by Catherine L. Mann, OECD Chief Economist, and Ken Ash, Director of the OECD Trade and Agriculture Directorate. This post was also published by the OECD Insights blog

Yesterday’s OECD Interim Economic Outlook warns that trade growth is slowing, contributing to another slowing of global GDP growth in 2016 and with few signs of improvement for 2017. Does it really matter? If we believe the current anti-trade, anti-globalisation rhetoric, we might shrug our shoulders and say “no”. Trade has been so maligned and demonised, some might even be pleased.

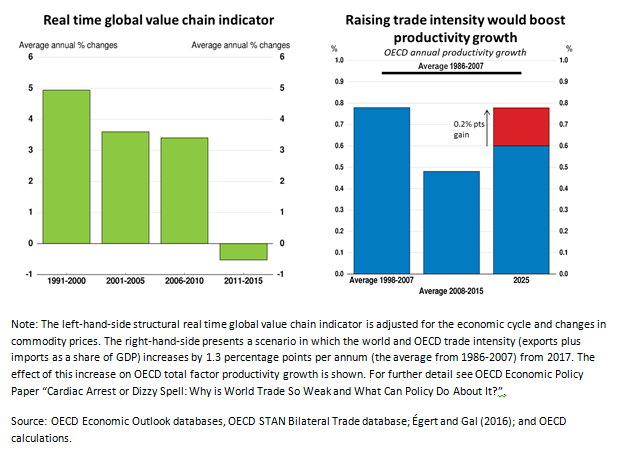

But that would be the wrong answer. Open trade and cross-border investment are key vectors for diffusion of new technologies and competition, which are central to achieving productivity gains and improving well-being. New research published yesterday by the OECD in conjunction with the Interim Economic Outlook suggests that a substantial part of the post-crisis slowdown in total factor productivity growth could be reversed if trade intensity were to recover. In short, weak trade is one of the factors that will keep the economy in a “low-growth” trap where sluggish trade and investment lead to diminished growth expectations and rising financial risks.

Over decades, trade has been responsible for drawing hundreds of millions of people out of poverty – and we mean one and two-dollar-a-day poverty – in emerging and developing countries. Trade could perform this same miracle for the many millions still living in abject poverty in poor countries in Asia and Africa, if other conditions are also right of course. Salaries and working conditions are almost always better in companies that trade than in those that do not, and this is true in countries at all levels of development. Households gain hugely from trade because it increases choice and reduces prices.

The prospects of millions of workers in the global economy depend on their participation in global value chains, as highlighted by statistics developed by the OECD with the WTO on Trade in Value-Added (TiVA). The main insight from these data is first, in order to export efficiently, a company has to also import efficiently. A second key insight is the importance of high quality services to support trade and trade-intensive activities. It should be of great concern that there are signs that the development of global value chains appears to have gone into reverse in recent years.

The OECD paper looks at the reasons for the trade slowdown and back-tracking in the development of global value chains. Several factors are at play, some of them cyclical in nature, others structural like the changing role of China in the global economy. Increasingly murky protectionism is contributing to the slowdown, as is the failure to implement any really ground-breaking global new trade initiatives for more than a decade. Without entering into a rather futile debate about when the slowdown really started or the exact contribution of structural versus cyclical drivers, let us instead ask what governments can do to reverse it.

The OECD Interim Economic Outlook calls for implementation of a package of measures to boost demand, including through collective fiscal action focused on raising investment and productive spending, and structural reforms. Removing barriers to trade and creating the conditions for people to reap the potential benefits of trade should be at the heart of the structural reform agenda.

First, governments should put their weight behind efforts to further lower trade barriers and unnecessary trade costs by implementing the Trade Facilitation Agreement, vigorously pursuing the reduction of restrictions on services trade, including by concluding the trade in Services Agreement (TISA), co-operating to reduce costly and unnecessary regulatory differences, concluding the Agreement on Environmental Goods, and by coming to the table to deliver a good result at the 11th WTO Ministerial Conference a little over a year from now. They should reduce remaining barriers to foreign direct investment. There are unilateral, bilateral, plurilateral and multilateral channels available if governments want to provide those growth opportunities that are currently lacking.

Second, governments need to step in to ensure that the benefits of trade are fairly shared. Governments should help those affected by the churn and disruption caused by globalisation. Benefits from trade are diffuse and long-term in nature. Losses tend to be sharp and very concentrated on individuals and regions. The people most affected are sometimes those with the least capacity to adjust. An unemployed steel worker does not take much comfort from knowing that programmers in Silicon Valley are thriving, or that T-shirts and smartphones are cheaper. What he or she needs is a decent job, new training and skills, and a robust social safety net to help through the transition.

Making trade work better for more people is not just about persuading them, although clearer and more honest communication is important. It is about ensuring that the full panoply of structural policies is put to work to ensure that people are able to reap the benefits that more open trade, technology, and investment will bring. This means paying attention to infrastructure, well-functioning financial markets, education and skills, clear and transparent institutions and rule of law – all the things that make an economy nimble Trade policy cannot be made in a vacuum but rather must be part of the fabric of domestic policies. If we are not able to do this, growing public scepticism, particularly in the most advanced economies, may mean that further market opening will be difficult, if not impossible. Such a result would impoverish many across the world.

References:

OECD Interim Economic Outlook, September 2016.

Haugh et al (2016), “Cardiac Arrest or Dizzy Spell: Why is World Trade So Weak and What Can Policy Do About It?” OECD Economic Policy Paper No. 18, September, OECD Publishing, Paris.