Greater fiscal prudence would help sustain growth in the Netherlands

Scrapping the most inefficient expansionary measures

and further enhancing the fiscal framework would contribute to preserving sound public finances.

By Daniela Glocker and Nicolas Gonne, OECD Economics Department

Sound public finances have largely contributed to the resilience of the Dutch economy. Years of fiscal discipline allowed the country to build up substantial budgetary buffers. These enabled the government to support households and businesses during recent downturns. They also provide the fiscal space needed to implement structural reforms.

However, current budgetary plans reflect a shift in priorities, towards increasing purchasing power in the short run and away from policies that support productivity, enhance competitiveness, and accelerate the green transition. The deficit is projected to widen from 0.9% of GDP in 2024 to 2.3% in 2025 and 2.8% in 2026 (Figure 1).

Figure 1. Public finances are projected to deteriorate

General government fiscal balance (% of GDP)

Should it not correct its course, the Netherlands could face a “Significant Deviation Procedure” under the preventive arm of the EU Stability and Growth Pact. Such a scenario is unlikely, as the government is strongly committed to remaining in compliance with EU Treaty limits for deficit and debt levels, and because supply bottlenecks often led to underspending in recent years. Yet, proactive fiscal adjustments would provide greater policy certainty and credibility, as discussed in the latest OECD Economic Survey of the Netherlands.

Budgetary plans should aim at expanding supply, not boosting demand

The fiscal stance is expansionary, with significant increases in spending on healthcare and housing, and with lower revenue from personal, corporate, and environmental taxation. Several new spending and tax measures are costly and lack targeting, including the reduction in out-of-pocket payments for medical care and the introduction of a new, lower-rate bracket for personal income taxation.

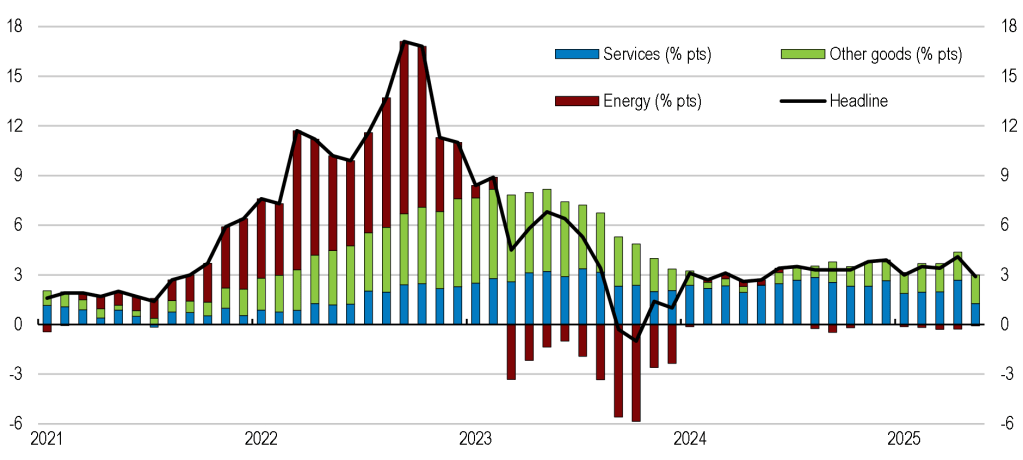

The expansion risks exacerbating inflationary pressures given persistent supply constraints, most notably the tight labour market. Labour costs have been rising relatively quickly since the post-pandemic recovery, pushing up the cost of labour-intensive services and contributing to elevated inflation (Figure 2). Further supply bottlenecks include electricity grid congestion, skills mismatch, and the knock-on impact of the nitrogen crisis. At the same time, spending cuts on education and R&D, while partially offsetting the fiscal cost of expansion, will weigh on growth potential and productivity.

Figure 2. Wage-driven price pressures remain

Contributions to consumer price inflation (y-o-y % change)

Fiscal prudence is key to supporting the economy and sustaining growth, by avoiding excessive demand stimulus and promoting supply-side expansion. Scrapping the most inefficient expansionary measures should be a priority. Reallocating expenditure towards efficiency-enhancing public investments would further promote growth potential, while reconsidering proposed cuts to public spending on knowledge, skills, and innovation would further help productivity, an increasingly pressing challenge for the Dutch economy.

Fiscal reforms are necessary to safeguard sound public finances

Under current budgetary plans, the fiscal balance is expected to deteriorate steadily over the medium run, particularly from 2029 onwards. This is despite the Dutch trend-based fiscal framework, which has been instrumental so far in maintaining fiscal space while enabling automatic stabilisers to fully operate –a particularly important feature to absorb global shocks in an open economy like the Netherlands’.

Most aspects of Dutch multi-year fiscal strategy are regarded as best practice under the OECD Spending Better Framework. However, the expenditure framework is fixed over the government’s term, while budgetary measures are announced on an annual basis. This limits the framework’s ability to address long-run fiscal pressures and can create incentives to postpone politically difficult but necessary decisions on revenue-raising measures and spending cuts.

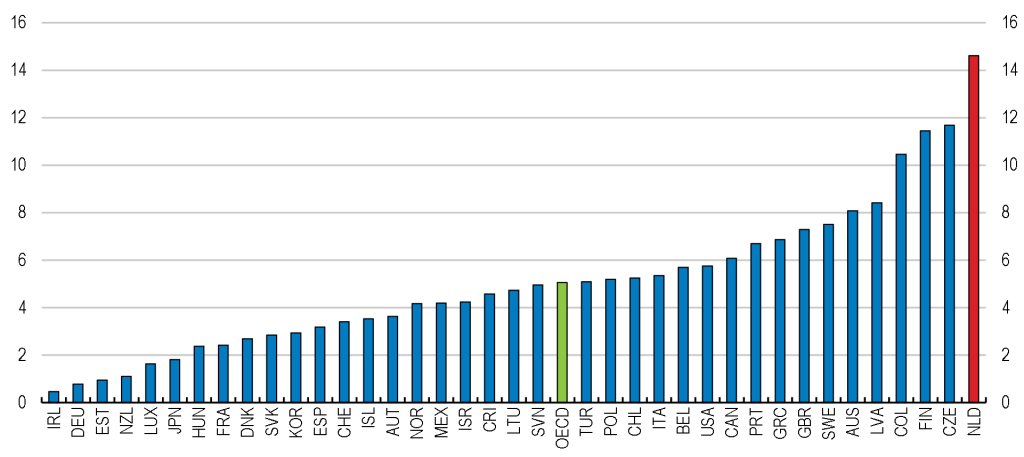

Rolling forward expenditure ceilings every year to keep a constant spending horizon would provide greater predictability, enhance transparency, and further support fiscal sustainability, while keeping the benefits of the current framework, including fiscal discipline on the expenditure side and macroeconomic stabilisation on the revenue side. This would be conducive to greater fiscal prudence, creating the conditions for achieving a balanced combination of revenue-raising measures and targeted spending cuts, including by reducing inefficient tax expenditures (Figure 3).

Figure 3. There is room to streamline tax expenditures

Tax expenditures (% of GDP), 2024 or latest available year

For more information, please visit our Netherlands Economic Snapshot page.

REFERENCES

Borowiecki M., J. Pareliussen, and D. Glocker (2021), “Chasing the frontier: Digitalisation for stronger productivity in the Netherlands”, OECD Economics Department Working Papers, No. 1680, OECD Publishing, Paris, https://doi.org/10.1787/e800ee1d-en.

CPB (2025), “Centraal economisch plan 2025 [Central economic plan 2025]”, Netherlands Bureau for Economic Policy Analysis, The Hague.

OECD (2025), OECD Economic Surveys: The Netherlands 2025, OECD Publishing, Paris, https://doi.org/10.1787/2dd1f4aa-en.

Gonne, N. (2023), “Lifting labour supply to tackle tightness in the Netherlands”, OECD Economics Department Working Papers, No. 1771, OECD Publishing, Paris, https://doi.org/10.1787/df5448fe-en.

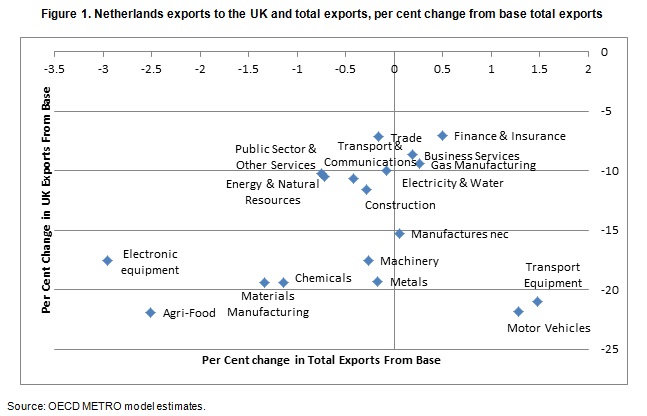

The Netherlands is likely to be one of the European countries that is going to be significantly affected by the United Kingdom’s planned departure from the European Union (Brexit). As an open economy with strong trade and investment links to the United Kingdom, the Netherlands is exposed to increases in barriers to trade between the United Kingdom and EU (Vandenbussche et al., 2017). New OECD simulations show the potential extent of this impact, as well as the different sectors of the Dutch economy likely to be affected.

The Netherlands is likely to be one of the European countries that is going to be significantly affected by the United Kingdom’s planned departure from the European Union (Brexit). As an open economy with strong trade and investment links to the United Kingdom, the Netherlands is exposed to increases in barriers to trade between the United Kingdom and EU (Vandenbussche et al., 2017). New OECD simulations show the potential extent of this impact, as well as the different sectors of the Dutch economy likely to be affected.