by Thomas Chalaux, Economist, Macroeconomic Analysis Division, OECD Economics Department

There is a recurring controversy, as to the role of global demand pressures in driving domestic inflationary pressures, which matters because such an effect would undermine the control which domestic central banks have in achieving their inflation objectives. Economists from the Bank for International Settlements have presented evidence that global demand pressures, proxied by a measure of the global output gap, are important in explaining inflationary pressure in advanced economies (Borio and Filardo, 2007 and Jasova et al., 2018). On the other hand, other distinguished economists have failed to replicate this result, finding little or no influence of the global output gap on domestic inflation, once other more standard explanations, including domestic unemployment and imported inflation, have been accounted for (Ihrig et al., 2010; Calza, 2008; Gerlach, 2004; Pain et al., 2006; Yellen, 2017; Mikolajun and Lodge, 2016). This blogpost suggests a way in which these apparently contradictory findings can be reconciled and demonstrates that this explanation is borne out with surprising clarity when tested across all OECD economies (for more details see Turner et al., 2019).

The studies that have found important effects from global demand pressures have focused on headline measures of inflation, whereas most of the studies that find contrary results have been explaining ‘core’ inflation, where core inflation typically excludes energy and food prices because they can be very volatile. Global demand pressures might be expected to have stronger effects on energy, food and commodity prices that feed more directly and immediately into headline inflation than core inflation. A simple look at the correlation between the global output gap and aggregate OECD measures of core inflation and of the ‘wedge’ between headline and core inflation, tends to confirm this (Figure 1).

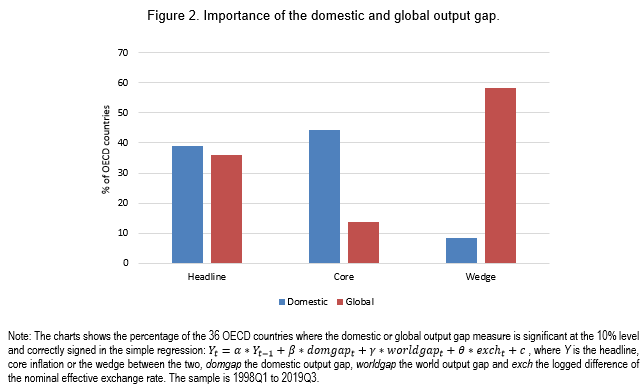

Similar results are found when looking at OECD countries individually: the choice between using the global or the domestic output gap is unclear when explaining headline inflation, while the domestic output gap is clearly favoured when explaining core inflation. Conversely, the global output gap is overwhelmingly preferred when explaining wedge inflation (Figure 2).

The strong relation found between global capacity measures and the wedge between headline and core inflation suggests policymakers should be wary of headline inflation picking up sharply when many countries overheat simultaneously. It might also raise questions as to the appropriate price index to target: if this wedge is strongly influenced by global, rather than domestic, conditions then targeting core might be more attractive than headline inflation because it relates more closely to domestic monetary policy. Moreover, the experience of recent decades suggests that the difference between headline and core inflation can be very persistent and should not be dismissed as short-term noise. On the other hand, excluding important components of the consumer basket from the official target is open to objections about the diminished relevance of a narrower policy objective, less closely related to living standards and so less relevant to agents in the wider economy.

References:

Borio, C. E. V. and A. Filardo (2007), “Globalisation and Inflation: New Cross-Country Evidence on the Global Determinants of Domestic Inflation”, Bank of International Settlements Working Papers, No. 227.

Calza, A. (2008), ´Globalisation, Domestic Inflation and Global Output Gaps: Evidence from the Euro Area, “European Central Bank Working Paper Series, No. 890.

Gerlach, S. (2004), “The Two Pillars of the European Central Bank”, Economic Policy, Vol. 72, No. 3, pp. 707-734.

Ihrig, J., S.B. Kamin, D. Lindner and J. Marquez (2010), “Some Simple Tests of the Globalisation and inflation Hypothesis”, International Finance, 13 (3), pp. 343-375.

Jasova, M., R. Moessner and E. Takáts (2018), “Domestic and Global Output Gaps as Inflation Drivers: What Does the Phillips Curve Tell?”, BIS Working Papers, No. 748, https://www.bis.org/publ/work748.htm.

Mikolajun, I. and D. Lodge (2016), “Advanced Economy Inflation: The Role of Global Factors”, ECB Working Papers, No. 1948, https://ssrn.com/abstract=2831946.

Pain, N., I. Koske and M. Sollie (2006), “Globalisation and Inflation in the OECD Economies”, OECD Economics Department Working Papers, No. 524, OECD Publishing, Paris, https://doi.org/10.1787/18151973.

Turner, D., T. Chalaux, Y. Guillemette and E. Rusticelli (2019), “Insights from OECD Phillips curve equations on recent inflation outcomes,” OECD Economics Department Working Papers 1579, OECD Publishing.

Yellen, J.L. (2017), “Inflation, Uncertainty and Monetary Policy”, remarks at “Prospects for Growth: Reassessing the Fundamentals”, 59th Annual Meeting of the National Association for Business Economics, Cleveland, Ohio, September.

Discover more from ECOSCOPE

Subscribe to get the latest posts sent to your email.