Italy’s reforms are paying off but challenges remain

By Mauro Pisu, Head of Italy Desk, Country Studies Branch, OECD Economics Department

Italy is recovering after a deep and long recession. Structural reforms, accommodative monetary and fiscal conditions, and low commodity prices have spearheaded the ongoing economic recovery. The Jobs Act and social security contributions’ exemptions jolted the labour market, leading to rising employment and higher consumer spending. Additional reforms in different areas, such as the school system, public administration, budget making process, banking system have been passed and implemented or are in the course of implementation. Greater focus has also been put on past reforms, with a sharp reduction in the backlog of decrees needed to implement them. The rejection of the constitutional reform by referendum in December 2016 has heightened political uncertainty but as discussed in the recently released OECD Economic Survey of Italy, the structural reform process must continue if Italy is to build a more inclusive and prosperous society.

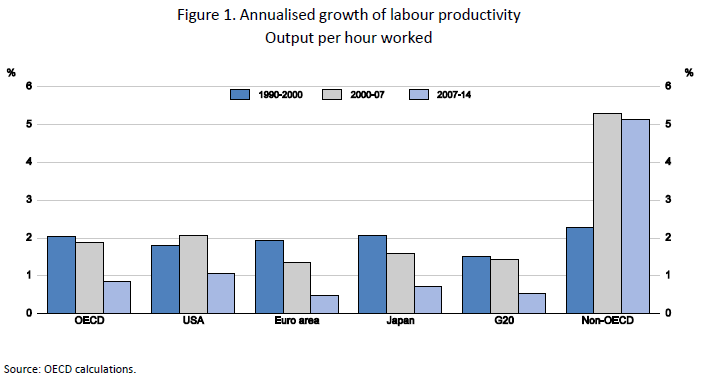

Despite the recent macroeconomic progress, the pace of the ongoing recovery remains modest (Figure 1). Productivity continues to decline and investment growth is weak. Public-administration inefficiencies, slow judicial processes, poorly designed regulation and weak competition still make it difficult to do business in Italy. Labour and capital resources are trapped in low-productivity firms, which hold down wages and well-being. Innovative start-ups and SMEs continue to suffer from difficult access to finance, especially through the corporate bond and equity markets. The Italian banking system features low profits and a large stock of non-performing loans, discouraging lending and investment.

Boosting investment is key to strengthening the recovery and increasing labour productivity. Raising investment will hinge on enhancing business dynamism, improving insolvency procedures, strengthening the innovation system and targeting innovation incentives towards innovative SMEs and start-ups. Restructuring the banking sector to improve governance and raise efficiency, and inducing banks to dispose of their bad debts, is key to restarting lending to firms.

The long crisis has eroded social inclusion, requiring renewed efforts to raise employment, reduce poverty, especially among youths and children, and improve skills. Strengthening further job creation, by lowering social security contributions, is crucial to increasing the employment rate, which, which despite recent improvements is still one of the lowest among OECD countries. Further progress on combating tax evasion, introducing a real estate tax based on updated cadastral value and cutting the numerous tax expenditures devoid of any economic and social rationale could offset the revenue lost by reducing social security contributions.

The crisis has also lead to sharp increase in poverty, especially among the young and children, which the weak economic recovery has not yet enabled to reverse (Figure 2). For instance, the absolute poverty rate of families with 1 or 2 children rose from 1.1 and 2.3% in 2006 to 4.9 and 8.6% in 2015. Over the same period, the absolute poverty rate among old people remained broadly stable. Ample empirical evidence has shown the large negative effects poverty experienced at young age has on school results as well as adult income and health status. It is of the utmost importance to implement the recently launched National Plan against Poverty, whose main aim is to establish a new nation-wide antipoverty programme (Reddito di Inclusione, REI). The allocated funds are still limited but are an improvement compared with the currently available resources. The government should ensure that the new programme is sufficiently funded to substantially reduce poverty among young children.

References:

OECD (2017), OECD Economic Surveys: Italy 2017, OECD Publishing, Paris.

.

.