Greece: Achieving the green economy transition

By Tim Bulman, Timo Leidecker and Ilai Levin, OECD Economics Department

More intense and more frequent wildfires and floods, hotter and drier summers, and disrupted seasons are among the striking signs that the climate in Greece and globally is changing. Like other OECD countries, Greece is contributing to the global effort to mitigate climate change by becoming a net zero emission economy.

Reducing emissions from energy use to transition towards a net-zero economy

The green economy transition poses a particular challenge for Greece. The economic crisis of the last decade has limited public and private financial capacity to invest in renewable energy production, make infrastructure more resilient, improve energy efficiency, upgrade heating systems, and replace fossil-fueled with zero emission cars. Using public funds effectively, mobilising private capital, and raising additional revenues will be key for Greece. The just-released OECD Economics Working Paper on “Transitioning to a green economy in Greece“, drawn from the OECD Economic Survey of Greece (2023) presents a mix of the policies required to limit the financial and social coss of the transition. Achieving the transition is feasible with little long-term cost to incomes and employment, especially if continued reforms to improve the business environment and raise investment accompany the transition (discussed in this ECOSCOPE post).

The Paper identifies three policy priorities that would make substantial cuts to the more than two-thirds of Greece’s emissions that come from energy use:

1. Pricing greenhouse gas emissions consistently to encourage investment, innovation and savings. Average CO2 prices from using fossil fuels are high in Greece but vary substantially across uses. For example, charges on CO2 emissions from using gasoline are effectively double those from diesel; in turn, charges for using fossil fuels for heating or producing electricity are much lower than average charges for using fossil fuels for road transport. Introducing a minimum price floor to harmonise prices would encourage low-cost ways to cut emissions. Higher and more consistent prices for emissions would also generate more than enough revenues to compensate low-income households for rising living costs.

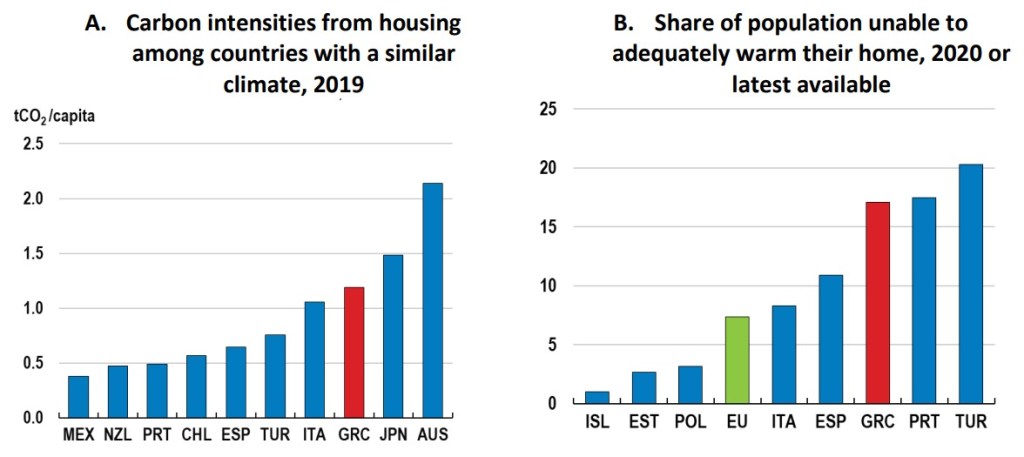

2. Giving a push to renovate buildings. Greece has an old housing stock with low energy efficiency. This harms residents’ well-being, especially when energy prices are rising, as experienced over the past year. It also contributes to high greenhouse gas emissions in Greece compared to countries with similar climates (Figure 1). Housing renovations can cut emissions, improve residents’ comfort, and usually pay for themselves through energy savings. The up-front costs of renovations, however, can be a major barrier to realising these savings. Substantially expanding the current financial support programmes and – to leverage more private financing – encouraging loans that are repaid through energy savings would boost renovations. Setting out a clear timeline of increasing minimum energy-efficiency standards to cover both new and existing buildings would provide certainty for investors and builders, bringing more resources to renovations and create green jobs.

Figure 1. Improving housing energy efficiency would reduce emissions and energy poverty

3. Moving transport onto low-emission modes. Cutting emissions from transport is costly and complex but, as it generates one-fifth of Greece’s total emissions, is central to Greece’s goals. More passengers and freight are carried on roads than in the EU on average. The car fleet is large and old, with Greeks spending less on buying cars than in most other OECD countries (Figure 2). Renewing the car fleet, especially with more expensive low-emission cars, is likely to be very slow, even if purchase subsidies were used more extensively. At the same time, modelling by the International Transport Forum and the OECD finds that improving public transport could cut transport emissions in Greece by 19% in 2030 relative to 2019 levels with an additional investment of about 0.2% of GDP annually.

Figure 2. Alternatives to road transport could cut emissions from transport cost effectively

Helping people and businesses adapt to the changing climate

Transforming the economy to net-zero emissions will affect how firms operate and which skills are needed. As some jobs bound to fossil fuels disappear, for example in lignite mining, new and potentially higher productivity job opportunities will be created, for example in housing renovations or greener technologies. Workers may need to up-skill for these new jobs, especially in regions highly dependent on fossil fuel industries such as Western Macedonia. Focused interventions such as those underway in Greece’s lignite mining areas are increasing access to quality training. and help hasten this transition and support incomes.

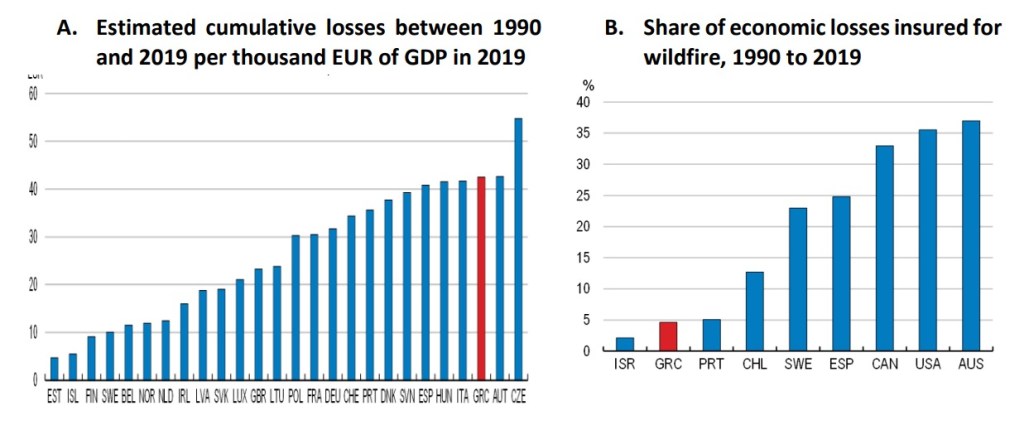

Damages from extreme weather events, such as wildfires or floods, are already mounting in Greece and are likely to further aggravate. Encouraging households and firms to anticipate these risks when they decide where and what to build will help reduce the disruption from a changing climate. Private insurance can help make the costs of climate-related risks clearer. Yet, insurance coverage in Greece is among the lowest in OECD countries (Figure 3). After past natural disasters the government has partly compensated damages, but this leaves people uncertain about how much and when they will receive compensation and weighs on public finances. Making insurance coverage compulsory could encourage people to take protective measures upfront, would leverage the skills of the private sector to assess reconstruction costs, and provide greater certainty to those afflicted. Public re-insurance, and ensuring that insurance markets remain competitive, can improve the accessibility of insurance.

Figure 3. Expanding insurance coverage would improve compensation for damages and encourage households and firms to minimise their exposure to a changing climate

Reference:

OECD (2023), OECD Economic Surveys: Greece 2023, OECD Publishing, Paris, https://doi.org/10.1787/c5f11cd5-en.

Leidecker, T., et al. (2023), “Transitioning to a green economy in Greece”, OECD Economics Department Working Papers, No. 1757, OECD Publishing, Paris, https://doi.org/10.1787/77cd54d8-en.