Lithuania: Sailing through rough waters

By Hansjörg Blöchliger, OECD Economics Department

Russia’s war in Ukraine hits a buoyant economy

It was expected to last. Lithuania had been among the fastest growing OECD economies of the past decade, buoyed by rising exports and integration into global value chains. As portrayed in the 2022 OECD Economic Survey of Lithuania, the pandemic-induced recession had been one of the mildest in Europe, and the recovery had been swift. Ambitious public investment in infrastructure, innovation, education, digitalisation, and climate action had paved the way for long-term sustainable growth.

Then Russia started its unprovoked and unjustified aggression against Ukraine. Geographically close, Lithuania soon felt the fallout: trade with Russia collapsed, energy prices soared, and inflation has reached record highs (figure 1). Since it cut all energy ties with Russia, Lithuania relies on natural gas imports through its terminal in Klaipeda and electricity from Poland and the Nordic countries. With commendable generosity, Lithuania has so far given shelter to around 65 000 Ukrainian refugees or more than 2% of its own population.

Growth is projected to decline to 1.6% in 2022 and 1.3% in 2023, against 5% in 2021.

Figure 1. Inflation is record-high

Source: OECD, Consumer Price Indices database.

Fiscal challenges ahead

The government quickly set up a programme to shield households from the full blow of the energy crisis, and fiscal policy has become expansionary. Since the euro area monetary stance is also expansionary, policy is currently fuelling rather than damping inflationary pressures. Against this background, fiscal policy should tighten to reduce demand and to avoid inflation rising further. Fiscal support should focus on the most vulnerable households and on investment in energy security.

Long-term fiscal pressures are looming as well. Lithuania is one of the fastest-ageing countries of the OECD, with the share of people 65 years and older almost doubling until 2060. Additional pension and health care spending could push up public debt to unsustainable levels. Against this background, the government should consider establishing an automatic link between the retirement age and life expectancy, while combating old-age poverty through targeted support for low-income pensioners.

Structural reforms to raise productivity and employment

Productivity growth has accelerated over the past five years, jolted by policy reforms in the past, but it remains below the OECD average (figure 2). To sustain further productivity growth, the government should continue investing in structural reform, particularly in education, digitalisation, and the functioning of public enterprises.

Figure 2. Productivity is accelerating but remains below the OECD average

Source: OECD, Productivity database; OECD, Labour Force Statistics database; and OECD, National Accounts database.

A consolidation of the network of overly small schools and a new teacher framework would help improve quality of compulsory education. Strengthening vocational education and training, in particular expanding apprenticeships, will help reduce structural unemployment.

Modernising the public sector and improving digital skills are important drivers for innovation. More effective support for business R&D and stronger research-business collaboration could boost private investment in digitalisation.

State-owned firms are active in many sectors, and their governance can be improved further. Subjecting all public entities to the same legal, financial, and regulatory possibilities and constraints as private firms is essential to level the playing field.

Setting the priorities right will again lift sustainable growth in Lithuania.

References:

OECD (2022), OECD Economic Surveys: Lithuania 2022, OECD Publishing, Paris, https://doi.org/10.1787/0829329f-en.

Spain continues to recover from the economic crisis with strong growth and falling unemployment, as highlighted in the latest

Spain continues to recover from the economic crisis with strong growth and falling unemployment, as highlighted in the latest

Important challenges remain. Productivity is lower than in other Baltic or central European economies and the gap with leading OECD economies remains large (chart A). Yet, productivity growth has slowed after the financial crisis, as elsewhere. To converge to the living standards of high income countries, Latvia has to reinvigorate productivity. As the

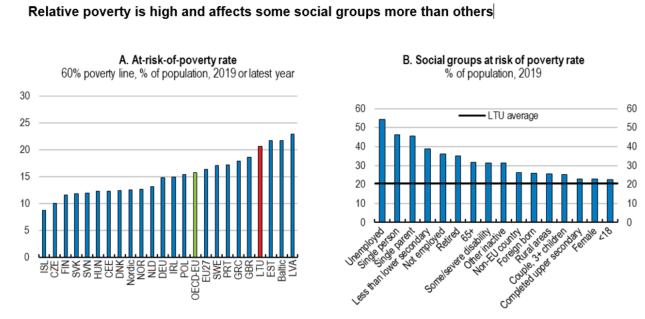

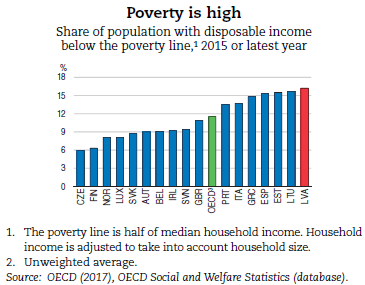

Important challenges remain. Productivity is lower than in other Baltic or central European economies and the gap with leading OECD economies remains large (chart A). Yet, productivity growth has slowed after the financial crisis, as elsewhere. To converge to the living standards of high income countries, Latvia has to reinvigorate productivity. As the  Poverty is among the highest in OECD countries (chart B) and is concentrated in some regions in part reflecting high unemployment. Lack of access to good and affordable housing makes it more difficult for low-income workers to move to well-paying jobs. Access to health services and higher education are also uneven and limit access to economic opportunities for low income households. Many young Latvians emigrate. These issues and policies to address them are analysed in the

Poverty is among the highest in OECD countries (chart B) and is concentrated in some regions in part reflecting high unemployment. Lack of access to good and affordable housing makes it more difficult for low-income workers to move to well-paying jobs. Access to health services and higher education are also uneven and limit access to economic opportunities for low income households. Many young Latvians emigrate. These issues and policies to address them are analysed in the