First published on OECD Insights http://wp.me/p2v6oD-2vJ.

By OECD Statistics Directorate

Four hundred years after the death of Shakespeare there remain many misconceptions on what he wrote. Perhaps the most common concerns the adulterated quote above, which is actually a reference to why Romeo was a Montague rather than where Romeo was. In the same spirit of confusion, recent years have seen considerable debate about the causes of the productivity slowdown seen across OECD countries.

This year’s Productivity Compendium includes a special chapter that casts a spotlight on some of the potential villains stalking the stage, together with insights from the OECD Productivity Database, and frames the discussion under the umbrella of the Productivity Paradox: a reference to the fact that productivity has slowed during a period of significant technological change, increasing participation of firms and countries in global value chains and rising education levels in the labour force. Indeed, the advent of digital innovations such as Big Data was expected to have sparked off a new wave of productivity growth, similar to those seen in the past, for example, as a result of electrification in the early 1900s and the ICT wave in the 1990s.

However, this has not yet materialised, raising a number of still largely open questions, ranging from potential lagged effects of these new technologies, a thinning out of new ideas (Gordon, 2012) to a breakdown of the ‘diffusion’ machine (OECD, 2015), right through to measurement. Indeed, against a backdrop of increases in income and wealth inequalities, concerns have emerged that this may reflect a structural, and not a cyclical, slowdown, with consequential impacts on well-being and long-term growth; hence the theme for this year’s OECD Ministerial meeting and OECD Forum : “Enhancing Productivity for Inclusive Growth” www.oecd.org/forum.

Double, double toil and trouble (Macbeth: Act 4, Scene 1)

But whilst all of these actors may in part explain the recent post-crisis productivity slowdown, often overlooked in the debate is that the slowdown in productivity is not a recent affair, a fact that even Macbeth’s witches may have struggled to foresee. The OECD Compendium of Productivity Indicators 2016 reveals that productivity growth began to slow well before the crisis; trending down since the early 2000s in Canada, the United Kingdom and the United States and since the 1970s in France, Germany, Italy and Japan (Figure 1).

Download graphs and data in Excel

Part of this downward trend in labour productivity can be explained by slower growth in multi-factor productivity (MFP), lending some weight to the arguments that technological spill-overs and diffusions from ICT, and other new technologies may be lower than from earlier technology breakthroughs. But lower MFP growth is not the only source. In many countries the contribution of capital deepening has also declined significantly, particularly in recent years.

Nothing will come of nothing (King Lear: Act 1, Scene 1)

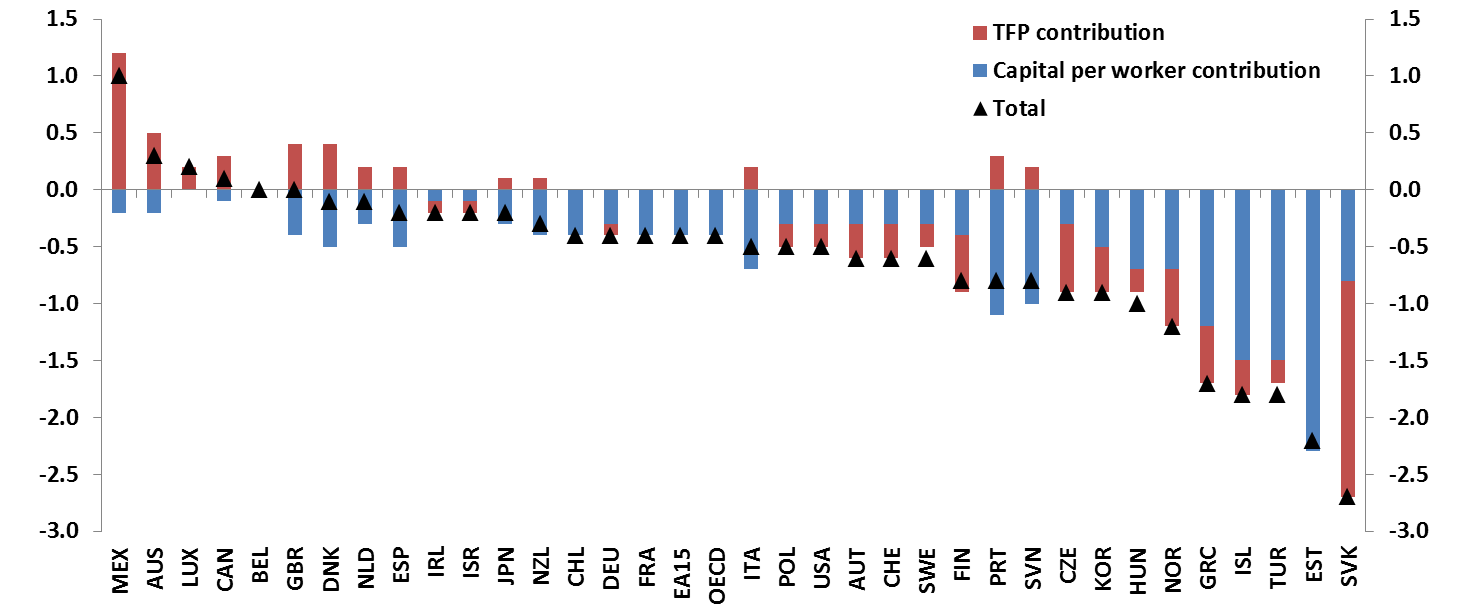

Although King Lear uttered the words above to his daughter Cordelia to solicit overt affection, his words are now typically used to illustrate that without investment, neither growth, nor indeed productivity, will follow. The Compendium shows, for example, that the direct contribution of information and communication technology (ICT) capital goods to productivity reached its peak in the late 1990s and has gradually waned since then, significantly so in most countries (Figure 2).

Download graph and data in Excel

And although the shares of ICT investment have held up reasonably well compared with other forms of investment, ICT investment as a share of GDP also remains below previous highs in many countries (Figure 3). Moreover, when measured and included, although knowledge based capital has held up better, it too has slowed in recent years and makes little change to the overall picture.

Download graphs and data in Excel

Truth is truth, to the end of reckoning (Measure for measure: Act V, Scene 1)

One suspect behind the slowdown, well versed in having to deal with the ‘slings and arrows of outrageous fortune’ is measurement. Indeed so prevalent is the view that measurement is at fault, particularly relating to the measurement of new disruptive (digital) technologies, such as Big Data, and business models, such as AirBnB and UberPop, it has been given its own acronym, MMH, the Mis-Measurement Hypothesis. The spread of digitalised applications has brought with it the provision of free services such as internet search capacity and media content and new business models, many of which are dependent on greater participation (i.e. labour input) by consumers. But the consumer’s activity remains (by and large) outside of the GDP production boundary, and the free services received are not captured as household consumption, raising questions about a missing ‘consumer surplus’ from GDP.

However, whilst it is clear that digitalisation may have compounded long standing measurement issues, in particular the measurement of price change and, so in turn, volume measures used in productivity measurement, and where efforts to improve measurement continue, the evidence increasingly suggests that the MMH is, at best, only partially true. Syverson (2016) for example shows that US GDP would have been around 15% higher in the third quarter of 2015 if the recent slowdown (post 2004) hadn’t occurred, swamping any potential unmeasured productivity growth and estimates of the consumer surplus, while Byrne, Fernald, and Reinsdorf (2016) show similar results. Ahmad and Schreyer (2016) further demonstrate that the GDP accounting framework is ‘up to the challenges posed by digitalisation’ and reinforce the distinction that needs to be made between GDP and welfare and indeed consumer surplus.

This is the short and the long of it (The Merry Wives of Windsor: Act II, Scene II)

In summary therefore the evidence suggests that the productivity slowdown is real and not a statistical phenomenon. True as this may be, it is also true that attempts to identify the causes of the slowdown can be greatly facilitated by improved availability or use of firm-level statistics in analyses, in particular on intra-firm transactions, and improved data on investment by type of asset, occupations, and skills. So, although statistics are not at fault they continue to provide the best route for a solution to the paradox and the key for policies that can restart the productivity engine.

The OECD Productivity Database

The OECD Productivity Database contains a consistent set of internationally comparable data on levels and growth rates of labour productivity, hours worked, employment, capital services, multifactor productivity and unit labour costs for OECD countries and Key Partners. It also includes growth measures of labour productivity, hours worked, employment and unit labour costs by main economic activity. These series, available from 1970 onwards for some countries, are updated on a daily basis.

Get real-time data at OECD Productivity Statistics (Database)

References

Ahmad, N and P. Schreyer (2016), “Measuring GDP in a Digitalised Economy”, OECD Statistics Directorate Working Paper, forthcoming.

Byrne D., J. Fernald and M. Reinsdorf (2016), “Does the United States have a productivity slowdown or a measurement problem?”, Brookings Papers on Economic Activity, BPEA Conference Draft, March 10-11.

Gordon, R. (2012), “Is US Economic Growth Over? Faltering Innovation Confronts the Six Headwinds”, NBER Working Papers, No. 18315.

OECD (2015), The Future of Productivity, OECD Publishing, Paris, http://dx.doi.org/10.1787/9789264248533-en.

OECD (2016), OECD Compendium of Productivity Indicators 2016, OECD Publishing, Paris, http://www.oecd.org/std/productivity-stats/oecd-compendium-of-productivity-indicators-22252126.htm.

Syverson, C. (2016), “Challenges to mismeasurement explanations for the U.S. productivity slowdown”, NBER Working Paper No. 21974, http://www.nber.org/papers/w21974.