Why Argentina needs a labour market reform

Argentina is going through one of the most comprehensive reform efforts in its history. Since late 2023, the authorities have taken unprecedented measures to reform fiscal, monetary, trade and regulatory policies, all of which have triggered significant improvements in the business environment. For this transformation to translate into new jobs and better living standards, policymakers need to continue reducing institutional and market frictions that impose costs on the reallocation of workers from low- to high-productivity sectors.

By Priscilla Fialho, OECD Economics Department

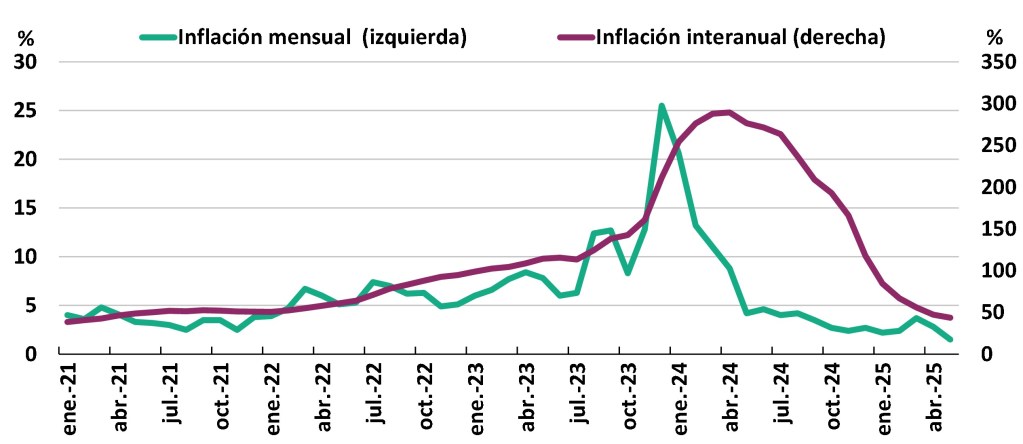

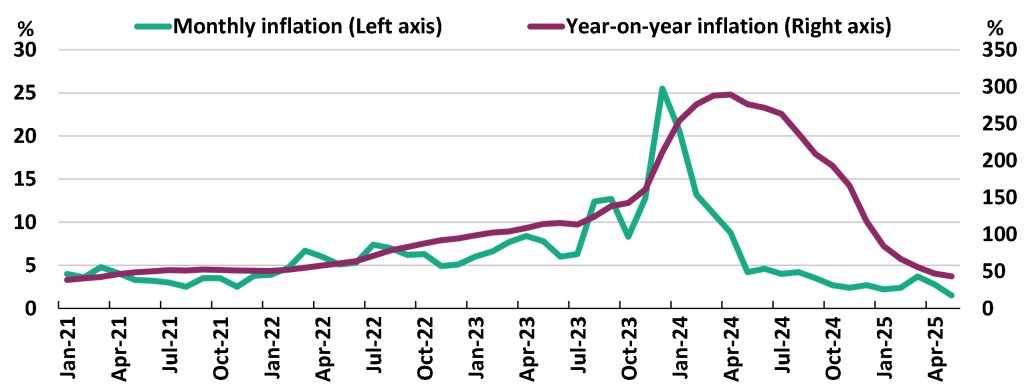

Argentina’s recent reform efforts are bearing fruits, and key macroeconomic indicators have improved significantly. Growth has likely exceeded 5% in 2025 and is projected to remain above 4% in 2026. Annual inflation fell from more than 200% in late 2023 to slightly above 30% in December 2025, and the government achieved a balanced budget for two consecutive years. Despite tighter fiscal policy and domestic financial conditions, labour markets have remained resilient and the poverty rate fell from a peak of 53% in early 2024 to about 32% in the first half of 2025. Following the introduction of a more flexible exchange rate framework in January 2025, foreign reserve accumulation has finally resumed. Markets have responded positively, and the country risk declined to levels consistent with a potential return to international capital markets.

The ambitious reform programme quickly led to improvements in sectors where Argentina has vast comparative advantages. Investments accelerated in the oil and gas and the mining sectors, both of which will help reduce external vulnerabilities in a durable manner. Lower export taxes are encouraging an expansion of agricultural production. More competitive manufacturing sectors are expected to expand at the expense of more traditional ones, thanks to lower prices for imported inputs and capital goods. At the same time, less stringent foreign exchange regulations and the expansion of private credit are supporting financial intermediation and knowledge-based sectors.

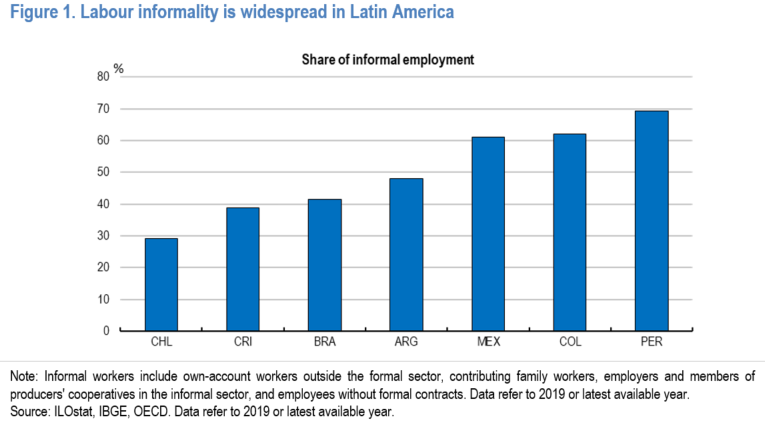

But expanding activity has not always come with sizeable increases in formal employment. Out of 19 sectors, only 6 officially increased their staffing levels in the last two years. Where employment has increased, this was mostly driven by informal jobs, which already account for about half of employment. Widespread informality can limit growth opportunities in the future, as informality often keeps resources trapped in low-productivity activities, discourages on-the-job training and undermines the public sector’s capacity to deliver high-quality public services. More visible improvements in labour market and social outcomes would also bolster public support for further reforms. In a nutshell, one challenge ahead is to ensure that growth translates into higher-quality employment.

Labour market regulations have been historically rigid

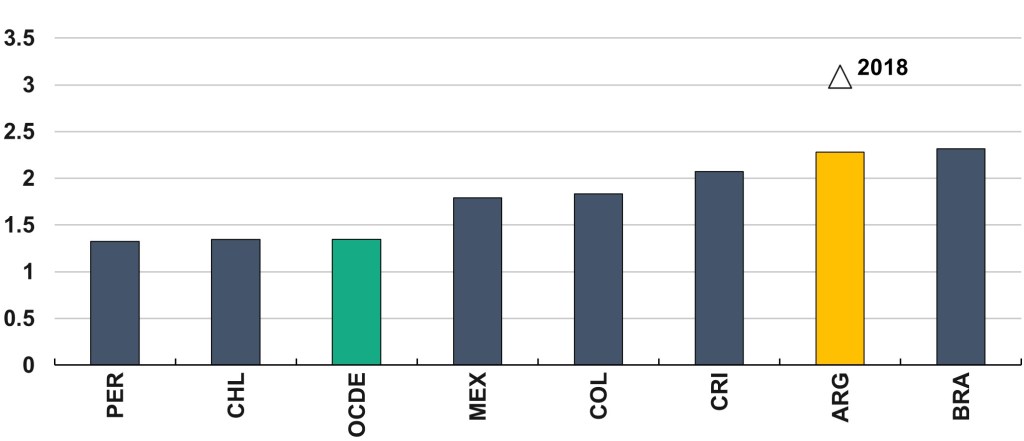

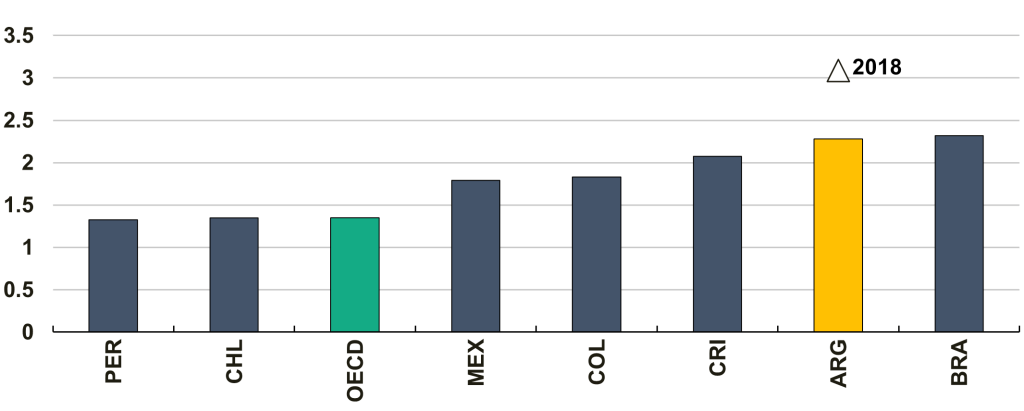

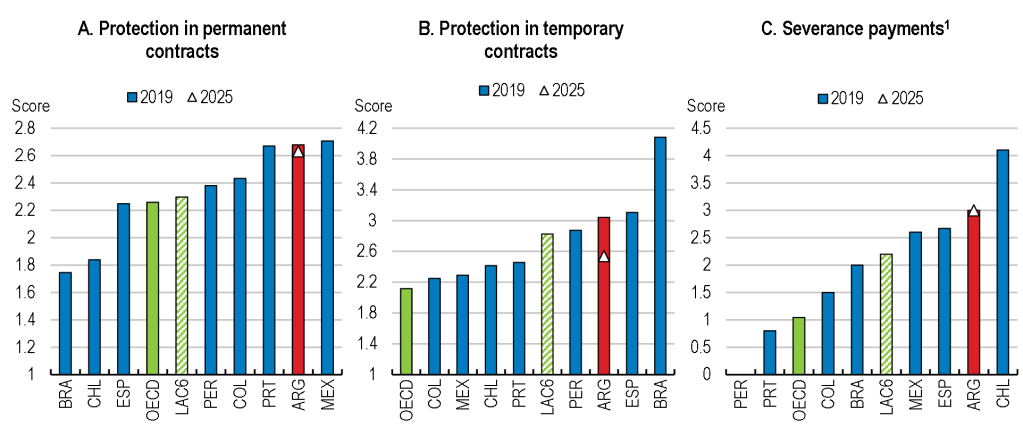

Despite recent improvements, Argentina still has stricter labour market regulations than other countries, based on the OECD Employment Protection Indicators that compare the stringency of hiring and dismissal rules across countries (Figure 1).

Figure 1. Argentina has stricter labour market regulations than peers

Source: OECD Strictness of employment protection.

In Argentina, employers can only dismiss workers in cases explicitly defined by law. This holds both for individual dismissals – where employers wish to separate from individual employees- and to collective dismissals – where firms wish to downsize there workforce. The definition for collective dismissals is exceptionally restrictive in Argentina and the administrative procedure particularly onerous. In addition, court cases can take a long time – on average, between two to four years – and can be filed up until two years after a dismissal, exposing firms to elevated uncertainty and contingent litigation risk. Severance payments, the compensation that firms have to pay in case of dismissal, are also high in international comparison, significantly exceeding those in regional peers. These payments amount to one month of salary for every year of service in most cases, without any cap.

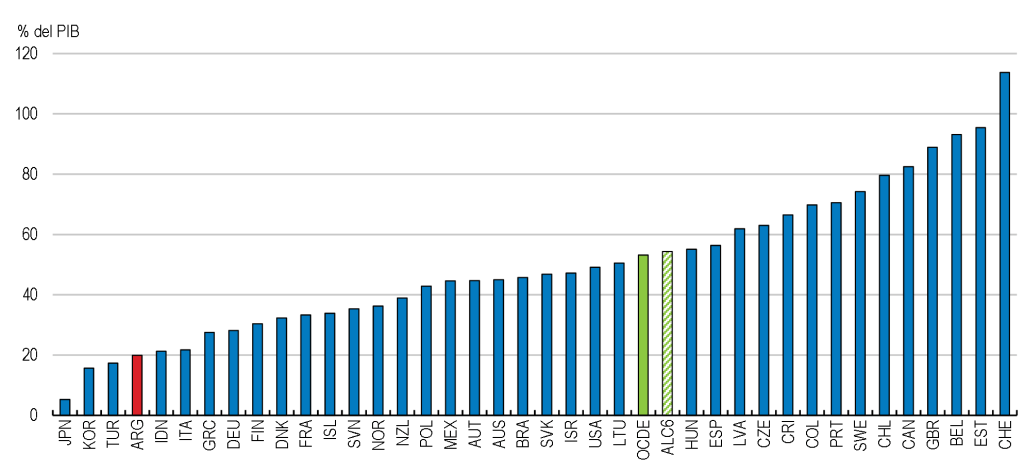

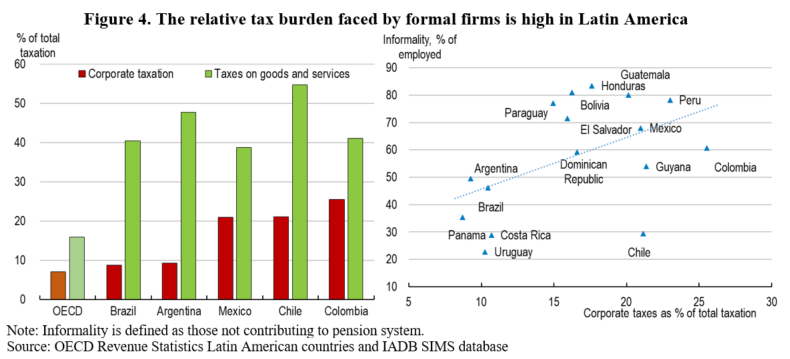

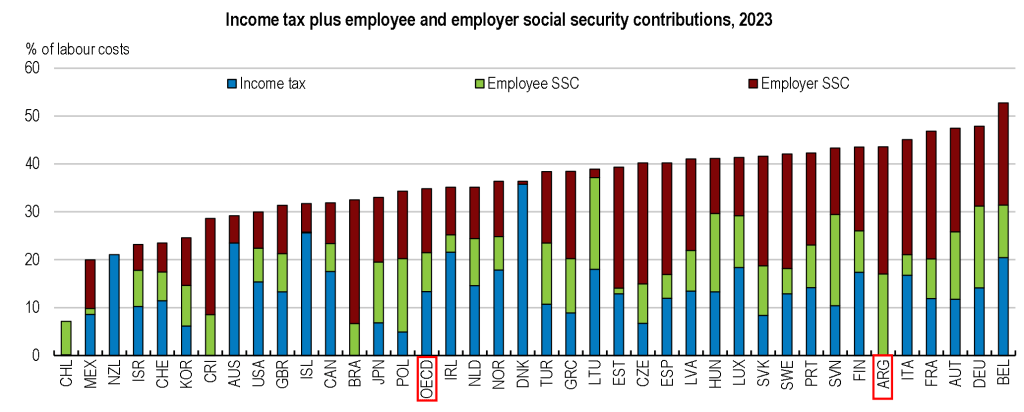

In addition, Argentina has the highest average labour tax wedge in Latin America, above most OECD countries (Figure 2). The labour tax wedge is the difference between what it costs a firm to employ someone and the worker’s take-home pay, which in the case of Argentina can be almost fully attributed to social security contributions. High social contributions discourage demand for and supply of formal labour.

Finally, the collective bargaining system is another source of labour market rigidities. Collective bargaining is organised at the sectoral level, where the labour unions and employer organisations with the highest number of members have the monopoly to bargain on behalf of all firms and employees in the sector. Agreements made between the signatory parties are then automatically extended to the entire sector. Firm-level agreements are strictly regulated by higher-level agreements and cannot apply less favourable terms for employees. Agreements remain valid until a new negotiation takes place, and outdated agreements often last over long periods of time, making it difficult for firms to adapt to changing environments.

Figure 2. The labour tax wedge increases the unit cost of labour

Source: OECD Taxing Wages in Latin America and the Caribbean 2016, OECD Taxing Wages 2024 – Country details, IBGE, OECD Taxing Wages in Selected Partner Economies: Brazil, China, India, Indonesia and South Africa in 2019.

Strict labour market regulations hurt particularly the most vulnerable

An extensive international academic literature suggests that rigid labour market institutions and limited opportunities for job mobility are associated with lower investment, formal employment, productivity and output. First-time jobseekers without relevant experience, older workers who struggle to keep up with new technologies, or less-educated workers, may be particularly affected. Smaller and younger firms may also be at a disadvantage, struggling to compete with large firms that often find it easier to bear the resulting compliance costs.

The last OECD Economic Survey of Argentina provides several policy recommendations to enhance the flexibility of labour market regulations and increase incentives for formal employment. The Survey recommends reducing the amount of severance payment mandated by law. In Chile, for example, severance payments are limited to 330 days of service. The report also encourages the wider application of schemes that provide a voluntary alternative to standard severance payment rules, such as individual worker accounts that can be accessed for income support at the termination of employment, and whose remaining balances can be carried over to new jobs. Moreover, the Survey provides examples of OECD countries that introduced temporary opt-out clauses, allowing the suspension or the firm-level renegotiation of sectoral agreements in cases of economic difficulties. Finally, the Survey discusses options to reduce the labour tax wedge, in particular social contributions, without jeopardising Argentina’s fiscal consolidation efforts. One option would be to unify the current array of available social benefits into a universal multi-pillar system that includes informal workers and provides better incentives for formal job creation. A recent OECD report expands on that discussion, quantifying the estimated fiscal cost of such reforms.

The time for reform is now

Argentina’s Congress is currently debating a labour market reform proposal. The proposal seeks to address some of Argentina’s main challenges:

- More flexible employment protection. The bill aims to reduce uncertainty and contingent litigation risk upon dismissal by clarifying that severance pay is the only compensation that can be claimed upon the termination of an employment contract, thus excluding the possibility of additional civil appeals and indemnities. In addition, it seeks to introduce a voluntary Labour Assistance Fund to cover severance payments from monthly employer contributions of 3% of workers’ remuneration.

- Lower labour tax wedge. Employers adhering to the above-mentioned fund will have a 3% reduction in pension contributions.

- Modernise collective wage negotiations. The draft bill proposes that firm-level agreements can prevail over agreements of a broader scope, whether prior or subsequent. It also intends to limit the automatic extension of clauses once an agreement expires.

Research shows that the timing of labour market reforms matters. Labour market reforms that facilitate the reallocation of workers are much more likely to have positive short-term and long-term effects on employment during economic expansions, and Argentina’s economy is currently growing strong. The timing for a labour market reform could hardly be better.

References

OECD (2025), OECD Economic Surveys: Argentina 2025, OECD Publishing, Paris, https://doi.org/10.1787/27dd6e27-en.