High uncertainty is weighing on global growth

By Laurence Boone, OECD Chief Economist

Less than 6 months ago, the global economy enjoyed healthy synchronised growth. Now, the landscape has changed. Global growth is hitting a plateau, uncertainties over the path forward abound, and risks from trade restrictions and tighter financial conditions have already started to materialise in some countries.

Global growth is projected to be at 3.7% in 2018 and 2019 in our latest Interim Economic Outlook, which remains an elevated pace. At the same time, it also reflects weaker prospects than anticipated just a few months ago, and some fragilities. Growth performance has become less synchronised across the world: while it remains strong in the United States, India and China, it has faltered in many other economies. Unemployment has continued to decline and is now below its pre-crisis level in the OECD, but wage growth remains persistently weak, raising uncertainties about how much spare capacity remains in the labour market. In other words, many workers would like to work more hours in Europe, or have left the labour force in the United States, fueling poor well-being perceptions.

More worryingly, risks – trade, emerging economies’ sensitivity to tightening financial conditions, politics, finance – are intensifying, casting shadows over the outlook for the coming months and years.

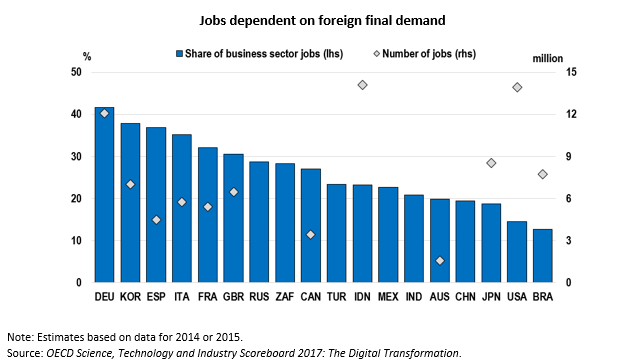

The consequences of rising trade restrictions are already visible. World trade in goods has markedly slowed in recent months, with acute impacts in the sectors directly targeted. For instance, the prices of washing machines for US consumers jumped by 20% between March and July this year after the imposition of tariffs. US imports of steel from China are sharply down, just like Chinese imports of cars from the US. Down the line, higher tariffs mean higher prices for consumers, less investment and less jobs for workers, and ultimately losses in productivity and standards of living. Just consider that 13 million jobs in the US and 8 million in Japan depend, directly or indirectly, on foreign consumption.

Another risk that has started to dent growth is, in emerging market economies (EMEs), the effect of rising interest rates and US dollar appreciation. Argentina and Turkey, having significant shares of debt in foreign currency, large external financing needs and high domestic inflation, have been the most exposed to turbulence in currency markets. Other EMEs with high foreign reserves, credible monetary frameworks and prudent fiscal policies, are better equipped to withstand shifts in investors sentiment that are unavoidable as monetary policy normalises around the world. Floating exchange rates have played their cushioning role which has limited contagion so far, but measures to ensure persistent macroeconomic policy credibility and resilience in more vulnerable economies are essential to safeguard financial stability.

In Europe, political risks could harm growth and social cohesion. Brexit is an obvious source of uncertainty. It is vital that a deal is struck that maintains the closest possible relationship between the United Kingdom and the European Union. As for Italy, public finances need to respect EU rules, ensure debt sustainability while privileging productive investments badly needed to raise growth. More largely, the EMU policy framework needs to be strengthened along the commitment made in the wake of the euro area crisis to enhance confidence, growth and ensure the euro area thrives as it should.

As we mark the tenth anniversary of the financial crisis, there is no denying that some lessons have been learned: banks are now better capitalised, and financial regulation has been stepped up thanks to a large extent to international coordination. But in other areas, financial risks have built up again. Debt has reached unprecedented highs, particularly in the public sector and for corporate debt. Less regulated shadow banking has expanded rapidly. In some countries, equity prices and housing markets are further cause for concern.

In light of the many risks, what should policymakers do?

The immediate priority is to preserve business confidence and investment by reducing policy uncertainty – including by restoring international dialogue to avoid the escalation of trade restrictions. Enhancing resilience is also key in the financial sector as well as, in the case of Europe, by completing the banking union launched in 2012.

In case risks materialise further, there is little space left for monetary policy to react in advanced economies. This makes it all the more important for countries currently enjoying strong growth not to widen fiscal deficits to support an already vibrant consumption, but instead to rebuild room for manoeuvre for those which lack it, and expand public investment to shore up the foundations for sustained growth for all.

At the same time, to foster thriving societies and provide a durable response to political tensions, structural policies should focus on ensuring all people have access to better opportunities. In the long term, the keys to healthy productivity gains and growth that benefits all lie in quality education, from early childhood to lifelong learning, and in offering better support for all workers to find good and fulfilling jobs. This is vital to reduce political uncertainty in a sustainable manner.

Reference

OECD Interim Economic Outlook, September 2018.