By Boris Cournède, Sahra Sakha and Volker Ziemann

Policies that shape the housing market, such as rules concerning mortgage lending, homebuilding and rental regulation as well as taxation, can have a considerable impact on economic crisis risks and the capacity to recover from a crisis. The reason is that housing market developments strongly influence the business cycle and macroeconomic trends. Changes in house prices, rents and mortgage interest rates prompt variations in household wealth, income and expenditure that often have a sizeable impact on aggregate demand and inflation. Furthermore, house price fluctuations affect residential investment, which is a component of GDP. Countries with sharper declines in residential investment in the aftermath of the global financial crisis generally needed more time to recover from the crisis and regain the pre-crisis level of real GDP (Figure 1).

New OECD empirical studies have probed the transmission of housing-related shocks to the real economy and the role that policy plays in (a) mitigating or amplifying shocks and (b) facilitating or hampering a recovery. The aim is to identify which housing policy-related reforms can foster economic resilience. These studies used a range of econometric techniques, including quantile regressions, probit estimation and propensity-score matching.

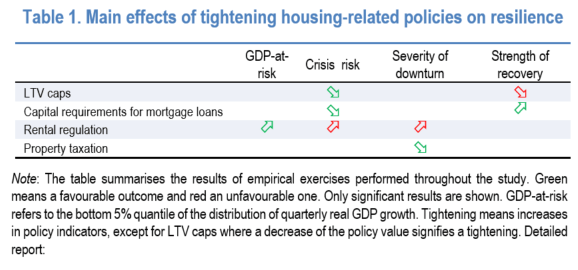

The main findings are (Table 1):

- Tighter loan-to-value (LTV) caps are associated with a reduced likelihood of severe downturns but also slower recoveries and lower growth. Overall, the evidence confirms earlier results that LTVs seem to entail a trade-off between growth and crisis risk.

- More demanding capital requirements also appear to involve the same trade-off, as they are linked with a reduced incidence of downturns but lower median growth. Risk weights that penalise risky mortgages more are tentatively linked with stronger episodes of positive growth, which would be consistent with the hypothesis that they encourage a more efficient allocation of credit.

- More stringent rental market regulations are associated with severe downturns that are more likely and more protracted, which may be related to bottlenecks in housing supply and lower labour mobility. On the other hand, tighter rental regulations, which aim to protect tenants against adverse economic shocks, appear to be associated with reduced extreme output losses (measured by GDP-at-risk).

- Higher effective taxation of housing is associated with less severe downturns. Moreover, countries with higher taxation experience more moderate house price fluctuations and smoother residential construction cycles.

Taken together, these results mean that, in the management of macroeconomic risks from housing, policies that shape the housing market itself, such as its regulation and taxation, are at least as important as tools to manage the flow of credit. Well-functioning housing markets are therefore important not only to improve housing affordability but also to enhance macroeconomic resilience.

References:

Cournède, B., S. Sakha and V. Ziemann (2019), “Housing Markets and Economic Resilience”, OECD Economics Department Working Papers, OECD Publishing, Paris, https://doi.org/10.1787/aa029083-en.

Discover more from ECOSCOPE

Subscribe to get the latest posts sent to your email.