Statistical Insight: Location, location, location – House price developments across and within OECD countries

by Pierre-Alain Pionnier, OECD Statistics and Data Directorate

Housing is key to wellbeing. Real estate typically forms the most important asset of households and their most important source of debt. Not surprisingly given their correlation with the economic cycle, house prices are also one of the most widely tracked economic indicators. However, despite their importance, including for macroeconomic policymaking, as the 2008-09 financial crisis well illustrated, there are few internationally comparable statistics to show how house price developments vary across regions and cities within countries. This is despite the common understanding that changes in house prices within countries are rarely uniform (e.g. there may be ‘ripple’ effects). Policies that target the ‘national’ therefore may miss differences across regions and in turn add to the geography of discontent. This Statistical Insights describes a new OECD database on national and regional house price indices that aims to fill this gap.

There are significant differences in house price developments across countries…

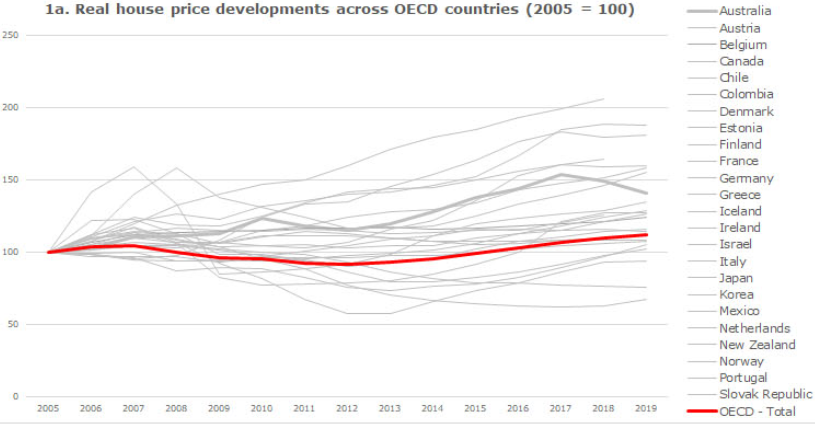

The bursting of the housing bubble in the United States played a key role in the 2008-09 financial crisis, which rapidly turned into a global recession. Even though real house prices (i.e. adjusted for general inflation) declined in several OECD countries, the extent of declines and subsequent ‘recoveries’ differed significantly across countries (Figure 1a). For example, in 2018, house prices in real terms in Colombia were double the levels in 2005, whereas they remained 40% lower in Greece.

This shows that beyond global factors such as those that drove the financial crisis, country-specific factors also matter. These include population growth, land-use restrictions, real household incomes, real interest rates, mortgage market regulations and supervision, lending patterns (at fixed or variable rates), tax relief on mortgage debt financing, and transaction costs such as stamp duty.

… but also within countries.

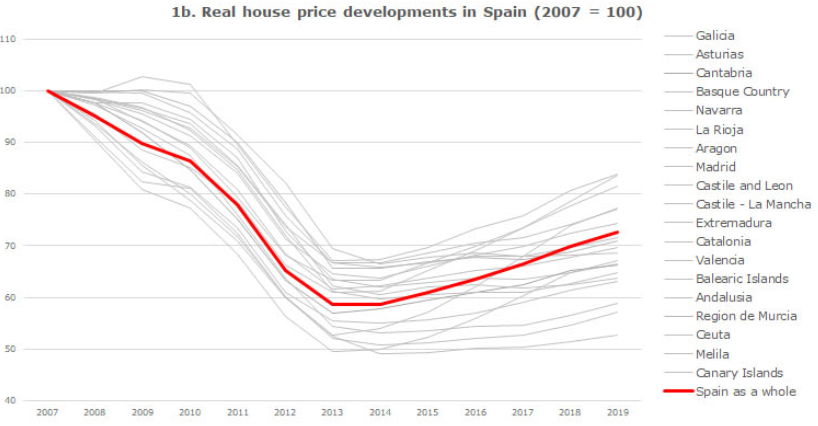

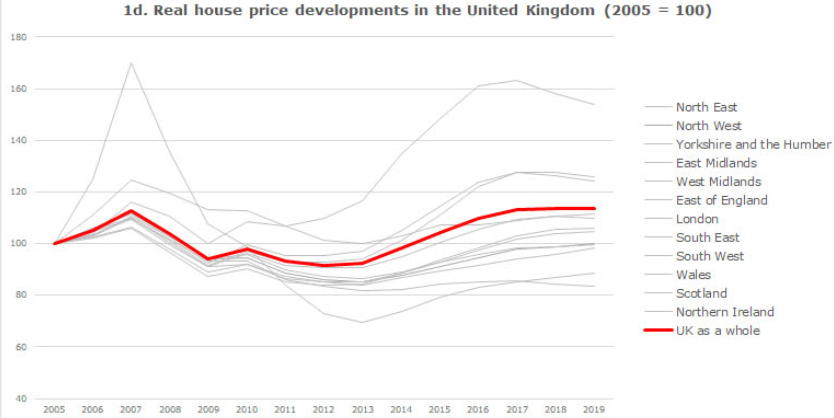

A focus on national price developments does not however tell the full story. Significant differences in the evolution of house prices also exist within countries. For example, while real house prices in Spain declined by 40% on average between 2007 and 2013, and then began to recover, in 2019 they remained nearly 50% lower in Navarra but only 15-20% lower in the Balearic Islands, Ceuta and Melila (Figure 1b). In Mexico, most regions show limited variation around the national average, with real increases ranging from around 10% in the Hidalgo region to around 30% in Yucatan between 2005 and 2018 but this is not universally true. The Federal District for example, which includes Mexico City, saw real prices rise by more than 70% over the same period (Figure 1c). In the UK, Northern Ireland and the region of London show much wider fluctuations in house prices than the rest of the country (Figure 1d).

Figure 1: Real house price developments across OECD countries,

and within Spain, Mexico and the United Kingdom

Note: The evolution of real house prices is the difference between the evolution of (nominal) house prices and the evolution of consumer prices (i.e. general inflation).

Sources: OECD database on national and regional house price indices, OECD national accounts database.

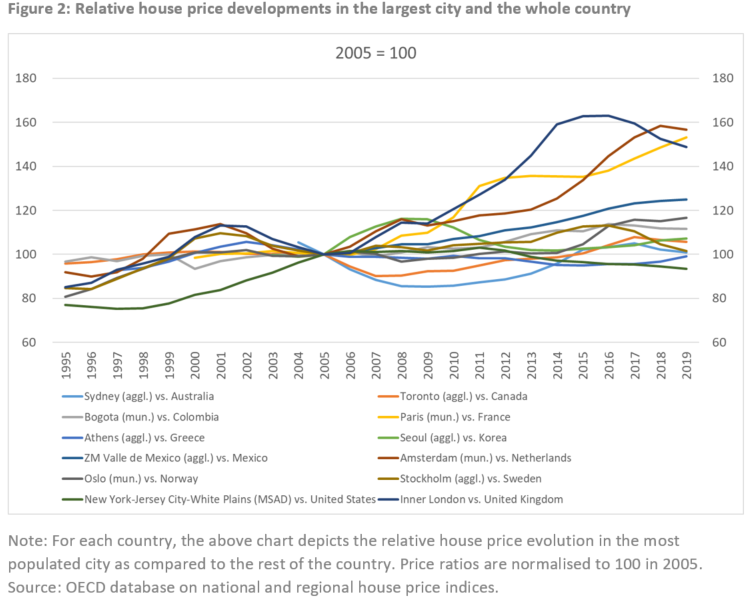

In recent decades, some large cities have seen significant growth in house prices.

In recent decades, an ‘urban resurgence’ (Glaeser 2020), driven in part by better-paid jobs within cities, the willingness to live closer to them, and better access to cultural amenities has led to gentrification and above (national) average house price growth in some of the largest cities. For example, house price inflation in Inner London was around double that of the rest of the United Kingdom between 1995 and 2019. Similarly, house price inflation in Paris between 2005 and 2019 was around 50% higher than in the rest of France (Figure 2).

Nevertheless, this does not exclude large differences across large cities within the same country. For example, the OECD database shows that house prices in the metropolitan area of Los Angeles have grown twice as fast as in the metropolitan area of Chicago since the mid-1990s. Moreover, Glaeser et al. (2012) also emphasise differences in house price developments within cities, with typically faster price growth in recent years in neighbourhoods closer to city centres.

Notwithstanding the fact that economic policy may be suboptimal if one ignores house price heterogeneity within a country, the impact of this heterogeneity on housing affordability may act as a barrier to mobility to households seeking employment in parts of the country where labour demand is higher but cannot always afford to do so due to differences in house prices.

In the years to come, it will be important to assess whether a more systematic use of digital tools to telework following the COVID-19 pandemic will reverse the gentrification of cities and ‘urban resurgence’ phenomena. Granular data on house price developments within countries and cities will become even more relevant for doing so.

The measure explained

House price indices are index numbers measuring the rate at which the prices of residential properties (flats, detached houses, terraced houses, etc.) purchased by households change over time. These indices adjust for quality differences between dwellings sold in the current period, relative to the reference period. In other words, they aim at measuring pure price changes. They cover both new and existing dwellings whenever possible, independently of their final use (to live in or for rent). These prices include the price of the land on which residential buildings are located and they are compiled by official statistical agencies following international statistical standards.

Calculating real house price growth, i.e. controlling for national general inflation, allows for a more meaningful comparison of house price dynamics across countries. The deflator used is the deflator of consumption expenditure of households, compiled according to the 2008 System of National Accounts (SNA). It is important to note that the deflator is typically only available at national level, meaning that the same deflator is used for all regions within a given country, and therefore, that heterogeneity in consumer price dynamics across the different regions of a country is neglected.

Where to find the underlying data

• OECD National and regional house price indices: headline indicators

• OECD National and regional house price indices: Complete database

• OECD National accounts database

Further reading

• Glaeser E.L., J.D. Gottlieb and K. Tobio (2012): Housing Booms and City Centers. American Economic Review: Papers and Proceedings, 102(3), pp. 1-10

• Glaeser E.L. (2020): Urbanization and its discontents. NBER Working Paper26839

• ILO, IMF, OECD, UNECE, Eurostat, World Bank (eds.), (2013): Handbook on Residential Property Price Indices

• OECD (2020): OECD Territorial Grids