Romania has made remarkable progress in converging toward OECD income levels over the past two decades, supported by deeper integration into global markets, substantial capital inflows, and wide‑ranging economic reforms.

by Katja Schmidt, OECD Economics Department

Romania has made remarkable progress in converging toward OECD income levels over the past two decades, supported by deeper integration into global markets, substantial capital inflows, and wide‑ranging economic reforms.

These forces have driven strong productivity gains (Figure 1), bringing labour productivity close to the OECD average. Yet significant untapped potential remains. Further boosting the productivity of domestic firms and integrating them more deeply into global markets would raise the domestic value‑added content of production and help the country move up the value chain. At the same time, realigning wage dynamics more closely with productivity growth – which wages have outpaced in recent years – will be essential to safeguard competitiveness and support sustained improvements in living standards.

The new 2026 OECD Economic Survey of Romania highlights four key priorities to increase the integration of domestic firms into global markets while supporting broader productivity gains:

Strengthening innovation capacities and digital intensity among domestic firms

Promoting human capital development and skills

Improving the business environment and market efficiency

Fostering infrastructure development.

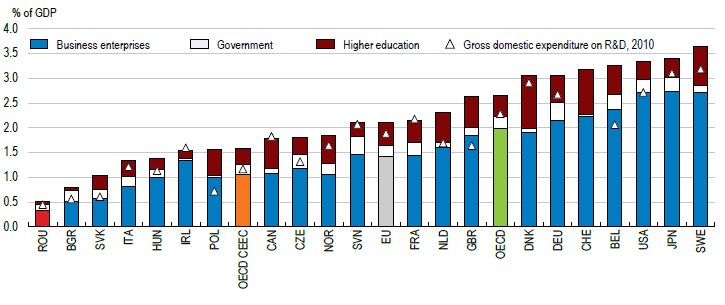

The innovation gap remains wide compared with both OECD and regional peers. Domestic firms continue to exhibit low rates of product, service, and process innovation, as well as limited R&D investment (Figure 2). Closing this gap requires measures to strengthen firms’ innovation capacities – for example, by simplifying access to R&D tax incentives and raising awareness of their availability. Innovation among SMEs could be further supported by making R&D tax incentives more effective, including through refundability so that any credit exceeding the tax liability is paid out in cash, and by establishing well‑defined public-private project opportunities that encourage SME participation in R&D. In parallel, improving firms’ access to finance and advancing financial deepening – including through more developed capital markets – will be essential to enable productivity‑enhancing investment, foster innovation, and support firm growth and scaling.

Romania’s digital infrastructure has improved significantly: access to high‑speed broadband is now approaching levels seen in the best‑performing OECD countries. However, digital intensity and the use of digital technologies by firms remain low. This reflects relatively low digital skills in the wider population, which should be strengthened as a priority. Awareness of and access to digital advisory and support schemes could also be improved. Ireland’s Grow Digital portal provides a useful example of good practice, consolidating support programmes, training and funding information, and a self‑assessment tool to help firms identify their digital needs.

Figure 2. Romania’s R&D spending is very low

Gross domestic expenditure on R&D, 2024 or latest available

Note: OECD CEEC is the non-weighted average of Czechia, Hungary, Poland, Slovak Republic, and Slovenia. Source: OECD Main Science and Technology Indicators database.

The economy’s productive capacity depends critically on the availability of advanced skills. As Romania moves up the value chain, demand for technical, digital, and managerial competencies is set to rise. Yet the country starts from a challenging position, with a high share of adults with low educational attainment, persistently elevated early‑school‑leaving rates, and comparatively weak learning outcomes. Addressing these gaps requires broad‑based reforms, as recognised in the 2023 education reform. Romania should focus resources on key priorities and ensure effective delivery – modernising curricula, strengthening teacher capacity, and investing in school infrastructure, particularly in disadvantaged areas. These efforts must be supported by sustainable and adequate financing, alongside a stronger focus on lifelong learning and continuous skills upgrading.

Fostering a dynamic, growth‑oriented business environment requires a regulatory framework that supports entrepreneurship, competition, and firm expansion. While Romania has made progress in improving the regulatory environment and market efficiency, further steps are needed. Starting and operating a business remains more burdensome than in top‑performing OECD countries, despite ongoing simplification efforts. Priority should be given to accelerating the implementation of the streamlined single industrial licensing procedure and strengthening the insolvency framework – including by improving the efficiency of court procedures and expanding the use of digital tools in insolvency cases. Further improvements in the efficiency and accessibility of public procurement processes are also required

Finally, the Survey highlights opportunities to further strengthen transport infrastructure, including by improving network connections, ensuring more efficient transport pricing, and enhancing road maintenance. Promoting alternative low‑emission transport modes and improving governance in the transport sector will also be essential to support sustainable mobility and improve overall system performance.

Convertir la incertidumbre global en oportunidad: Una agenda de competitividad para América Latina

Category: Argentina,Brazil,chile,Colombia,Costa Rica,Latin America,Mexico,Peru,Posts in Spanish

written by oecdecoscope | March 16, 2026

Por Jens Arnold, Aida Caldera, Priscilla Fialho, Paula Garda, Alberto González Pandiella, Michael Koelle, Alessandro Maravalle, Dimitris Mavridis, Claudia Ramírez yAdolfo Rodriguez-Vargas, OCDE.

El contexto global, marcado por una alta incertidumbre política y fragmentación, plantea nuevos desafíos para América Latina, pero también abre nuevas oportunidades para fortalecer su competitividad y reducir vulnerabilidades.

Se espera que el PIB en América Latina crecerá 2.1% en 2025 y 2% en 2026, lo que refleja una desaceleración generalizada en la región. Estas cifras son más bajas que las previstas a fines del año pasado y se sitúan por debajo del promedio de otras economías emergentes. Aunque se espera una fuerte recuperación en Argentina, el crecimiento se mantiene débil en la mayoría de los países, con revisiones a la baja para Brasil, México y Colombia (Tabla), en un contexto generalizado de una débil demanda externa y la alta incertidumbre.

Cuadro. Perspectivas económicas para los países de América Latina

Nota: América Latina 7 es la media ponderada por el PIB a valores de paridad del poder de compra de los 7 países en la tabla para el PIB. América Latina 6 es la media simple de los países incluidos en el cuadro para la inflación excluyendo a Argentina. Fuente: OCDE Perspectivas Económicas No. 117, junio de 2025.

La desinflación avanza, pero persisten las presiones inflacionarias. La inflación se mantiene por encima del objetivo en muchos países. En cambio, Argentina ha logrado avances significativos gracias a una combinación de consolidación fiscal y una política monetaria más restrictiva. Con la excepción de Argentina y Brasil, los bancos centrales de la región deberían continuar con su flexibilización monetaria prudente y gradual para asegurarse que la inflación se acerque al objetivo, manteniéndose alerta ante riesgos de salidas de capitales y nuevas presiones inflacionarias.

Los riesgos para las perspectivas son a la baja. Un aumento de los aranceles comerciales y menor dinamismo al previsto en socios comerciales clave podría debilitar aún más las exportaciones y presionar a la baja los precios de las materias primas. Los costos comerciales podrían ralentizar más de lo esperado la desinflación en las economías avanzadas y prolongar tasas de interés globales más altas. Una elevada deuda pública y unas condiciones financieras globales más restrictivas de lo previsto, podrían retrasar la tan necesaria inversión. Si se intensifican las salidas de capital, los bancos centrales podrían tener menos margen de maniobra para flexibilizar la política monetaria.

Una agenda de competitividad para tiempos inciertos

En este complejo entorno global, la región necesita más que nunca mejorar sus políticas domésticas. Un área donde es posible avanzar, y urgentemente necesario, es en competitividad, comercio e inversión. Estas no son prioridades nuevas, pero los cambios globales en el comercio, las cadenas de suministro y la transición hacia economías más sostenibles aumentan su relevancia estratégica. Los países que ofrezcan estabilidad institucional, apertura y baja carga administrativa estarán mejor posicionados para atraer inversión y expandir sus mercados.

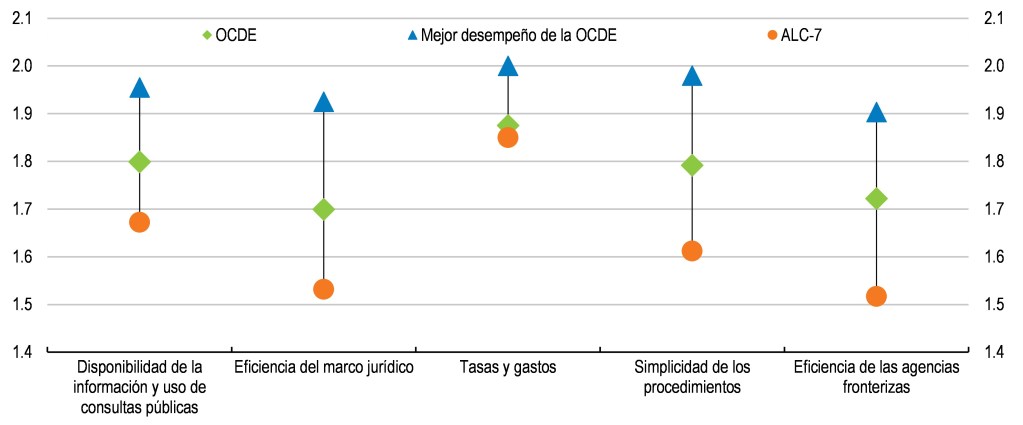

Mejorar los procedimientos aduaneros representa una oportunidad clara. Según los Indicadores de Facilitación del Comercio de la OCDE, América Latina aún enfrenta altos costos comerciales debido a procedimientos aduaneros complejos, inspecciones redundantes y poca coordinación entre agencias fronterizas (Figura). Hay amplio margen para mejorar el procesamiento, levante y despacho de mercancías, en particular mediante una mayor automatización y una mejor coordinación entre las agencias aduaneras, sanitarias, tributarias y otras agencias fronterizas. Medidas prácticas como la cooperación entre agencias de distintos países en la frontera, la agilización de los procesos judiciales y una mayor digitalización pueden beneficiar a los exportadores, especialmente a las pequeñas empresas, y atraer inversión. Además, estas medidas reducen los costos de operar formalmente, lo que incentiva a más empresas a salir de la informalidad.

Figura. Las políticas de facilitación del comercio pueden mejorarse en América Latina

2 = Mejor desempeño

Nota: Disponibilidad de la información y uso de consultas públicas es la media de los indicadores de la facilitación del comercio (TFI, por sus siglas en inglés) A y B. Eficiencia del marco jurídico es la media de los indicadores TFI C y D. Simplicidad de los procedimientos es la media de los indicadores TFI F, G y H. Eficacia de las agencias fronterizas es la media de los indicadores TFI I, J y K. ALC-7 es la media de Argentina, Brasil, Chile, Colombia, Costa Rica, México y Perú. Fuente: Estadísticas sobre los Indicadores de Facilitación del Comercio de la OCDE (TFI, por sus siglas en inglés).

La facilitación del comercio debe ir acompañada de reformas más amplias que fomenten la productividad. Impulsar la competitividad de las exportaciones y la productividad empresarial también requiere un entorno empresarial más dinámico, una mayor competencia doméstica, un mejor acceso a la financiación, más capacitación y capacidad de innovación. Estas reformas se refuerzan mutuamente: las empresas más productivas tienen mayor probabilidad de exportar, invertir y formalizarse.

El fortalecimiento de la integración regional sigue siendo relevante en América Latina, especialmente en un mundo donde las cadenas de valor están cambiando y los centros regionales cobran mayor importancia. El enfoque debe centrarse en la cooperación: mejorar la cooperación entre organismos fronterizos, el reconocimiento mutuo de normas, el intercambio de datos, los sistemas interoperables y el reconocimiento de estándares técnicos comunes. La región también cuenta con un potencial sin explotar en el comercio de servicios, gracias a idiomas compartidos y husos horarios similares; sin embargo, el comercio interregional de servicios sigue siendo bajo en comparación con los estándares mundiales.

América Latina debe adoptar una visión más orientada hacia el exterior. Acuerdos comerciales como el de la UE-Mercosur, y la participación en marcos plurilaterales como la Alianza del Pacífico o el CPTPP pueden ayudar a diversificar mercados de exportación, atraer inversión, fortalecer la participación en las cadenas globales de valor y aprovechar nuevas tecnologías. Sin embargo, para aprovechar al máximo los beneficios de estas iniciativas, los países deben mejorar su capacidad de implementación y garantizar la coherencia entre las políticas comerciales, de inversión y regulatorias.

América Latina cuenta con ventajas reales: vastas reservas de minerales críticos, abundante energía renovable, una fuerza laboral joven y cada vez más cualificada, y proximidad a mercados clave. Al impulsar reformas concretas que mejoren la competitividad, reduzcan las barreras comerciales y atraigan inversión de calidad, la región puede convertir los desafíos actuales en oportunidades y sentar las bases para un crecimiento más sólido y resiliente.

Referencias:

OECD (2025), OECD Economic Outlook, Volume 2025 Issue 1, OECD Publishing, Paris, doi – Reporte completo en inglés con las proyecciones macroeconómicas, los principales desafíos estructurales e información detallada por país.

Stepping up structural reforms to improve Egypt’s business climate

Category: Egypt,Private sector,Uncategorized

written by oecdecoscope | March 16, 2026

by Ania Thiemann, Economist and Competition Expert, Competition Division.

Egypt’s challenging business climate is holding back productivity and therefore also living standards. Labour productivity is still far below the OECD average (Figure 1), with low overall investment and a declining share of private investment in the total. Low investment in innovation, and research and development (R&D) also contributes to low productivity growth, as Egypt spends less than 1% of GDP on R&D. Market mechanisms, such as business entry and exit, and growth of the most efficient firms, appear to be weaker than in many similar emerging markets. Underlying these facts are deep-seated structural causes that impede market competition, investment and efficient resource allocation. These barriers stifle the country’s potential for long-term sustainable growth and restrict the development of a robust private sector. To ensure sustainable economic growth, as set out in Egypt’s National Structural Reform Programme, thorough policy reforms are required that can boost market competition. Regulatory and trade barriers, as well as a dominant state presence need to be addressed to revive private sector activity.

Figure 1: Low output per worker is related to low investment

Note: Data for Egypt in all three panels refer to fiscal years (from July of indicated year to June of the following year). Neighbouring countries refer to Algeria, Israel, Jordan, Lebanon, Morocco, Tunisia and Türkiye. Source: IMF, World Economic Outlook database – October 2023; OECD, National Accounts database; Ministry of Planning and Economic Development; and OECD calculation.

Removing regulatory barriers to enhance market entry and expansion

A central and long-standing challenge is the heavy regulatory burden that acts as a barrier to market entry and expansion, while also promoting informality. Complex and lengthy processes for obtaining business licenses and permits during the post-establishment phase constrain both domestic businesses and exporters (Figure 2). Despite recent reforms, the administrative load remains heavy, stifling Egypt’s business dynamism compared to regional and global averages, with comparatively low entry and exit rates. Moreover, overall regulatory quality remains low, reflecting lengthy and opaque decision-making processes and implementation.

Figure 2: Business licensing is a constraint on domestic businesses and exporters

Percentage of firms in Egypt identifying business licensing and permits as a major constraint, 2020

Note: Share of respondent firms out of 3075 firms surveyed. Source: World Bank, Enterprise Surveys.

To support a more dynamic private business sector, Egypt needs to streamline its business registration and licensing processes. Licensing requirements can be replaced by online registration in most cases, while a more efficient on-line application system would speed up processes. A new online platform for business registration was opened up in 2023, but difficulties remain with local permits. Simplifying procedures and reducing bureaucratic hurdles can encourage new business formation and attract more investment. Additionally, improving the transparency of administrative procedures would also reduce opportunities for corruption, which is a crucial step towards creating a fair and competitive market landscape.

Strengthening competitive pressures through trade and investment

High tariff and non-tariff barriers to trade mean that the Egyptian market remains relatively insulated from global competition. Such trade restrictions limit the country’s integration into global value chains and reduce the spillover benefits of foreign technology and know-how, which are essential for boosting productivity.

Liberalising trade policies and reducing tariffs can enhance Egypt’s competitiveness on the global stage. The creation of the National Single Window (Nafeza) to support external trade, should help speed up customs procedures. Border clearance has improved but remains comparatively slow (Figure 3). To support faster import release, the authorities are working on a new risk management system, which should speed up processes by reducing the number of inspections to those selected by the risk matrix. However, Egypt should also simplify its tariff regime, as tariffs remain high and unwieldy, with particularly high tariffs for agricultural products, and for products that compete with Egyptian manufactured goods (with tariff rates of 40-60%), in a system with 7 850 tariff lines. Foreign traders whose products already meet domestic standards should not have to preregister their products, and import licences could be replaced by a simple registration with the customs authorities, as is the case in Europe. A more open and predictable trade regime would benefit domestic businesses and investors, as well as supporting more inward foreign investment. This in turn would facilitate the transfer of technology and expertise, thus foster productivity growth.

Figure 3: High import tariffs and slow border clearance are hampering trade

Note: In Panel A, data for the countries presented refer to 2019 except for Thailand (2015), Tunisia (2016), Israel (2017), Mexico (2018), Jordan and Malaysia (2020). Weighted mean applied tariff is the average of effectively applied rates weighted by the product import shares corresponding to each partner country. When the effectively applied rate is unavailable, the most favoured nation rate is used instead. Source: World Bank, World Development Indicators; World Economic Forum (2019), Global Competitiveness Index 4.0.

Reducing the state’s footprint in the economy

State-owned enterprises (SOEs) play a significant role in Egypt’s economy, to the detriment of competitive market conditions by crowding out private sector activity. The government’s recent steps to level the playing field, though commendable, need to be more comprehensive and sustained. Over-reliance on SOEs in various sectors, such as utilities and transport, but also in manufacturing, prevents private enterprises from competing on an equal footing. Privatisation and divestment of SOEs should be pursued more aggressively to reduce the state’s dominance in the market. This move will not only improve efficiency but also stimulate private investment. The OECD’s guidelines on privatisation could serve as a valuable framework for Egypt in this regard.

Further actions to support private businesses: Access to finance and digital diffusion

Access to finance remains a significant hurdle for many businesses in Egypt. Banks overwhelmingly prefer to lend to the government, leaving private enterprises, especially small and medium-sized enterprises (SMEs), with limited financing options which hampers business expansion and innovation. Enhancing financial inclusion by opening up the banking sector to competition, notably by FinTechs with Open Banking regulation, can mitigate this issue. Policies aimed at improving the creditworthiness of SMEs and developing a robust microfinance sector will also support private sector growth. Improving digital financial services could play a critical role in this transformation.

Digital inclusion is key to boost productivity and competitiveness. However, Egypt lags behind in terms of digital infrastructure, and adoption by SMEs. The legal framework for digital business models needs significant improvement to allow for dematerialised businesses to expand. Investing in digital infrastructure and fostering a regulatory environment that supports digital innovation are therefore crucial steps to create a more vibrant business sector and help enhance overall economic efficiency.

References:

Thiemann, A. (2024), “Improving Egypt’s business climate to revive private sector growth”, OECD Economics Department Working Papers, No. 1808, OECD Publishing, Paris, https://doi.org/10.1787/a4b2ce91-en.

Maintaining and reinforcing achievements in Costa Rica

Category: Costa Rica,education

written by oecdecoscope | March 16, 2026

By Alberto Gonzalez Pandiella and Alessandro Maravalle, OECD Economics Department

Costa Rica has made remarkable economic progress over the past two decades, such as achieving life expectancy at par with the OECD average. Thanks to a strong commitment to trade, it has succeeded in attracting foreign direct investment and in increasing the level of sophistication of its export basket. However, the challenges to safeguard these achievements and further improve living standards are substantial. Growth prospects were deteriorating before the pandemic and going forward population ageing will take an additional toll (Figure). Unemployment is high, at a two-digit rate since 2018, as well as informality, affecting nearly half of the labour force. The fiscal situation improved in 2021 and 2022, thanks to the 2018 fiscal reform, but with public debt at around 70% of GDP, public finances remain a critical vulnerability requiring sustained efforts to contain spending and boost public sector efficiency. Nearshoring trends, by which companies seek reducing supply chain disruption risks by locating closer to their final markets, are providing new investment opportunities. Costa Rica is a front runner in environmental protection and renewables generation, and the global transition to net zero greenhouse gas emissions can further increase the country’s competitiveness.

The latest OECD Economic Survey (OECD, 2023) argues that continuing and stepping up structural reform efforts would be the best way for Costa Rica to respond to these challenges and seize new opportunities. Reforms to boost productivity are particularly critical to uphold growth in GDP and living standards. Strengthening competition is especially a promising avenue to boost productivity. Weak competition tends to translate into relatively high prices of goods and services for consumers and firms. Valuable and bold steps have been recently taken to boost competition in key markets, such as rice or professional services. Steps are also being taken in cooperation with the private sector to reduce regulatory burden, by identifying regulations and procedures susceptible to be phased out, including also specific deadlines for their elimination. Providing the national competition authority with the budget granted by law is a pending challenge that would be particularly beneficial at the current juncture when measures to improve regulations and open up key sectors of the economy are being taken. Effective competition authorities, by promoting stronger economic growth, can also have a positive fiscal impact by supporting higher tax revenues.

Informality, at around 45% of total employment, remains high and is both a cause and a consequence of low productivity. A comprehensive strategy is required to reduce it, with actions needed in several policy areas, such as reducing non-wage labour costs, facilitating the creation of formal firms, including by reducing the bureaucratic and economic cost of establishing a formal firm, helping more Costa Rican to acquire the skills needed to access formal jobs, simplifying taxes and enhancing enforcement mechanisms. Experience in some OECD countries, such as Colombia, indicates that reducing non-wage costs, by cutting employer payroll charges, can help to reduce informality. Employer payroll charges in Costa Rica are high in comparison with the OECD average, indicating that there is ample room to move in this direction.

Virtually universal health care and primary education and one of the highest pension coverage in the region have led to remarkable social outcomes. However, Costa Rica faces substantial social challenges, such pas poverty remaining largely unchanged at around 20% over the last 25 years and increasing income inequality. There is room to improve social programmes targeting, as in some cases more than 40% of the beneficiaries are middle and high-income households. There is also room to reduce fragmentation, as 21 institutions are in charge of delivering more than 35 schemes. Better targeting and lower fragmentation would facilitate reinforcing social protection in key areas and reduce inequality.

Improving the quality and efficiency of education and training is also key to support growth and equity in Costa Rica. Even if spending on education is high in Costa Rica, where it amounts to more than 6.5% of GDP, one of the highest shares across OECD countries, educational outcomes remain poor and educational exclusion is still high, with too many Costa Ricans leaving school without an upper-secondary education. A more targeted support to students with learning gaps, improving teachers’ selection and training and expanding access to education to children below four years would help increase equity of opportunities and help more Costa Ricans access better paid formal jobs and firms fill easier their vacancies.

Figure. Without reforms the economy’s growth potential will fall as the demographic bonus fades

Walking in modern-day Seoul, you are easily struck by its modernity. You do not even have to go there if you own a Samsung smartphone, drive a Hyundai, listen to BTS (which recently announced a break) or Blackpink, watch Squid Game or Extraordinary Attorney Woo. It is hard to fathom the speed at which Korea has travelled the long road from poverty and devastation following the Korean War to strength and prosperity, with per capita GDP rising above the OECD average in 2020 (Figure 1). Since the 1960s, income growth and access to health care pushed life expectancy well above the OECD average, accompanied by an equally impressive transition from authoritarian rule to vibrant democracy. The 2022 OECD Economic Survey of Korea tells the tale of present strengths and skilful governance, but also points to current and future challenges which are to an extent rooted in Korea’s export-oriented growth strategy and its rapid ascent from poverty to prominence.

Figure 1. Rapid development and great economic success

GDP per capita, constant 2015 prices and PPPs

Source: OECD National Accounts Database.

Sound economic policies

In the recent past, skilful health management steered the country through the pandemic relatively unscathed, with a world-leading tracing system implemented early in spring 2020 and a vaccination campaign carried out with speed and efficiency. Building on a tradition of sound economic management, supportive policies protected people and businesses from hardship and bankruptcy. The strong exporting sector helped the economy rebound. The recovery is set to continue as pandemic-era restrictions on contact-intensive services are shelved, despite the Russia-Ukraine war raising inflation and highlighting the need to boost supply chain resilience.

K-ETS should be Korea’s best friend to reach climate pledges

Korea has committed to reducing emissions by 40% from the 2018 level by 2030, and to net zero by 2050. Its exporting sector and electricity generation are emission intensive, pointing to a challenging transition. However, this also leaves room for relatively low-cost emission reductions with considerable co-benefits from cleaner air. Korea’s emission trading scheme (K-ETS) was the first in East Asia and should be recognised by policymakers as the best tool to reduce emissions as much as possible at a lowest possible cost. K-ETS puts a price on carbon from a large share of emissions, but too many allowances are handed out for free and its overall emission limit is not yet aligned with the new and more ambitious emissions reduction targets. Deregulation is needed to allow the carbon price to pass through to electricity producers to actually incentivise emission reductions in this important sector.

Productivity gaps are mirrored in income, social protection and working conditions

Export-led growth and the nurturing of large exporting companies laid the ground for considerable and persistent productivity gaps to smaller companies. Large firms typically offer highly educated workers well-paid jobs, good working conditions, regular employment and social insurance coverage, but their share of employment has fallen as production has been automated and moved offshore. Low-productivity SMEs hire a larger share of non-regular workers, who earn less and are less protected. These firms find it hard to attract the skilled workers needed to boost productivity, for example by adopting digital technologies. A large number of policies have been put in place to support SMEs, including subsidies, favourable access to public procurement, regulations differentiated by company size, and even whole market segments reserved for SMEs. Each policy may have some justification if seen in isolation, but they sum up to a system that supports the survival of low-productivity firms against a backdrop of regulatory complexity.

Youths’ struggle for a golden ticket is unproductive

Korea’s high level of human capital is fundamentally a strength, but important aspects of the current status quo are unproductive. Entering a top university increases the chance to land a secure and attractive career in a large firm or the public sector rather than in a low-productivity SME. Competition is therefore fierce to score highly on the university entrance exam. This Korean “Golden ticket syndrome” has several negative effects, including low youth employment, a lot of time and money spent on private tutoring (hagwon), skill and qualification mismatches, high pressure on students and low life satisfaction.

Korea needs more children and more working moms

Over the past few decades, education and access to jobs have become increasingly equal between genders. The large-scale roll-out of publicly-funded day care and kindergartens has raised enrolment rates to the level of Nordic countries, but working life and social norms have not kept pace. Combining career and children is often not an option when facing norms and expectations based on traditional gender roles, and long working hours and limited flexibility in the workplace. Mothers returning to working life tend to find that only low-paid non-regular jobs are available. Young women therefore postpone family formation and have fewer children over their lifetime (Figure 2). This has put Korea on the path to rapid ageing which will lead to fiscal and labour market pressures going forward.

Figure 2. Women postpone childbirth

Source: OECD Economic Surveys: Korea 2022.

Work in progress

Building on its considerable strengths, Korea should harness the economic dividends of equal opportunity and fair competition to reduce productivity gaps, thereby narrowing gaps in pay and social protection and reducing the pressure to win a golden ticket. Wise climate policies can contribute to productivity and help secure equal opportunities for future generations. Making the workplace friendlier to both women and men along with a continued drive by the government to lead by example, facilitate the combination of career and family and change gender norms could lead to more children, more working moms and happier people.

By Piritta Sorsa, Jens Arnold and Paula Garda, OECD Economics Department

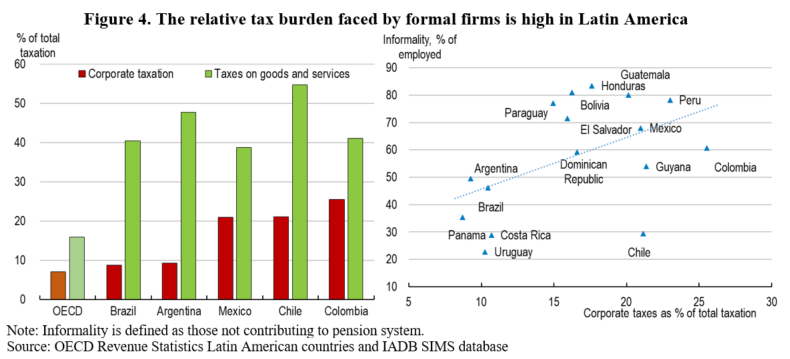

Why is growth persistently low and so unevenly distributed in emerging Latin America compared to emerging Asia despite a huge potential? Potential growth is ranging around 2-3% in the region. Some refer to dependence on commodities, poor education, weak business environments or corruption as possible causes. But the question is deeper and more complex. A crucial factor for Latin America is low productivity, often related to a poor use of available resources. Across the region, many workers and significant amounts of capital are stuck in activities that are not efficient. The reasons for this are many, but two important forces stand out: high informality and weak competition.

High and persistent informality in the region leaves workers more vulnerable and deprives them from social protection, thus contributing to inequality. For example, old age poverty in Colombia is high as low-skilled workers spend much of their working lives in informal employment, without pension contributions (OECD, 2019[1]). In Brazil and Argentina, informal workers retire later than others for the same reason, until they eventually reach the age to benefit from a non-contributory pension (OECD, 2019[2]; OECD, 2018[3]). In Mexico, poverty and informality are highly correlated among regions (OECD, 2019[4]). Informality also tends to maintain companies small with often low productivity as growing would face high costs of formalisation. Indeed, informal-sector productivity in the average LAC country is only between 25 and 75 percent of total labour productivity, and productivity decreases as informality rises (Loayza, 2018[5]). Informality also reduces the tax base for corporate and personal income taxes, reducing the capacity of the public sector to boost productivity and reduce inequality, and requires a higher tax burden on larger formal companies.

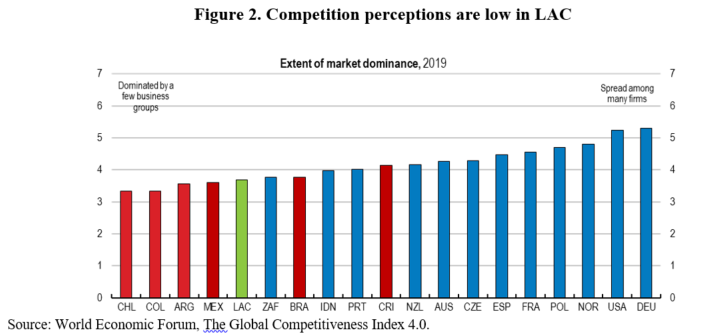

Weak competition is a second reason behind low productivity and is often reflected in high concentration (Figure 2). Entry barriers can protect existing activities that have little future growth potential at the cost of new dynamic and productive firms. Weak competition creates rents and lowers the share of wages in value-added worsening income distribution. Higher prices for consumers reduce purchasing power, affecting disproportionally low-income households.

Reducing informality for productivity and equity

The causes of informality are multiple. Informality is often a consequence of high costs of hiring formal workers, both wage and non-wage, especially in relation to labour productivity, given low educational outcomes.

Where high informality and weak competition coincide, as is the case in many Latin American countries, the consequences for both growth and equity can be particularly severe. For emerging Latin America to grow stronger and better share the fruits of growth, dealing with informality and competition should be priority.

Labour informality is often caused by rigid labour regulation. High firing costs of workers can discourage formal-sector hiring and promote inequality (Loayza, 2018[5]; OECD, 2018[6]; Heckman and Pages, 2000[7]). In Mexico, a labour reform in 2012 reduced hiring and firing costs, introduced different models of contracting and brought changes to the resolution of labour conflicts. Formal salaried jobs increased in the aftermath (OECD, 2019[4]). Minimum wages can be high compared to productivity or average wages keeping most workers informal. In Colombia, the minimum wage is close to the median wage and two thirds of workers earn less than that (OECD, 2019[1]). High payroll taxes can also have a detrimental effect on informality rates (Bobba, Flabbi and Levy, 2018[8]). Antón and Rastaletti (2018[9]) show how lowering employer social security contributions could lead to a substantial increase of labour formalisation. At a minimum, lower employer contributions could be offered temporarily for hiring low-skilled workers that enter the formal sector for the first time (OECD, 2017[10]). Lowering payroll taxes in Colombia helped reduce informality after the 2012 reform (Kugler et al., 2017[11]; Morales and Medina, 2016[12]; Fernández and Villar, 2016[13]; Bernal et al., 2017[14]). While incentives are crucial, better enforcement also needs to be part of any formalisation strategy.

Cumbersome administrative barriers and high taxes can keep companies informal. Latin America stands out in this respect (Figure 3). The tax burden on formal companies is also high compared to the OECD and positively associated to informality rates (Figure 4). To promote formalisation, regulatory and tax systems should be simple, with gradual increases in the tax burden as firms grow, so as not to discourage growth, and keep marginal tax rates as low as possible (Loayza, 2018[5]). These characteristics are crucial to encourage investment and employment in growing and larger companies.

Many countries in the region have implemented simplified schemes and reduced costs for small taxpayers with the aim of reducing informality. For example, Mexico introduced a special simplified regime for SMEs (Regimén de Incoporación Fiscal, RIF) in 2014, which induced 1.5 million informal firms to join the tax system (OECD, 2018[15]). In Brazil, a special tax regime for microenterprises (Microemprendedor Invididual, MEI) reduced the cost of formalisation and contributions to social security as of 2008. This regime helps explain the rising formalisation of the self-employed, including of women (OECD, 2012[16]). In Argentina, a simplified tax regime called Monotributo helped formalise self-employed workers. In Colombia, the tax reform in 2018 introduced a new simplified tax scheme (Simple) for small firms, and there are signs of positive impact on firm formalisation during 2019. At the same time, these regimes have to be designed carefully. When participation thresholds for special SME tax regimes are set too high, the effectiveness for formalisation declines while fiscal cost and threshold effects rise, as in the case of Brazil’s Simples Nacional (OECD, 2018[3]). At times, simplifying the general tax regime may be preferable over creating exceptions.

Education and skill levels are also linked with informality. Countries with lowest informality rates tend to have significantly higher levels of human capital (Docquier, Müller and Naval, 2017[17]). It is not a coincidence that the decrease in informality over recent decades in Latin America went hand in hand with steady progress towards universal education. Evidence shows that improvements in education have been an important driving force behind falling informality in Colombia and Brazil (International Monetary Fund, 2018[18]; OECD, 2018[3]).

Increasing competition for productivity and equity

In Latin America, the same complex rules that discourage formal job creation often coincide with overly strict regulations that stifle competition. Competition is affected by how easily firms can enter or exit markets, by the extent of license requirements for starting or expanding a business and by competitive pressures from imports. Relatively high trade protection adds to this in a number Latin American countries, shielding domestic producers from international competition (OECD, 2018[3]). All of this tends to raise prices for consumers and keep resources in low-productivity activities where informality is widespread, for both workers and firms.

These circular relationships suggest that it is important for the public sector to take stock of burdens that even well-intended regulations and codes can impose on private activity. Disincentives for firms to go formal will inevitably preclude workers from the benefits of formal jobs, while unnecessary barriers to competition will keep more jobs in activities with limited potential for productivity and wage growth. To foster formal job creation, all parts of a country’s regulatory framework should be simple and clear, promote competition, and facilitate both market entry and exit of firms (Loayza, Oviedo and Serven, 2005[19]).

Getting there

A comprehensive strategy is needed to deal with both informality and competition. It involves simplifying labour regulations, keeping administrative burdens and license requirements for companies as easy as possible, facilitating market entry and reducing trade barriers. Bringing more workers and firms into the formal sector would bring about broader social and labour protection, fairer wages, a more even tax burden and higher potential growth. Many of these policies are politically difficult as they involve dealing with vested interests and require appropriate sequencing. But that is not an excuse for inaction. These reforms should be accompanied with training and other active labour market policies for affected workers, as the informal sector often fulfils the function of absorbing excess labour supply, especially during transitions or economic recessions. Reforms to improve quality and relevance of education to raise worker productivity and policies that can raise investment and boost firm productivity should be also part of the strategy.

References

Antón, A. and A. Rasteletti (2018), Imposición al trabajo en contextos de alta informalidad laboral: Un marco teórico para la simulación de reformas tributarias y de seguridad social, Inter-American Development Bank, Washington, D.C., http://dx.doi.org/10.18235/0001467.

Bernal, R. et al. (2017), “Switching from Payroll Taxes to Corporate Income Taxes: Firms’ Employment and Wages after the Colombian 2012 Tax Reform”, IDB Technical Note, No. 1268, Inter-American Development Bank.

Bobba, M., L. Flabbi and S. Levy (2018), “Labor Market Search, Informality and Schooling Investments”, Interamerican Development Bank, https://publications.iadb.org/en/publication/12928/labor-market-search-informality-and-schooling-investments.

Docquier, F., T. Müller and J. Naval (2017), “Informality and Long-Run Growth”, The Scandinavian Journal of Economics, Vol. 119/4, pp. 1040-1085, http://dx.doi.org/10.1111/sjoe.12185.

Fernández, C. and L. Villar (2016), “The Impact of Lowering the Payroll Tax on Informality in Colombia”, No. 72, Fedesarrollo, http://hdl.handle.net/11445/3300.

Heckman, J. and C. Pages (2000), “The Cost of Job Security Regulation: Evidence from Latin American Labor Markets”, NBER working paper, No. 7773, National Bureau of Economic Research, http://dx.doi.org/10.3386/w7773.

International Monetary Fund (2018), “Colombia: Selected Issues”, Country Report, No. 18/129, http://www.imf.org.

Kugler, A. et al. (2017), “Do Payroll Tax Breaks Stimulate Formality? Evidence from Colombia’s Reform”, NBER Working Paper Series, http://www.nber.org/papers/w23308.

Loayza, N. (2018), “Informality : Why Is It So Widespread and How Can It Be Reduced?”, Research and Policy Briefs, No. 20, World Bank, http://documents.worldbank.org/curated/en/130391545228882358/Informality-Why-Is-It-So-Widespread-and-How-Can-It-Be-Reduced.

Loayza, N., A. Oviedo and L. Serven (2005), “The impact of regulation on growth and informality – cross-country evidence”, Policy, Research working paper World Bank 3623, http://documents.worldbank.org/curated/en/212041468134383114/The-impact-of-regulation-on-growth-and-informality-cross-country-evidence.

Morales, L. and C. Medina (2016), “Assessing the Effect of Payroll Taxes on Formal Employment: The Case of the 2012 Tax Reform in Colombia”, Borradores de Economia, Banco de la Republica, http://www.banrep.gov.co/en/borrador-971.

Laurence Boone, OECD Chief Economist, Chiara Criscuolo, OECD Science and Technology Directorate, and James Mancini, OECD Directorate for Financial and Enterprise Affairs

Digital technologies have the potential to bring huge

benefits in terms of productivity, jobs and ultimately living standards. At the

same time, consumers will gain access to new, innovative, and cheaper products.

However, for digitalisation to bring benefits to all firms and citizens, we

need a healthy competitive environment, which encourages and diffuses innovation, and helps bring the

gains from technology to people.

There is a growing debate in the media and among

policymakers about how competition is functioning in digital markets, with a

focus on market power, concentration and data protection, among other concerns.

The OECD’s analysis is beginning to shed light on this important issue, and

develop policy options to harness the benefits of digitalisation.

To start with, let’s recall what makes digital markets

unique and shapes the business models and competitive dynamics in digital

sectors. These characteristics include:

Substantial network effects in platform markets, meaning that as the number of users grows, the value of a platform to users increases.

Low variable costs and high fixed costs, meaning that there are significant economies of scale and scope in digital markets.

Data from users playing an increasingly important role as an input and competitive asset. New firms may find that data constitutes a substantial barrier to entry in digital markets, and consumers may not be fully aware of the data collected when they use online services.

These characteristics can result in a small number of firms

holding very high market shares and potentially dominant positions in some

digital markets.

However, it is important to recognise that a firm having a

large share of a given market is not automatically a cause for concern. In

fact, it may simply be the reward for having the most innovative ideas, or

attracting the highest number of users to increase the usefulness of a digital

platform. As long as the large market share is not defended through

anticompetitive conduct, and the market is accessible enough for new entrants,

the market can function well.

However, there are some signs that markets are becoming less

dynamic than before

First,

the OECD and others have found that mark-ups (defined as the ratio of unit

price over marginal cost) charged by firms are increasing. This could be an

indicator that competitive intensity is weaker than before.

Second, there is evidence that fewer start-ups are being created, particularly in the digital sector, which also has implications for the entrenchment of large firms, as shown in Figure 1 below.

Third,

there has been an acceleration of M&A activity that focuses on digital

firms (see Figure 2 below). Many mergers can have broadly procompetitive

benefits, for example in terms of innovation. But there is concern about

transactions involving small start-ups that are not captured by competition

authorities, and which may have anticompetitive effects.

Fourth,

there are signs that the largest firms are earning an increasing share of

revenues. While revenue concentration is not a very meaningful indicator of

competition on its own, in combination with the other evidence above, it may

suggest that something is changing about competitive dynamics in markets.

The OECD is working to understand

the implications of these findings, especially the role of digitalisation. There

is currently no single “smoking gun”, whether technological entry barriers,

regulatory distortions to competition, or firm misconduct. A variety of factors

may be at play.

In the meantime, policymakers can take

steps to address competition risks in digital markets.

First, there are opportunities to strengthen competition law enforcement. Agencies may need to adjust merger notification thresholds to ensure they capture potentially anticompetitive acquisitions of digital start-ups. They will also require vigilance in assessing merger harms associated with dynamic competition (i.e. effects on potential future competition) and innovation, as well as addressing potential abusive conduct by firms. Ex-post assessments of merger decisions can also help authorities review the analysis and tools used in past cases in order to draw lessons going forward. Authorities may also need additional tools to analyse and detect novel forms of firm misconduct, such as algorithmic collusion.

Second, we need to consider whether

current legislative frameworks are themselves contributing to problems

regarding digital competition. For example, the OECD is adapting its

Competition Assessment Toolkit to assist policymakers in identifying regulatory

barriers to competition in digital sectors. The adapted toolkit for digital

markets will be released later this year.

Third, new policy solutions may be

needed to protect and promote competition in digital markets, such as data

portability measures. Such measures could potentially help innovative new firms

overcome the barriers to entry associated with data, and empower consumers by

reducing switching costs. New business models could emerge that involve paying

consumers for their data, allowing them to share in the value generated by

their online activities.

Consumer and data protection

regulators can also address growing consumer concerns about digital firms while

at the same time promoting competition. This can include clarifying the rights

consumers have, and ensuring that they are given meaningful opportunities to

exercise those rights through fair contracting standards and default options

Fourth, competition authorities can

strengthen cooperation with international counterparts given the global scale

of many digital businesses. Investigation and advocacy cooperation is also

needed with consumer protection and data protection authorities, who may be

dealing with overlapping concerns. The OECD has a range of resources for

competition authorities on emerging digital

competition issues, assessing

their past decisions, and using non-enforcement

tools.

More broadly, policymakers must

ensure that the fundamentals are in place for new businesses to succeed, namely

by ensuring the right skills mix in the economy, keeping administrative burdens

to a minimum, and promoting broadband internet access.

OECD will be jointly hosting with the French Ministry of the Economy and Finance, and the French Autorité de la concurrence, a conference exploring many of these issues on June 3, 2019. The conference, Competition in the Digital Economy, will be webcast, and available to watch during and after the event here.

by Antoine Goujard, Chile Desk, Economics Department

Chile’s export growth has disappointed over the past two decades. In particular, exports of goods and services – in volume – have only grown at 1.1% annually over 2009-17 and at around 2.0% for non-copper products and services, compared to 4.2% in the average Latin American country (Panels A and B).

Chile’s weak export performance reveals structural weaknesses. Beyond copper and copper-related products that are highly dependent on external demand, export growth has been weak in manufacturing and services sectors. At the same time, with low investment in innovation and skills, productivity gains have stalled (Panel C). Exports remain mostly natural-resource based (Panel D) and highly concentrated across products, firms and destinations, with SMEs participating little in international trade.

To enhance inclusive growth potential decisive policy efforts are needed to improve productivity and competitiveness, and broaden the export base. The 2018 OECD Economic Survey shows that while the implementation of the 2014-18 Productivity Agenda and measures to raise the efficiency of electricity markets have been positive steps, more efforts are needed to raise productivity in four key areas:

Strengthening competition. Perceived market dominance that tends to reduce efficiency and raise rents, is among the worst in the OECD. Competition is limited in key sectors, such as telecommunications, maritime services and railways. The recent strengthening of the competition framework is welcome, but systematic reviews of competitive pressures are needed. Moreover, the guidelines issued by the OECD (2016b) should be used to review existing regulations from a competition perspective according to a set schedule, and pro-competitive and streamlining measures should be implemented rapidly.

Simplifying the business environment. Administrative procedures, such as licenses and permits, are burdensome, notably for smaller and younger firms complicating entry of new businesses. Streamlining unnecessary and complex regulations would allow substantial productivity gains. Improving the digital procedures for firms (Escritorio Empresa), and focusing on ex-post controls for businesses that have low associated sanitary and environmental risks, would ease firm creation and growth. On the trade side, simplifying regulations of preferential trade agreements would help SMEs to go global. Going forward, the regulatory process should build on all stakeholders and strengthened ex-ante and ex post evaluations such as the new productivity assessments (OECD, 2016a).

Increasing innovation and skills.Business investment in R&D and innovation is particularly weak, while entrepreneurial and managing skills are low and unequal. Increasing public support for R&D and innovation, and strengthening its evaluation, would help develop public-private links and ease R&D financing for SMEs. Additional technical assistance and mentoring for young and smaller firms, building on the recent Centros de Desarrollo de Negocios, would also support firm growth, innovation and access to export markets.

Improving logistic and digital infrastructure. Investment in intermodal connections, railways and digital networks is needed to bridge connectedness gaps (OECD, 2017b). Developing national and local infrastructure strategies, integrating the regulation of public and private ports and better accounting for environmental damages in transport taxes and road pricing would ensure money is well spent. Fully integrating the single window mechanism for exports and imports (SICEX) with the domestic logistic infrastructure and with regional partners would deliver significant synergies and gains for exports.

Goujard, A. (2018), “Boosting export performance in Chile”, OECD Economics Department Working Papers, forthcoming, OECD Publishing.

Will the inflation genie escape the bottle? New evidence on globalisation, competition and inflation

Category: international trade,Uncategorized

written by oecdecoscope | March 16, 2026

By Dan Andrews, Peter Gal and William Witheridge, Economics Department

Markets and commentators are speculating that there may be a sustained pick-up in inflation in the United States, after years of subdued price pressures. Along with continued solid US jobs growth and low unemployment, there are tentative signs of higher wage growth and the fiscal stimulus will also boost short-term growth. Global growth is also getting stronger (OECD, 2018a).

As well as these recent developments, longer-term worldwide trends which have kept inflation generally low since the mid-1990s may also be reversing. In particular, globalisation appears to have stalled since the crisis, aggregate demand in strengthening and output gaps have closed or are generally close to zero in most major countries. Moreover, there is mounting evidence of rising market power in services sectors. Together, these trends risk letting the inflation genie out of the bottle.

Declining inflation in many countries over the past few decades at the same time as rising global competition has led to a debate on the importance of globalisation for domestic inflation. Auer, Borio and Filardo (2017) at the BIS have argued that rising GVC integration has accentuated the importance of global factors – particularly global economic slack – for domestic inflation. However, recent research at the ECB (Tagliabracci, Osbat and Koester, forthcoming) and at the US Federal Reserve (Yellen, 2017) has disputed this conjecture.

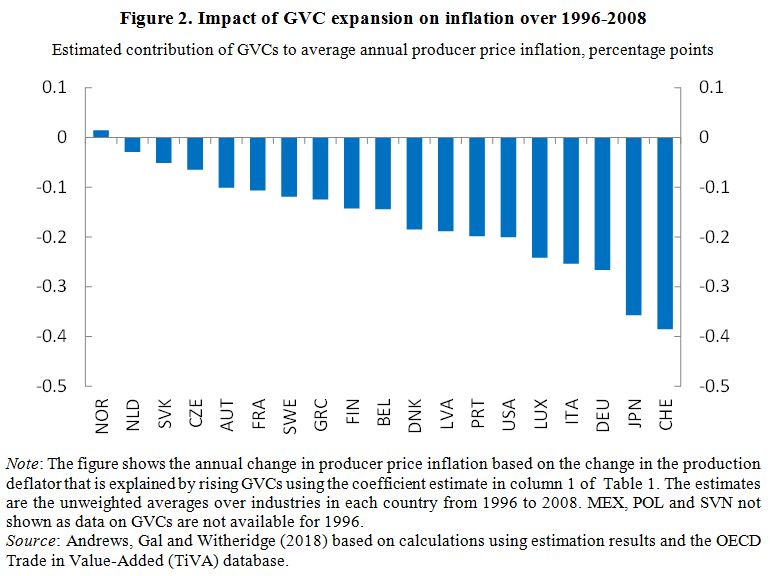

Figure 1 shows that global value chain (GVC) integration expanded significantly from 1995 until the crisis, while inflation remained relatively subdued. In the post-crisis period, GVCs flattened off and remained around the pre-crisis peak, while producer price inflation has fallen dramatically and remains very low on average across industries for our sample of countries.*

Motivated by this pattern, our new analysis of prices and globalisation (Andrews, Gal and Witheridge, 2018) goes beyond existing research by using recently released cross-country OECD data on prices and GVCs by industry, rather than at the country level, which allow us to control for time-varying country-specific and global shocks. We find that stronger Backward GVC Participation – that is, domestic producers relying more on foreign value added content – is associated with lower producer price inflation at the industry level. For example, we estimate that the rise in GVCs from the mid-1990s up to the crisis reduced annual producer price inflation by 0.15 percentage points on average, but this effect is more than double in some OECD countries (Figure 2).

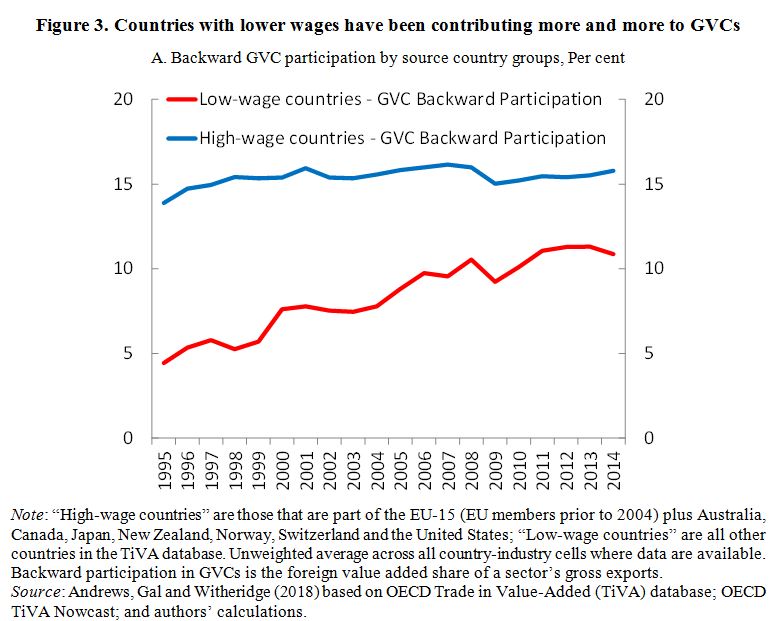

Confirming the existence of a cost-reduction and wage moderation channel, we also show that higher backward GVC participation is associated with lower wages and rising productivity in the importing countries and industries, especially when low-wage countries are integrated in their supply chains. This channel is likely to have contributed to lower inflation in recent years as the structure of the source (i.e. supplying) countries in GVCs has moved increasingly towards low-wage countries (Figure 3), despite a stall in the overall level of GVC integration (Figure 1). Therefore, inflation in advanced economies could remain low if the composition of GVCs continues to shift towards low-wage countries.

Moreover, we find that a high level of GVC integration can also dampen producer price inflation by accentuating the impact of global economic slack on domestic inflation. This provides new industry-level evidence to support the finding of Auer et al (2017) who use aggregate data covering the pre-crisis period. We show this by using a similar approach combining bilateral industry-level GVC and national output gap data to measure changes in global slack over time.

This implies that weak global demand has a larger disinflationary impact when GVC participation is higher. For example, given our sample of countries facing an average global output gap of -1.5 per cent in 2014, we estimate that annual producer price inflation was on average 0.25 percentage points lower in 2014 than for 1996 GVC levels. This figure is more than 0.5 percentage points, however, for countries that experienced a particularly large rise in GVC participation. But with slowing expansion of GVCs since the crisis, coupled with stronger aggregate demand and output gaps closing in most countries, this could lead to greater inflationary pressures in the medium term.

The third longer-term trend posing an upside risk to inflation is declining competition and market contestability. We exploit harmonised cross-country firm-level data to show an increasing trend in mark-ups, which suggests rising market power in services sectors (Figure 4). This upward trend in mark-ups is consistent with other estimates for the United States (De Loecker and Eeckhout, 2017) and other OECD countries (Calligaris et al, 2018). In turn, in these market services sectors we find a significant positive correlation between producer price inflation and mark-ups within industries since the early 2000s. This leads us to conjecture that if market power continues to rise it may pose a further risk to letting the inflation genie out of the bottle.

This analysis suggests that the expansion of GVCs facilitated by trade liberalisation and advances in technology has put downward pressure on producer prices, with potential implications for monetary policy. Looking forward, a continuation of the stalling globalisation observed since the crisis poses an upside risk to future inflation. This provides a further reason to resist the rising threat of trade protectionism in the global economy.

In addition, if more intense competition in product and labour markets contributed to global disinflation in over recent decades (Rogoff, 2003), then it follows that waning structural reform ambition (OECD, 2018b) – against the backdrop of strengthening global growth – could lead to inflationary pressures. Given the growing importance of ICT-based activities in the economy, as well as evidence of increasing market power in those industries, policy efforts to adapt anti-trust and pro-competitive market regulations to the digital age will not only bring benefits to long-run productivity growth but will also be desirable from a monetary policy perspective.

Auer, R., C. Borio and A. Filardo (2017), “The globalisation of inflation: The growing importance of global value chains”, BIS Working Papers, No. 602, January.

Calligaris, S., C. Criscuolo and L. Marcolini (2018), “Digital and market transformations”, OECD Science, technology and industry working papers, forthcoming.

De Loecker, J. and J. Eeckhout (2017), “The Rise of Market Power and the Macroeconomic Implications”, NBER Working Papers No. 23687.

* The sample of countries are: Austria, Belgium, Czech Republic, Denmark, Finland, France, Germany, Greece, Italy, Japan, Luxembourg, Latvia, Mexico, Netherlands, Norway, Poland, Portugal, Slovenia, Slovak Republic, Sweden, Switzerland and the United States.

Unleashing private sector productivity in the United States

Category: Productivity,Uncategorized,United States

written by oecdecoscope | March 16, 2026

By Douglas Sutherland, Head of the United States Desk, OECD Economics Department

With the global economy mired in low- growth and no signs of strong acceleration, a lot of attention has been paid to the meagre pace of productivity growth in OECD countries. In the United States, the most watched indicator of productivity (nonfarm business productivity growth) decelerated about ¾ percentage point from 2009 to 2014 relative to the preceding 5-year period. This is not just the result of the crisis holding back investment. Productivity growth had already been slowing from the early 2000s.

Economic research reveals competitive markets stimulate productivity: faced with competitors, firms survive by becoming more efficient and bringing new products to the market. Competitive markets see a lot of firm entry and exit. However, this dynamism has declined: new firms are not being created as frequently as in the past (See figure, top panel) and the most productive of these firms are not growing as fast as they once did. This matters because advances in productivity typically result from the rapid growth of young dynamic firms. Instead, start-ups appear to be failing more often and the remaining firms are getting older with larger firms increasingly dominating markets (See figure, bottom panels).

When this happens, markets become more concentrated, with large incumbent firms gaining market power. This has many disadvantages because gains in productivity are not being passed onto consumers in lower prices or to workers in higher wages. Faced with these worrying trends, competition/antitrust policy needs to adapt. This is particularly the case in markets transformed by digitalisation, financial innovation and globalisation – such as e-commerce and those dependent on access to information. The decline in business dynamism sometimes comes from barriers to competition being erected by the States. For example, state-level prohibitions on municipalities creating their own fixed broadband networks have hindered the development of stronger competition in this sector. In other cases, States have blunted competitive pressure through imposing state-specific occupational licensing requirements.

Amongst other factors, changes to bankruptcy laws have also contributed to more sluggish business formation. Reforms in 2005 increased the cost of bankruptcy for failed entrepreneurs and made it more difficult for them to try again (see the recent Ecoscope blog on the importance of this for productivity growth). The reforms appear to have stymied the creation of sole proprietorships and partnership, particularly in States that do not exempt some of the entrepreneur’s assets from bankruptcy proceedings. Given the importance of bankruptcy for long-run prospects, a better balance needs to be stuck between supporting entrepreneurship and creditor rights.