Four Challenges of Inclusive Growth from the OECD’s chief economist

Category: finance,Inequality,Labour markets,Productivity,Uncategorized

by Catherine L. Mann, Chief Economist and Head of the Economics Department, OECD

- The challenge of measuring inclusiveness. A standard metric for measuring inequality is the Gini coefficient, which measures income distribution within an economy. But there are many other measures, such as distribution of income deciles, distribution of wealth, distributions of these by regions or by gender. These are all static measures, even if they change over time. On the other hand, the persistence of earnings across generations, e.g. income mobility, explicitly is a dynamic intergenerational measure. Which measure is best? Particularly as they deliver different rankings across countries. For example, the Canadian Gini is persistently higher than the French Gini. But, the metric of earnings persistence is much lower in Canada than than in France. Which country is more inclusive? For more metrics, see OECD: Measures of inequality, immobility

- Getting below the averages. Recent OECD research has found a wide gap in both productivity and wages between firms in each sector that are at the productivity frontier (in the top 5 percent, in productivity), where labour productivity has advanced some 35 percent since 2000, and the rest of firms in the economy, where labor productivity has increased less than 5 percent over the same period. The widening wage gap is reflected in the widening distribution of income across deciles where, among OECD countries, the real household disposable income of the bottom 10 percent remains some seven percent below the peak in 2007, the mean income is only on par, yet the top 10 percent has edged higher. Closing both the productivity and income gaps is a key element of inclusive growth. While the specifics of the policies to close these gaps differ by country, there are elements in the policy domains of business dynamics and competition, labour market functioning and skills, and financial market structure and performance. These policies, if deployed in packages, tend to work synergistically rather than present tradeoffs to achieve inclusive growth. For more on this topic, see the OECD: Global Forum on Productivity

- Getting finance right. OECD research shows that specific kinds of finance can undermine inclusive growth. Specifically, excessive mortgage debt increases the likelihood of a financial crisis, with deleterious outcomes for growth, and for equity, since those at the bottom of the income distribution are more likely to be at higher risk and higher exposure to this kind of debt and therefore to consequences of crisis. On the other hand, deeper equity markets contribute to growth; although, to the extent that equity wealth is unequally distributed, deeper equity markets favour the wealthier. OECD research also finds that otherwise identical workers, regardless of their income decile, are paid a wage premium if they work in finance. One reason is that too-big-to-fail rents are distributed partly to workers. For more on this topic, see OECD: Finance,growth, and inequality

- Globalization, technology, ‘tastes’ and regional impact on manufacturing jobs. How is the interplay of these factors relevant for inclusive growth? A decomposition of manufacturing job loss finds that changes in technology and ’tastes’ (that is, consumer preferences for services vs. goods) dominate the direct force of trade flows in the loss of manufacturing jobs. However, to the extent that manufacturing is regionally concentrated, the three factors together accentuate and concentrate jobs losses in those regions. Not surprisingly, countries with higher regional concentration of manufacturing jobs have tended to have experienced higher overall inequality. The policy approach to ameliorate this concentrated impact so that all can enjoy the benefits of globalization and technological change remains a critical task. For more on this topic, see OECD: Chapter 2 of the June Economic Outlook

This post also appears on the C.D. Howe Institute site

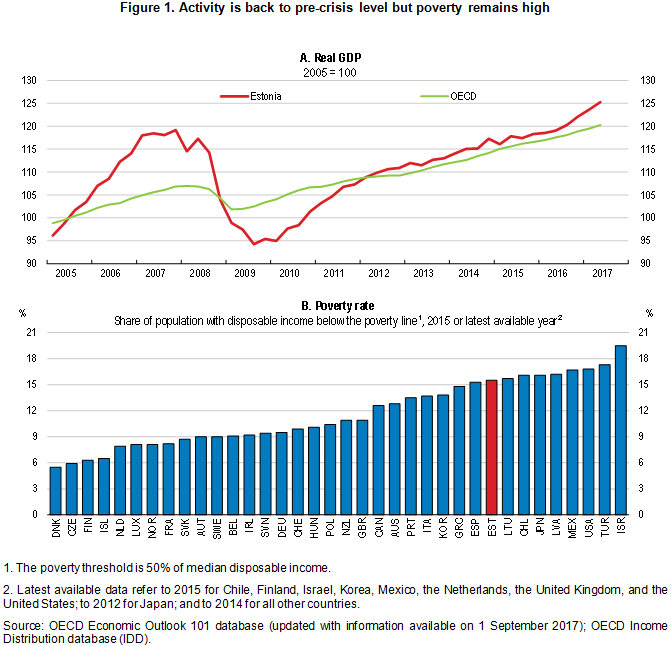

Important challenges remain. Productivity is lower than in other Baltic or central European economies and the gap with leading OECD economies remains large (chart A). Yet, productivity growth has slowed after the financial crisis, as elsewhere. To converge to the living standards of high income countries, Latvia has to reinvigorate productivity. As the

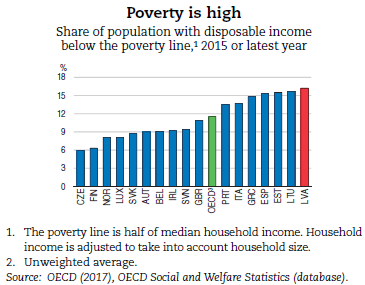

Important challenges remain. Productivity is lower than in other Baltic or central European economies and the gap with leading OECD economies remains large (chart A). Yet, productivity growth has slowed after the financial crisis, as elsewhere. To converge to the living standards of high income countries, Latvia has to reinvigorate productivity. As the  Poverty is among the highest in OECD countries (chart B) and is concentrated in some regions in part reflecting high unemployment. Lack of access to good and affordable housing makes it more difficult for low-income workers to move to well-paying jobs. Access to health services and higher education are also uneven and limit access to economic opportunities for low income households. Many young Latvians emigrate. These issues and policies to address them are analysed in the

Poverty is among the highest in OECD countries (chart B) and is concentrated in some regions in part reflecting high unemployment. Lack of access to good and affordable housing makes it more difficult for low-income workers to move to well-paying jobs. Access to health services and higher education are also uneven and limit access to economic opportunities for low income households. Many young Latvians emigrate. These issues and policies to address them are analysed in the