Reviving business dynamism in Japan

In the context of a shrinking working-age population, Japan needs to reignite productivity growth to sustain living standards. Annual growth in hourly productivity fell from 1.2% in the 2000-08 period to 0.3% between 2019 and 2024.

By Patrizio Sicari, OECD Economics Department

Business dynamism, which spurs productivity by encouraging firm entry and subsequent growth, as well as the exit of less productive firms, is weak in international perspective (Figure 1). As highlighted in the 2026 OECD Economic Survey of Japan, strengthening competition, making public support to small and medium-sized enterprises (SMEs) more effective and reforming the innovation framework and incentives for start-ups are key to a more dynamic entrepreneurial ecosystem.

Overhauling cumbersome business regulations

Starting a business is relatively complex, requiring several procedures across different institutions. The introduction of online business registration in 2020 formally reduced the need for time-consuming direct contact with licensing, employment and social security authorities. Access to the relevant online services occurs through a common digital authentication platform (gBizID) managed by the Digital Agency. However, limited digitalisation means that this opportunity is not fully exploited.

Further improving the availability and uptake of digitised administrative procedures requires expanding gBizID’s service coverage across local governments and promoting its adoption among firms. Among corporations, only 33% have registered with the service as of early 2026, well below the government’s 80% target by 2030. Seamless digital integration across government services would enable firms to avoid resubmitting information already held by other public authorities (the “once-only” principle). Adopting a “silence is consent” principle would also ease procedural uncertainty for more complex licences and permits.

Ensuring efficient capital allocation towards more dynamic SMEs

As of March 2025, around 45% of SMEs held publicly guaranteed loans offering 80% coverage of private banks’ credit risk, amounting to 5.3% of 2024 GDP (Figure 2, Panel A). Public financial institutions provided SMEs with a further 4.2% of GDP in direct loans. Although at levels below pandemic peaks, these broad-based guarantees and subsidised loans weigh on business dynamism. They prevent the exit of low-productivity firms, hindering the reallocation of resources towards more dynamic firms. Indeed, the share of zombie firms eased somewhat after the phase-out of pandemic-era support, but remained elevated at 14.3% in FY2024 (Panel B). Lowering guarantee coverage rates would improve risk sharing between banks and the public sector by strengthening banks’ incentives to carry out deeper credit screening.

Public SME support is largely bank-based, constraining access for innovative start-ups lacking tangible assets for collateral or personal guarantees required by risk-averse banks. Limited availability of alternative financing sources also prevents their scaling up. Greater reliance on public venture capital (VC) investment would boost the valuation and scaling of artificial intelligence and deep-tech start-ups. The limited size of the late-stage VC market often forces highly innovative start-ups to go public prematurely, after which many struggle to secure follow-on funding, constraining their productivity potential. Complementing public VC with a wider use of mezzanine financing instruments, which offer more flexible growth capital, would also help limit direct public exposure.

Redesigning public support for broader innovation and scaling up

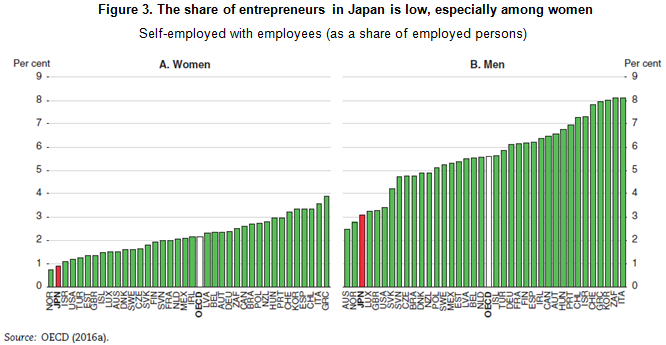

Japan has the fifth highest expenditure on research and development (R&D) in the OECD, but this is mainly commercially oriented and concentrated in large manufacturing firms. Openness to foreign R&D funding and collaboration with universities remains limited, especially among SMEs, which performed just 5% of business R&D in 2023 (Figure 3). R&D tax incentives make up around 75% of total public support for business R&D, but they mainly benefit large incumbents. This reduces the likelihood of SMEs developing breakthrough inventions and scaling up, constraining innovation and its diffusion.

The R&D tax system should be simplified. The main existing schemes are combinable but separately administered, with different eligibility criteria, rate calculations, and varying deduction ceilings. In addition, a recent tax reform introduced higher R&D tax credit rates for business investment in strategic-technology research fields from FY2027, which could increase fragmentation. Together with various revisions and temporary provisions, these features lower the system’s predictability and make it administratively burdensome. A more streamlined and stable system would help increase uptake among smaller innovative firms, which are more likely to drive productivity growth.

To support scaling, public R&D policy should more effectively target innovative start-ups, reducing the share of support to profitable incumbents that are likely to invest in innovation regardless. Amendments to the Corporate Tax Act approved in March 2026 move in this direction, by allowing innovative SMEs, which typically have little or no tax liabilities, to carry forward unused R&D tax credits for up to three years from FY2027. However, this was accompanied by less favourable effective credit rates for firms that do not increase R&D spending over time. Complementary measures making credits partly refundable for research aligned with specific policy objectives (e.g. fostering systemic innovation) would strengthen investment incentives for early-stage firms and help broaden the innovation base.

In addition, the 2026 OECD Economic Survey of Japan provides policy recommendations to enhance competition in services, encourage greater inward foreign direct investment, promote an effective skills pipeline for innovation-oriented research and boost the adoption of advanced digital technologies.

Visit the OECD’s Japan Economic Snapshot page for further information.

References

OECD (2026), OECD Economic Survey of Japan, OECD publishing, Paris.