Statistical Insights: An x-ray view of inflation

By Pierre-Alain Pionnier, Francette Koechlin, Anne-Sophie Fraisse and Elena van Eck.

Inflation may be present in some parts of an economy but not others. Contributions to annual inflation show how much different product groups contribute to overall inflation in a given year.

The measure is a useful tool to understand where inflation is occurring in different countries, analyse trends in inflation over time, and identify volatile and stable components of inflation. It may also help explain why consumers’ perceptions of inflation sometimes differ from official figures.

This Statistical Insight uses figures for Germany, Japan and the United States (US) to illustrate the usefulness of data on contributions to inflation.

Analysing inflation by component

In addition to aggregate national Consumer Price Indices (CPIs), the OECD provides data on the contributions to annual inflation of 12 standard product groups and special aggregates.

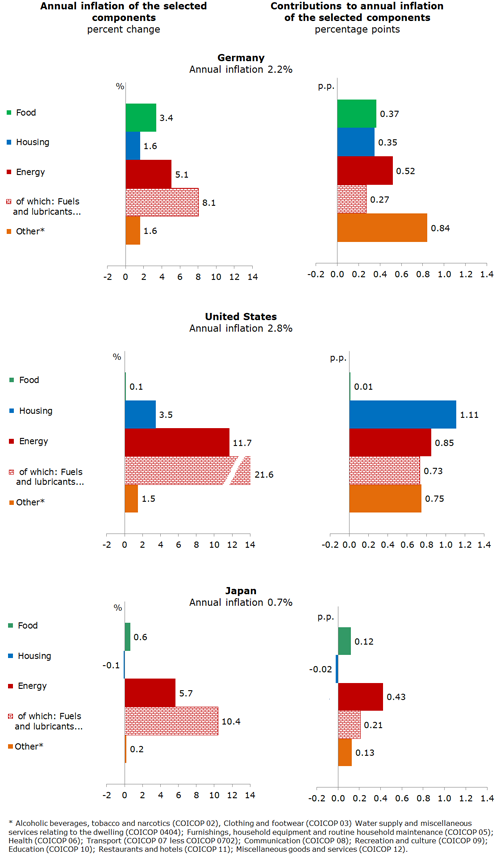

Figure 1 shows that in Germany, Japan and the US, aggregate inflation hides wide variations in price movements across product groups. In Germany, while overall prices increased by 2.2% in the year to May 2018, food and housing prices increased by 3.4% and 1.6% respectively. In the US, energy prices increased by 11.7%, and gasoline prices by 21.6%, while overall prices only increased by 2.8%.

The contribution of a given product group to overall inflation depends both on the price change of the relevant product group and on its share in consumers’ expenditures. The shares vary between countries. For example, households spend around 20% of their incomes on housing in Germany and Japan, but over 30% in the US. The high share of housing costs in US households’ budgets meant that price changes in those costs contributed most to overall US inflation in the year to May 2018, even though energy prices rose much faster than housing prices. In fact, energy prices shot up everywhere, but only in Japan was energy the largest contributor to overall inflation.

It may also be the case that consumers are more sensitive to movements in the prices of items they purchase frequently. For example, they may feel that inflation is high if the prices of food items are rising quickly, even though food products and non-alcoholic beverages represent less than 10% of households’ expenditures in the US, around 10% in Germany, and less than 20% in Japan.

Figure 1. Annual inflation rate (%) and contributions of selected components

May 2018, Germany, United States and Japan

Recent trends in overall and core inflation (2012-2018)

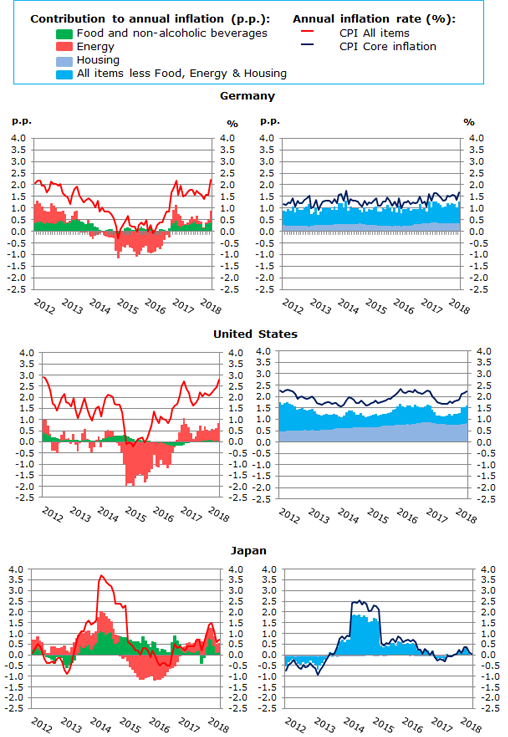

Because food and energy make volatile contributions to inflation, economists often focus on a consumption basket that excludes them in order to better understand and forecast long-term developments in inflation. The resulting numbers are called underlying, or core, inflation.

Figure 2 shows that energy contributed to the bulk of inflation fluctuations between 2012 and 2018. Changes in energy prices are dominated by movements in world crude oil prices, but exchange rate fluctuations also play a role because oil prices are usually fixed in US dollars. In 2015, for example, oil prices fell but at the same time the euro and the yen depreciated against the US dollar, so that oil prices in those currencies did not fall as much as they did in dollars. This meant that falling oil prices did not reduce inflation as much in Germany and Japan as in the US.

Even after excluding volatile food and energy prices, core inflation rates vary significantly across countries. Figure 2 shows that core inflation in Japan has long been lower than in Germany and the US, except for a blip in 2014-15 caused by a hike in value-added tax. Since 2016, core inflation in the US has also been consistently higher than in Germany. The major contributor to these differences is housing prices, which have risen faster in the US than in Germany, and faster in Germany than in Japan. Note that housing prices correspond to housing rentals (including imputed rentals for owner-occupied dwellings) and maintenance costs. This ignores the purchase prices of houses and apartments, which are considered as investments rather than consumption and are covered by separate price indices.

Figure 2. Annual inflation rates (%) and contributions of selected components (percentage points)

2012-2018, Germany, United States and Japan

The measure explained

Contributions to annual inflation represent the contributions to overall inflation in percentage points by different product groups. The contribution of each product group depends both on the price change in the relevant product group and its weight in households’ expenditures.

The OECD calculates contributions to inflation based on national data for all countries except Austria, Chile, Finland, Mexico, the Netherlands, Poland, Sweden, and the United Kingdom, whose National Statistics Offices provide the data directly. For further information please see OECD CPI FAQs.