Powering competitiveness: Europe’s path to energy security and growth

by Ruben Maximiano and Wouter Meester, OECD Economics Department.

Europe’s competitiveness is increasingly linked to the availability of secure, affordable and reliable electricity. As electrification accelerates across industry, transport, heating and digital services, including AI data centres, power has become a strategic input to growth, investment and innovation, a point also underscored by the 2024 Draghi report. However, as outlined in a recent OECD report Diagnostic Tool for Reducing Regulatory Barriers to Solar, Wind and Pumped Hydro Storage in the EU, five key types of regulatory barriers slow the deployment of these technologies in Europe. This results in significant opportunity costs, especially in the European Union, where high import dependence exposes firms and households to price volatility, supply shock and higher prices.

The 2021–22 energy crisis laid bare this vulnerability: the EU’s energy import bill surged from EUR 137 billion in 2020 to nearly EUR 549 billion in 2022. Even after prices eased, the 2023 import bill remained well above historical levels.

Why the electricity system is changing and why rules matter

At the same time, Europe’s power system is being reshaped by technologies with fundamentally different system characteristics, including variable renewables, storage, demand-side response and digital controls. These resources increase the need for flexibility, real-time coordination across grids and more granular planning, particularly as new electricity-intensive loads, such as data centres, concentrate demand in specific locations. This transformation exposes the limits of regulatory frameworks designed for a centralised, thermal-based system. Ensuring the EU’s energy security, including by delivering its new energy mix, depends on fit-for-purpose regulation as much as on physical infrastructure.

Competitiveness increasingly depends on affordable, “always-on” electricity

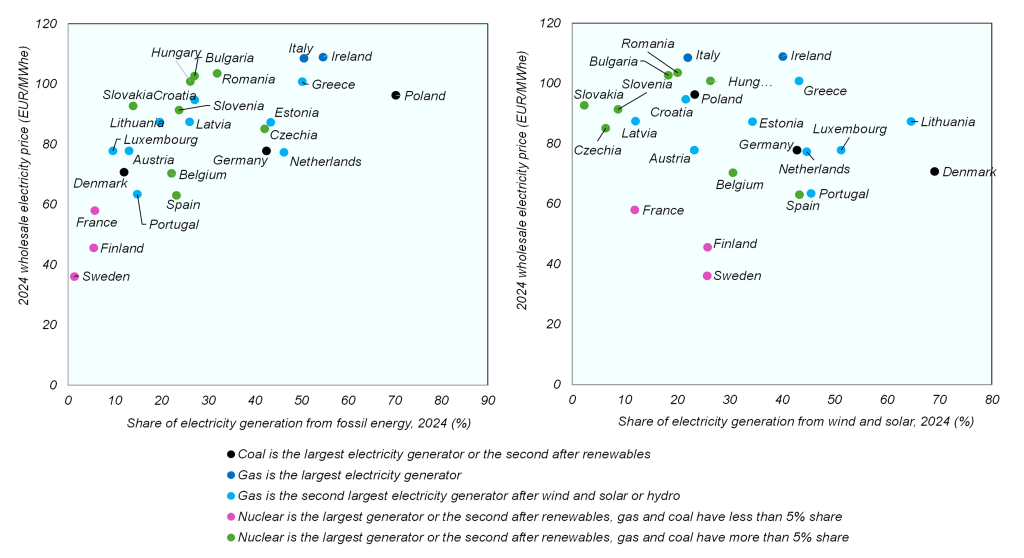

In addressing its energy security, Europe has already made important progress. Since Russia’s invasion of Ukraine, renewable energy has expanded substantially, helping to cushion price shocks (see Figure 1). Evidence suggests that EU countries with higher shares of wind and solar in their electricity mix tend to exhibit lower wholesale prices on average (Figure 2), reflecting the declining technology costs and the downward pressure renewables place on marginal pricing. Moreover, recent system-level modelling by WindEurope shows that, even once the additional cost of grids, storage and backup capacity are taken into account, a renewables-led pathway is the lowest-cost option for Europe’s power system.

Figure 2. Relationship between the average wholesale electricity prices and the share of electricity generation from wind and solar in EU Member States, 2024

Source: OECD calculations based on Ember Yearly and Hourly Electricity Data

Yet the next wave of electrification will put (even greater) pressure on the EU’s electricity system. For example, in the EU, demand from data centres could rise from around 96 TWh in 2024 to about 236 TWh by 2035, increasing their share of total electricity use from 1.5% to nearly 6%.

Energy system upgrades require regulatory upgrades – and a tool to help deliver them

This increasing electrification, with more decentralised generation, new flexibility technologies and large, concentrated loads such as data centres, requires regulatory frameworks that are aligned with these new system characteristics.

In this context, regulation increasingly functions like infrastructure itself: it must be planned ahead of need, operate reliably, and remain aligned with system needs. Outdated or fragmented rules quickly become binding constraints on investment, adding years to project timelines and raising costs. As such, modernising and simplifying regulatory frameworks have become a strategic lever of energy security and competitiveness.

Recent EU legislation, including the Renewable Energy Directive III, provides an important foundation. Implementation at national level, however, will determine whether projects proceed from pipeline to operation.

Across EU Member States, five recurring regulatory barriers consistently slow deployment and undermine system efficiency:

First, unclear or restrictive legal frameworks create uncertainty and deter market entry, particularly for newer solutions. Where rights and permitted uses have been clarified – such as enabling dual land use for both agriculture and PV solar in France and Italy – deployment has accelerated; where ambiguity persists, projects stall.

Second, insufficient remuneration for new system services limits investment, for instance in flexibility. Many frameworks still do not reward services such as inertia or fast frequency response on a standalone basis, despite their growing importance for system stability. Ireland’s recent market reforms to remunerate these ancillary services illustrate how rule changes can unlock these services.

Third, infrequent and inefficient spatial planning and permitting remain a major drag on investment. Complex, sequential procedures involving multiple authorities often result in long timelines distorting siting decisions and raising financing costs. Where procedures have been simplified, impacts have been immediate and significant: reform to grid-permitting rules in Germany have enabled the Federal Network Agency (BNetzA) to approve roughly four times more transmission-line kilometres in 2024–25 than in previous years (see figure 3).

Fourth, outdated grid-connection rules create artificial bottlenecks. First-come, first-served queues allow speculative projects to hold capacity delaying viable investments. Sweden’s readiness-based connection rules show how prioritisation can improve outcomes without new infrastructure.

Finally, grid-investment frameworks still contain structural disincentives that limit system optimisation. Regulation often favours capital-intensive network expansion while constraining anticipatory investment, flexibility procurement, and digital solutions. In some Member States, system operators cannot recover the costs for non-wire alternatives, even when these are faster and cheaper than traditional reinforcement.

These barriers can add years to project timelines and increase financing costs. They affect not only renewable developers but also energy-intensive industries, such as AI infrastructure and advanced manufacturing, that require stable, low-cost electricity to remain competitive.

To address these barriers systematically, the OECD has developed the Diagnostic Tool for Reducing Regulatory Barriers to Solar, Wind and Pumped Hydro Storage in the EU for the European Commission. The Tool helps policymakers at national and sub-national levels identify where rules are misaligned with system needs, prioritise reforms, and coordinate implementation – providing a practical roadmap for accelerating electrification while strengthening both energy security and competitiveness.

With clear rules, coordinated planning and tools such as the OECD Diagnostic Tool, the EU can move from energy dependence toward electric resilience – strengthening both economic competitiveness and energy security.

*We will be launching the Diagnostic Tool on 29th January. You may register here.

References

Draghi, M., 2024. The Future of European Competitiveness—A Competitiveness Strategy for Europe

IEA, 2025, Energy and AI, World Energy Outlook Special Report

IEA, 2023, Renewable Energy Market Update Outlook for 2023 and 2024

WindEurope and Hitachi, December 2025, Delivering a cost-effective energy system for Europe

The global economy is navigating rough seas. Global GDP growth is strong but has peaked. In many countries unemployment is well below pre-crisis levels, labour shortages are biting and inflation remains tepid. Yet, global trade and investment have been slowing on the back of increases in bilateral tariffs while many emerging market economies are experiencing capital outflows and a weakening of their currencies. The global economy looks set for a soft landing, with global GDP growth projected to slow from 3.7% in 2018 to 3.5% in 2019-20. However, downside risks abound and policy makers will have to steer their economies carefully towards sustainable, albeit slower, GDP growth.

The global economy is navigating rough seas. Global GDP growth is strong but has peaked. In many countries unemployment is well below pre-crisis levels, labour shortages are biting and inflation remains tepid. Yet, global trade and investment have been slowing on the back of increases in bilateral tariffs while many emerging market economies are experiencing capital outflows and a weakening of their currencies. The global economy looks set for a soft landing, with global GDP growth projected to slow from 3.7% in 2018 to 3.5% in 2019-20. However, downside risks abound and policy makers will have to steer their economies carefully towards sustainable, albeit slower, GDP growth.