by Nicola Brandt, France Desk, Country Studies Branch, OECD Economics Department

While overall poverty is relatively low in France, it can be highly concentrated at the neighbourhood level. In some cases the income of up to 40% of households in such neighbourhoods falls short of the relative poverty line. Unemployment is high, many children struggle in school, housing and urban infrastructure is run down, and there is a lack of local employers, public and private services, and amenities. The French government targets education, employment, business and safety measures specifically at these areas. There are also dedicated policies to promote social mixing: municipalities in areas with tensions on the housing market have to reach a social housing share of at least 25% or face fines. A large-scale urban renovation programme aims to attract the middle class to poor neighbourhoods and re-locate some of their inhabitants in wealthier areas when dilapidated social housing estates are demolished and smaller units with a mix of tenures are built on their sites. Such policies are based on the idea that there can be neighbourhood effects, whereby a high concentration of poverty would reinforce and reproduce economic and social disadvantage. Indeed, in the United States children who moved away from neighbourhoods with a high concentration of poverty have been found to attain higher levels of education and earnings than their peers who stayed behind (Chetty et al., 2016; Chetty and Hendren, 2015).

While these results do not necessarily carry over to the French context, as poverty overall is much lower than in the United States and the social safety net is stronger, there is clear evidence that social disadvantage is reinforced for inhabitants of France’s poor neighbourhoods. Their unemployment risk can almost double compared to individuals with comparable characteristics who live in wealthier neighbourhoods (Figure 1). Studies show that this is partly due to discrimination – chances to be invited to an interview simply fall when a CV features a foreign-sounding name or an address in a poor area (Bunel et al., 2016; Petit et al., 2016). Another issue is that many poor neighbourhoods are remote and poorly connected to transport infrastructure and services. This is particularly true at unusual hours, which are more common among low-qualified workers. At the same time they are less likely to have a driver’s license or own a car. The recently released OECD Economic Survey of France concludes that active policies are needed to fight discrimination. This can include awareness campaigns for recruiters as well as mentoring and coaching for candidates to put them into direct contact with employers, which has proven to work well for university graduates.

The urban renovation programme has improved infrastructure, and many inhabitants are satisfied with the results, but the impact on social mixing is more questionable. Echoing the experience from other countries many inhabitants have been relocated to other high-poverty neighbourhoods. Moreover, mixing tenures is no guarantee for more social interaction (Posthumus et al., 2013; Lelévrier, 2013a and b). As the government plans to extend the programme the Economic Survey recommends to better integrate it with employment and social policies. Consultation with inhabitants about the planned projects should be used as an entry point to offer basic skills and language training. Renovation works themselves would be an opportunity to offer apprenticeship-style training for building sector jobs. Indeed, consultation needs to improve, and citizen councils introduced in 2014 to help to draft strategy documents for the economic and social development of poor neighbourhoods are a first step in that direction. Strong resident participation in designing and implementing renovation projects has been successfully practiced in Germany (Blanc, 2010), where self-directed rehabilitation is a common model, and more recently the United States (Kirszbaum, 2013), where residents of demolished sites now have a right to return.

France has run priority education programmes to devote more resources to schools with many disadvantaged pupils for more than 30 years, but the impact of socio-economic background on learning outcomes is still among the highest in the OECD (Figure 2). The OECD Economic Survey of France argues the introduction of various measures to enhance individualised support for struggling students has suffered from a lack of high-quality initial and continuing pedagogical training for teachers to ensure effective implementation. More has to be done to offer attractive pay and career prospects for teaching in schools with many disadvantaged children to attract and retain excellent teachers. While the premium for teaching in priority education schools has recently been lifted, it remains too low to stabilise teaching teams, and, until recently, some advantages for teachers in those schools actually helped them to leave faster, creating perverse incentives.

Presentation: What policies for poor neighbourhoods?

This discussion will be introduced by the author on Friday 13 October at 9h30 at the Université Paris-Est Marne-la-Vallée. A round table discussion will follow the presentation. The event is open to the public, for more information: http://www.tepp.eu/conferences/ contacts : samir.mellal@u-pem.fr

Bibliography

Blanc, M. (2013), “La gouvernance participative et la rénovation urbaine en Allemagne et en France”, 6èmes Rencontres du Réseau transfrontalier ’Participation Grand Est’, Strasbourg.

Bunel, M., Y. L’Horty and P. Petit (2016), “Discrimination based on place of residence and access to employment”, Urban Studies, Vol. 53, No. 2, pp. 267-86.

Chetty, R. and N. Hendren (2015), “The impacts of neighborhoods on intergenerational mobility: childhood exposure effects and county-level estimates”, https://scholar.harvard.edu/files/hendren/files/nbhds_paper.pdf.

Chetty, R., N. Hendren and L. Katz (2016), “The Effects of Exposure to Better Neighborhoods on Children: New Evidence from the Moving to Opportunity Experiment”, American Economic Review, Vol. 106, No. 4, pp. 855-902, April.

Kirszbaum, T. (2013), “Rénovation urbaine et équité sociale: Choice Neighborhoods aux Etats- Unis”, [Rapport de recherche] ISP; CNRS; Commissariat général à la stratégie et à la prospective; secretariat général du Comité interministériel des villes.

Lelévrier, C. (2013a), “La mixité dans la rénovation urbaine : dispersion ou re-concentration”, CAIRN Info, Paris.

Lelévrier, C. (2013b), “Social mix neighbourhood policies and social interaction: The experience of newcomers in three new renewal developments in France”, Cities, Vol. 35, pp. 409-16.

Petit, P., M. Bunel, E. Ene and Y. L’Horty (2016), “Effets de quartier, effet de département ; discrimination liée au lieu de résidence et accès à l’emploi”, Revue Économique, Vol. 67, pp. 525-50.

Posthumus, H., G. Bolt and R.Van Kempen (2013), “Why do displaced residents move to socioeconomically disadvantaged neighbourhoods?”, Housing Studies, Vol. 28, No. 2, pp. 272-93.

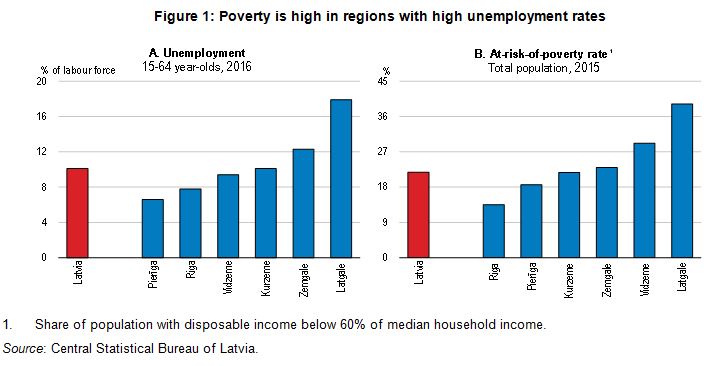

Housing policies shape residential mobility and can encourage workers’ movement to jobs (Andrews et al, 2011). The 2017 Economic Survey of Latvia therefore argues that good housing policies help reduce unemployment in high-unemployment areas. By helping workers find better jobs, they can also boost productivity and wages. Housing policies are particularly relevant for young people since they have a naturally higher propensity to move. Good housing policies could also encourage young people to seek opportunities in Latvia rather than emigrate.

Housing policies shape residential mobility and can encourage workers’ movement to jobs (Andrews et al, 2011). The 2017 Economic Survey of Latvia therefore argues that good housing policies help reduce unemployment in high-unemployment areas. By helping workers find better jobs, they can also boost productivity and wages. Housing policies are particularly relevant for young people since they have a naturally higher propensity to move. Good housing policies could also encourage young people to seek opportunities in Latvia rather than emigrate.

With a particular focus on the business environment and skills and labour market policies the 2017

With a particular focus on the business environment and skills and labour market policies the 2017

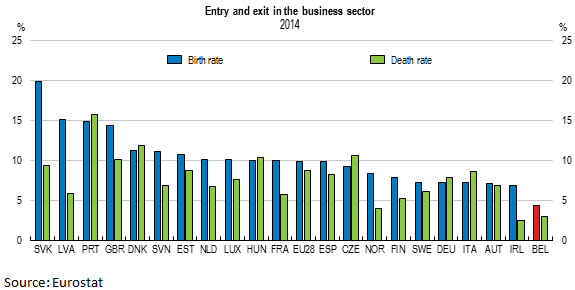

Productivity growth has also been held back by low public investment, particularly in transport infrastructure. Public investment declined from close to 6% of GDP in the early 1970s to just above 2% of GDP since the 1990s (Figure 4). Antwerp and Brussels are among Europe’s five most congested urban centres. Given limited fiscal space, public investment could be financed through a combination user fees, well-designed public-private partnerships, reductions in inefficient public spending, and higher non-distortionary taxes.

Productivity growth has also been held back by low public investment, particularly in transport infrastructure. Public investment declined from close to 6% of GDP in the early 1970s to just above 2% of GDP since the 1990s (Figure 4). Antwerp and Brussels are among Europe’s five most congested urban centres. Given limited fiscal space, public investment could be financed through a combination user fees, well-designed public-private partnerships, reductions in inefficient public spending, and higher non-distortionary taxes.