Addressing the housing challenges in Central and Eastern Europe

By Federica De Pace, Francesca Papa and Filippo Cavassini, OECD Economics Department; Willem Adema and Marissa Plouin, OECD Directorate for Employment, Labour and Social Affairs.

The historical development of housing in Central and Eastern European (CEE) countries continues to have implications for the tenure, type, quality and affordability of housing today, calling for policy actions to address a looming affordability challenge.

An ageing and low-quality housing stock

CEE countries record some of the highest homeownership rates in the OECD, with over 70% of households owning their home outright. This is largely due to historical reasons, following the privatisation of state-owned housing in the transition to a market economy in the early 1990s. The formal rental market is generally thin and underdeveloped — only in the Czech Republic is the rental market home to more than 15% of households (19%).

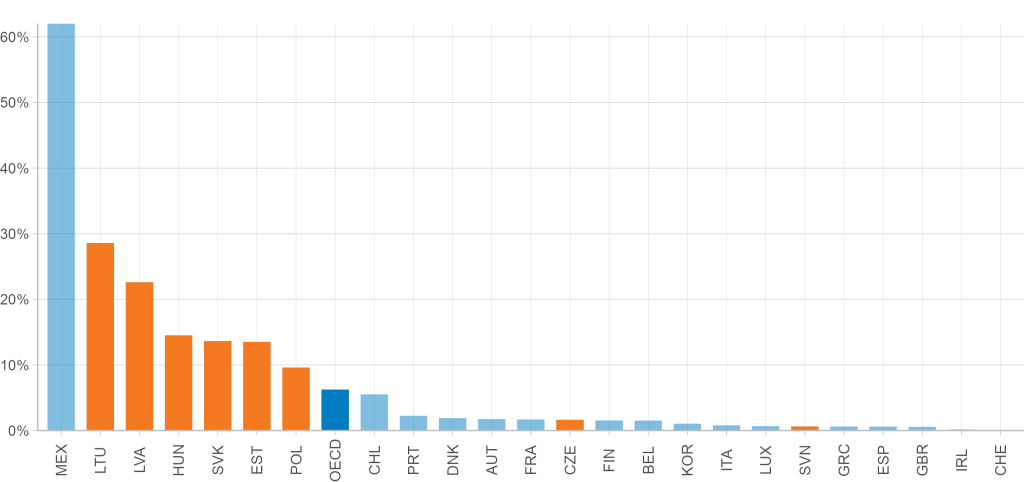

Multi-apartment buildings dominate the housing stock, many built during the communist period. As a result, the stock is ageing and of poor quality. Most households cannot afford to maintain or upgrade their dwellings according to environmental requirements. The share of poor households living in dwellings without access to indoor flushing toilets is well above OECD average in Lithuania, Latvia, Hungary, Slovakia, Estonia and Poland (Figure 1).

Figure 1. The housing stock is of poor quality for many households across the income distribution

Share of poor households1 without an indoor flushing toilet (2019)

Source: OECD, Affordable housing database.

A looming affordability issue

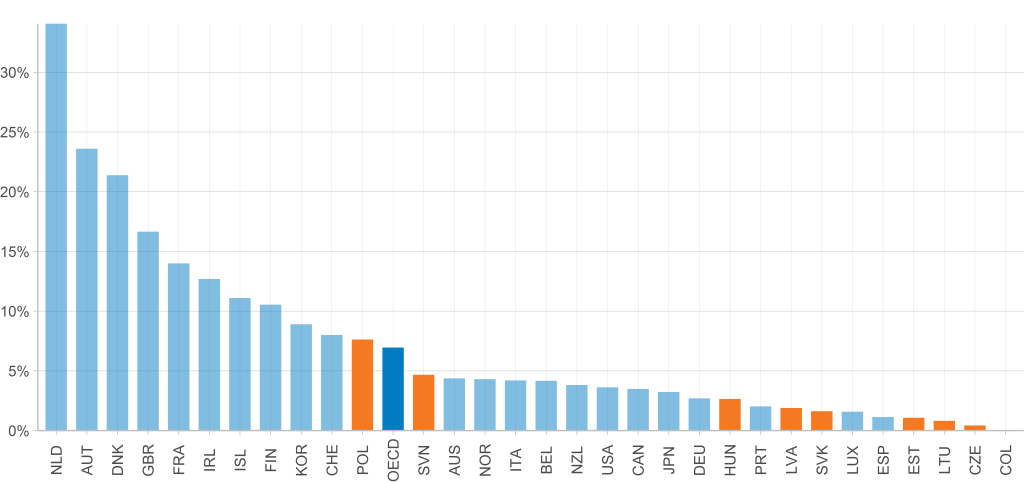

Although households in CEE countries spend less on housing than in other OECD countries (OECD Affordable Housing Database), housing prices in CEE have increased substantially over the past decade and faster than the OECD average (Figure 2).

This is not surprising. As in most OECD countries, the strong increase in housing demand in CEE – also fed by the steady increase in average income and abundant mortgage funding prior to the Global Financial Crisis – has not been accompanied by a corresponding increase in housing supply. Housing investment rates in CEE countries have been substantially lower than the OECD average.

Figure 2. Housing prices in CEE have increased substantially over the past decade and at a faster rate than the OECD average

Affording better quality housing is thus out of reach for many households in CEE countries. For example, an OECD housing affordability review of Latvia shows that 44% of all households – the “missing middle” — are too rich to qualify for social housing or a housing allowance yet too poor to reasonably afford a commercial mortgage (OECD, 2020a).

In parallel, the social housing supply in most CEE countries is well below the OECD average, with the exception of Poland and Slovenia (OECD, 2021). As in most OECD countries, the development of the social housing stock has not kept pace with overall housing construction (Figure 3).

Figure 3. The social housing stock in CEE countries is substantially smaller than the OECD average

Number of social rental dwellings as a share of the total number of dwellings, 2020

What can be done?

OECD countries have taken different approaches to address some of the challenges, from reserving a share of new developments to social housing to tax incentives, among others. Establishing a dedicated funding instrument to boost investment in affordable housing whilst creating the institutional and policy environment to support such investments can be a particularly promising way to address some of the housing challenges in CEE countries.

Boosting sustainable, targeted support for affordable housing

Developing special-purpose funding instruments to channel resources towards affordable and social housing, such as dedicated housing funds, can be an important tool to address the quality, environmental and affordability challenges in CEE countries. Slovakia and Slovenia have already established dedicated housing funds; Latvia is working in this direction. Such funds hold important potential to increase the currently limited housing investment in the region and offer accessible long-term funding needed to bridge affordability and quality gaps (Figure 1 and 2). The OECD 2020 Economic Survey of Lithuania highlighted how the creation of a housing fund could be an effective strategy to improve quality and energy-efficiency of dwellings (OECD, 2020b).

Resources channelled through these funds can leverage public and private funding. In countries where these funds and funding mechanisms have been in place for decades, like Austria and Denmark, funding for social and affordable housing relies on a combination of market loans, guarantees and rental payments. State guarantees help keep borrowing costs low.

The “revolving” element of these funds helps ensure financial sustainability over time, as well as continuous improvements of the housing stock. In Denmark, 2.8% of tenants’ rents contribute to the loan repayment and, once the loan is repaid, are used to finance renovations and improvements. In Austria, tenant equity contributions (about 5-10%) enable low-profit housing associations to generate the surpluses needed to build up equity for future investments, functioning as an internal revolving fund for the associations’ activities. In Latvia, the proposed Housing Affordability Fund will be designed as a revolving fund in which rents paid by tenants are perpetually reinvested in the Fund to finance the construction of affordable rental housing and support upgrades and maintenance.

In Slovakia and Slovenia, the funds directly rely on public funding to construct, repair, and maintain dwellings. In Slovakia, the fund has become financially self-sustained and now relies primarily on the repayments of the loans it provides. The Slovakian State Housing Development Fund has helped support maintenance and refurbishments, responding to the quality gaps common in CEE countries. Half of the refurbished dwellings in Slovakia – a quarter of the overall stock – have been renovated using the Fund.

Creating an enabling environment for better housing quality and affordability

Establishing a fund is an important step – but it isn’t enough. OECD experience shows that funding mechanisms need to be supported by a larger institutional and policy environment – an “eco-system” – in which central and local governments, financial institutions and non-profit housing associations work together for a common purpose. This institutional and policy environment should accompany efforts in CEE countries to bolster sustainable funding for quality, affordable housing.

In Austria, Denmark and the Netherlands, for instance, housing associations have been active in developing and maintaining social and affordable housing. While such actors are less developed in CEE countries, opportunities to further develop such a sector could help meet demands and needs that are currently not met by existing market actors. In Slovakia, not-for-profit organisations are eligible for loans from the State Housing Development Fund. In Slovenia, the Housing Fund co-invests in local community housing programmes, working with municipalities and non-government organisations to meet local needs.

New funding mechanisms to channel investment in housing, bolstered by an enabling institutional environment, can support housing policy development and implementation and act as a catalyst for substantial improvements in housing quality and affordability in CEE countries.

References

OECD (2020a), Policy Actions for Affordable Housing in Latvia, OECD Publishing, Paris, https://issuu.com/oecd.publishing/docs/latvia_housing_report_web-1

OECD (2020b), OECD Economic Surveys: Lithuania 2020, OECD Publishing, Paris, https://doi.org/10.1787/62663b1d-en

OECD (2021), Brick by Brick: Building Better Housing Policies, OECD Publishing, Paris, https://doi.org/10.1787/b453b043-en

OECD Affordable Housing Database, https://www.oecd.org/housing/data/affordable-housing-database/