring the rate at which the prices of residential properties (flats, detached houses, terraced houses, etc.) purchased by households change over time. These indices adjust for quality differences between dwellings sold in the current period, relative to the reference period. In other words, they aim at measuring pure price changes. They cover both new and existing dwellings whenever possible, independently of their final use (to live in or for rent). These prices include the price of the land on which residential buildings are located and they are compiled by official statistical agencies following international statistical standards.

Calculating real house price growth, i.e. controlling for national general inflation, allows for a more meaningful comparison of house price dynamics across countries. The deflator used is the deflator of consumption expenditure of households, compiled according to the 2008 System of National Accounts (SNA). It is important to note that the deflator is typically only available at national level, meaning that the same deflator is used for all regions within a given country, and therefore, that heterogeneity in consumer price dynamics across the different regions of a country is neglected.

Further reading • Glaeser E.L., J.D. Gottlieb and K. Tobio (2012): Housing Booms and City Centers. American Economic Review: Papers and Proceedings, 102(3), pp. 1-10 • Glaeser E.L. (2020): Urbanization and its discontents. NBER Working Paper26839 • ILO, IMF, OECD, UNECE, Eurostat, World Bank (eds.), (2013): Handbook on Residential Property Price Indices • OECD (2020): OECD Territorial Grids

Housing-related policies matter for economic resilience

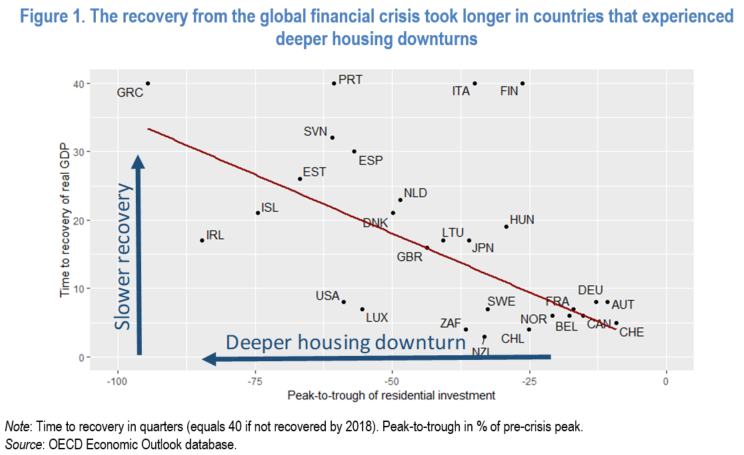

Policies that shape the housing market, such as rules concerning mortgage lending, homebuilding and rental regulation as well as taxation, can have a considerable impact on economic crisis risks and the capacity to recover from a crisis. The reason is that housing market developments strongly influence the business cycle and macroeconomic trends. Changes in house prices, rents and mortgage interest rates prompt variations in household wealth, income and expenditure that often have a sizeable impact on aggregate demand and inflation. Furthermore, house price fluctuations affect residential investment, which is a component of GDP. Countries with sharper declines in residential investment in the aftermath of the global financial crisis generally needed more time to recover from the crisis and regain the pre-crisis level of real GDP (Figure 1).

New OECD empirical studies have probed the transmission of housing-related shocks to the real economy and the role that policy plays in (a) mitigating or amplifying shocks and (b) facilitating or hampering a recovery. The aim is to identify which housing policy-related reforms can foster economic resilience. These studies used a range of econometric techniques, including quantile regressions, probit estimation and propensity-score matching.

The main findings are (Table 1):

Tighter loan-to-value (LTV) caps are associated with a reduced likelihood of severe downturns but also slower recoveries and lower growth. Overall, the evidence confirms earlier results that LTVs seem to entail a trade-off between growth and crisis risk.

More demanding capital requirements also appear to involve the same trade-off, as they are linked with a reduced incidence of downturns but lower median growth. Risk weights that penalise risky mortgages more are tentatively linked with stronger episodes of positive growth, which would be consistent with the hypothesis that they encourage a more efficient allocation of credit.

More stringent rental market regulations are associated with severe downturns that are more likely and more protracted, which may be related to bottlenecks in housing supply and lower labour mobility. On the other hand, tighter rental regulations, which aim to protect tenants against adverse economic shocks, appear to be associated with reduced extreme output losses (measured by GDP-at-risk).

Higher effective taxation of housing is associated with less severe downturns. Moreover, countries with higher taxation experience more moderate house price fluctuations and smoother residential construction cycles.

Taken together, these results mean that, in the management of macroeconomic risks from housing, policies that shape the housing market itself, such as its regulation and taxation, are at least as important as tools to manage the flow of credit. Well-functioning housing markets are therefore important not only to improve housing affordability but also to enhance macroeconomic resilience.

References:

Cournède, B., S. Sakha and V. Ziemann (2019), “Housing Markets and Economic Resilience”, OECD Economics Department Working Papers, OECD Publishing, Paris, https://doi.org/10.1787/aa029083-en.

Are there ways to protect economies against potential future housing busts?

Category: Canada,Germany,Sweden,Uncategorized

written by oecdecoscope | March 28, 2023

by Boris Cournède, Maria Chiara Cavalleri, Volker Ziemann, OECD

Housing, a large and volatile sector, is often at the centre of economic crises, as a trigger or amplifier. The current situation, which is characterised by house prices approaching or exceeding pre-crisis levels in many countries, raises questions as to whether these price levels may be indicative of a possible impending correction and what can be done to reduce housing-related macroeconomic risks.

Figure 1. House price developments since the global financial crisis

The OECD has been developing models that allow assessing to which extent economic trends associated with housing booms, such as steep house price increases or strong debt expansion, can fuel the risk of a severe economic downturn (Turner, Chalaux and Morgavi, 2018). About half of the countries covered by the models are estimated to face real yet limited risks (above 20% but below 30%) of experiencing a severe downturn over the medium term, with housing trends playing a significant role.” Model results suggest that housing booms can fuel crisis risk domestically but also across borders as a consequence of international financial links (Cavalleri, Cournède and Ziemann, 2019).

Countries can reduce housing-related risks in particular by:

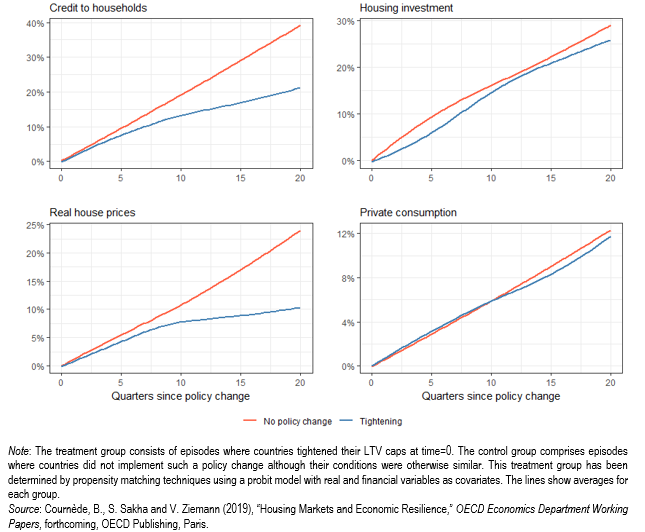

Capping the size of loans relative to house prices. New evidence suggests that such caps are capable of containing house prices and mortgage lending incurring limited economic cost (Figure 2): housing investment is only marginally reduced and there is very little effect on consumption. Tighter loan-to-value ratios are also linked with a lower risk of severe downturns.

Limiting the size of loans relative to income. This measure holds promising potential but has been seldom used so far, which means there is little scope yet to evaluate it ex post.

Tightening bank capital requirements for riskier housing loans. Measures of this nature are linked to more moderate output fluctuations and stronger recoveries after downturns.

Reducing the tax advantages given to housing assets. Higher effective taxation of housing assets (which can come from higher property taxes or lower income tax breaks for housing) favours smoother housing cycles.

Making access to housing more affordable to all in Luxembourg

Category: Luxembourg

written by oecdecoscope | March 28, 2023

by Jan Strasky, Luxembourg Desk, OECD Economics Department

Luxembourg’s economy has been buoyant – robust growth has strongly outpaced the euro area average over most of the past decade. However, this success creates new problems, in particular in the housing market, which the 2019 Economic Survey of Luxembourg [link] analyses in detail. Strong population growth, mainly reflecting the number of foreign workers attracted by a buoyant economy, has kept housing demand growing for many years. When coupled with supply-side restrictions, such as limited use of land available for construction and cumbersome zoning restrictions, the imbalance between demand and supply stokes rising house prices (Figure 1). Increasing mortgage debt also raises the debt service burden for a larger share of households than in other countries and a tight rental market impedes housing affordability for poorer parts of the population.

As the housing stock has not expanded in line with growing

demand for many years, the essential part of the solution is an increase in

construction of new housing. Although the land available for housing

construction seems sufficient, it is mainly in private ownership and many

landowners do not have a strong incentive to sell or develop their land. In

order to reduce the practice of land hoarding, where constructible land is kept

undeveloped to capitalise on continuing land price increases, the opportunity

cost of holding land for construction should be increased. Possible ways of

doing so include introducing land value taxes on land zoned for housing

construction or imposing sanctions on landowners and developers for non-use of

building permits. Higher recurrent taxes on immovable property, based on

up-to-date valuations reflecting the market price of the property, could also

help to incentivise the owners to sell vacant dwellings (Figure 2).

Both municipalities and the central government could improve

the situation in this area. Municipal autonomy in spatial planning decisions is

high and the current framework has not delivered sufficient supply of housing.

Some instruments exist in the law, but are simply not used. This is the case of

an annual tax on constructible land not developed for more than three years,

and also of a tax on unoccupied housing. Other instruments, such as a special

property tax on building land for residential purposes, were introduced more

broadly, but they are based on obsolete cadastral valuations and provide

negligible revenues.

Given the high level of urban sprawl, which has important

environmental costs, new housing construction should aim at increasing

residential density, namely by constructing higher buildings, in particular

around transport hubs. To soften municipal resistance to densification, the

targets on new housing construction agreed between the municipalities and the

central government in the Housing Pact could be extended to include numerical

targets for densification measures or social housing construction. It is clear

that a lot remains to be done by the central government, too. For example, a

reduction of mortgage interest deductibility could help reduce demand for

owner-occupied housing, while financing for new land acquisition by public

providers of social housing would help expand the stock of social rental

housing. Measures reducing demand for owner-occupied housing would also help

reduce the build-up of already high household indebtedness, which creates risks

for poorer households (Figure 3).

The stock of social rental housing is small in international comparison, despite recent efforts by social rental management companies, and often allocated to tenants who are not those most in need. The low stock reflects many factors, including the historical policy of building affordable housing for sale, which could later be re-sold on the private market. This practice has now been phased out and the public housing providers focus on building social housing for rental, rather than for sale. The allocation of social housing also needs to be improved. The admission criteria for social housing are often flexible and with low transparency. Recurrent means-testing should be combined with tailored plans for re-entering the private rental sector, similar to those used by social rental agencies. Housing allowances and rents in the social housing sector could also become more geographically differentiated, reflecting the differences in market rents across municipalities: for example, Luxembourg City has clearly higher market rents than the north of the country.

Boosting economic opportunities and wellbeing in Latvia: why housing matters

Category: Latvia,Uncategorized

written by oecdecoscope | March 28, 2023

by Andrés Fuentes Hutfilter, Germany-Latvia Desk, OECD Economics Department

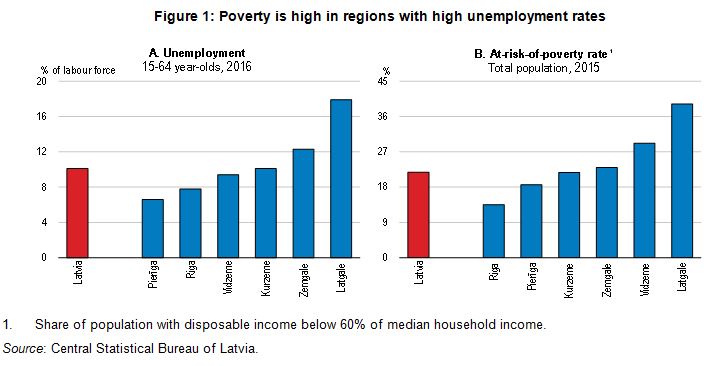

Unemployment is still above 8% in Latvia and contributes to poverty, in part because many unemployed have been without a job for an extended period of time. High unemployment and poverty are concentrated in some regions (Figure 1).

Housing policies shape residential mobility and can encourage workers’ movement to jobs (Andrews et al, 2011). The 2017 Economic Survey of Latvia therefore argues that good housing policies help reduce unemployment in high-unemployment areas. By helping workers find better jobs, they can also boost productivity and wages. Housing policies are particularly relevant for young people since they have a naturally higher propensity to move. Good housing policies could also encourage young people to seek opportunities in Latvia rather than emigrate.

Affordable quality housing is also important for wellbeing. Overcrowded housing is widespread among low- and middle-income households in Latvia. The share of households’ housing spending in total expenditure (26%) is high, and higher than in other countries with similar income level, such as Estonia. Policies are therefore needed to make quality, affordable housing available in neighbourhoods which are well connected to employment opportunities.

Few households rent their homes, even among low-income households (Figure 2). Home owners from high-unemployment areas are likely to find it difficult to afford buying housing in areas with good employment opportunities, where house prices are likely to be higher. There is little development of new housing for rent. Legal uncertainty and long legal procedures hold back the development of the private rented housing market. Reducing tax evasion and fostering long-term lease contracts could also make contracts more reliable and make rented housing more attractive for tenants. Several OECD countries have also successfully expanded affordable housing by requiring private developers to allocate a proportion of the dwellings as affordable units (Salvi del Pero et al., 2016).

Social housing is scarce and waiting lists are long, especially in the Riga area, where unemployment is low and good jobs more abundant. Government spending on social housing and on cash housing benefits for low-income households is low. Support only covers a small share of the low and middle income population. More funding for low-cost rented housing in areas of expanding employment would boost employment and lower poverty. An eligible person can only apply for assistance in the municipality where she resides, limiting labour and residential mobility. A nation-wide register that allowed eligible persons to apply for social housing where they expect better job opportunities could support residential mobility.

New Zealand has recently enjoyed strong economic growth, but housing and population ageing pose challenges

Category: New Zealand,Uncategorized

written by oecdecoscope | March 28, 2023

by David Carey, New Zealand Desk, OECD Economics Department.

New Zealand enjoyed strong economic growth during 2016, driven by high net inward migration, solid construction activity, booming tourism and supportive monetary policy, although in per capita terms growth has been more in line with that in other advanced economies. The terms of trade have rebounded to near record levels, boosting income growth. Growth eased somewhat during the last quarter of 2016 and the first quarter of 2017, in part due to temporary factors including the impact of unfavourable weather conditions on agricultural output and disruption from the November 2016 Kaikōura earthquake. The OECD projects that growth will return to around 3% in 2017‑18, supported by export growth from strong tourism demand and increases in dairy exports. However, slower net immigration is likely to curtail both consumption and residential construction, and the wind-down in the Canterbury earthquake rebuild will curb construction expenditure, more than offsetting the boost from the Kaikōura rebuild and the recently announced increases in infrastructure spending. The unemployment rate is expected to edge down to 4 ½ per cent by the end of 2018 and wage growth to rise moderately. Consumer price inflation should rise sustainably to 2% by the end of 2018, as the effects of oil price falls pass and capacity constraints bite.

While appropriate on the basis of the Reserve Bank of New Zealand’s inflation projections, current monetary policy settings have the downside of fuelling increases in house prices and household debt. As discussed in the accompanying housing blog, both have reached high levels by historical standards and in comparison with most other countries. Further progress is needed to reduce housing supply restrictions, and macro-prudential policy may need to be tightened further, notably by the implementation of debt-to-income limits to reduce financial stability risks.

The government’s prudent approach to fiscal policy puts New Zealand in good stead to cope with future global shocks and natural disasters. Like other countries, New Zealand also faces large spending pressures from public pensions and health-care costs in the longer term. To this end, the government has announced its intention to increase the age of eligibility for the public pension by six months each year from 2037, reaching 67 by 2040. Budget savings would be larger and inter-generational equity greater if this increase were to be brought forward, the transition period lengthened and the pension age subsequently indexed to life expectancy. The planned focus on increasing public-sector productivity should help to contain long-term increases in health-care outlays.

Housing policies shape residential mobility and can encourage workers’ movement to jobs (Andrews et al, 2011). The 2017 Economic Survey of Latvia therefore argues that good housing policies help reduce unemployment in high-unemployment areas. By helping workers find better jobs, they can also boost productivity and wages. Housing policies are particularly relevant for young people since they have a naturally higher propensity to move. Good housing policies could also encourage young people to seek opportunities in Latvia rather than emigrate.

Housing policies shape residential mobility and can encourage workers’ movement to jobs (Andrews et al, 2011). The 2017 Economic Survey of Latvia therefore argues that good housing policies help reduce unemployment in high-unemployment areas. By helping workers find better jobs, they can also boost productivity and wages. Housing policies are particularly relevant for young people since they have a naturally higher propensity to move. Good housing policies could also encourage young people to seek opportunities in Latvia rather than emigrate.