Child benefits and female labour supply – the case of Poland

by Nicola Brandt, Polish Desk, OECD Economics Department

In 2016 the Polish government introduced a large new child benefit, called “Family 500+”, with the aim to increase fertility from a low level and reduce child poverty. The benefit is universal for the second and every further child and means-tested for the first child. It more than doubles fiscal support for families, making Poland one of the top spenders in the EU concerning cash transfers for families.

It is already clear that the benefit helped to materially reduce child poverty. Extreme child poverty dropped by 3 percentage points in 2016 and the effect may well strengthen, as the benefit was paid out only starting in June of that year. It is too early to gauge the effect on births, which have been rising lately, but this could be mainly a result of the booming labour market and rising incomes. Studies for other countries find that generous family benefits can have a positive impact on fertility, although estimated effects differ widely (Brainerd, 2014).

But there may also be undesirable side effects on employment. Evidence from other countries suggests that that there can be negative effects of child benefits on female labour supply, which tend to be greater for women with lower skills (Schirle, 2015; Haan and Wrohlich, 2011). Access to affordable childcare is improving in Poland, but still very limited in many areas, in particular for the smallest children. It is hardly used at all by mothers with less than tertiary education (Figure 1). In that context child benefits can create disincentives to work for single mothers or second earners with children. This is due to its feature that the benefit is withdrawn at once when per capita family income increases beyond the eligibility ceiling. As an example, the OECD tax-benefit models suggest that an unemployed single mother of two taking up a job that pays the average wage would retain less than 20% of her earnings as a result of taxes and benefit withdrawal. If her only choice is unsubsidised private childcare, she would actually lose money.

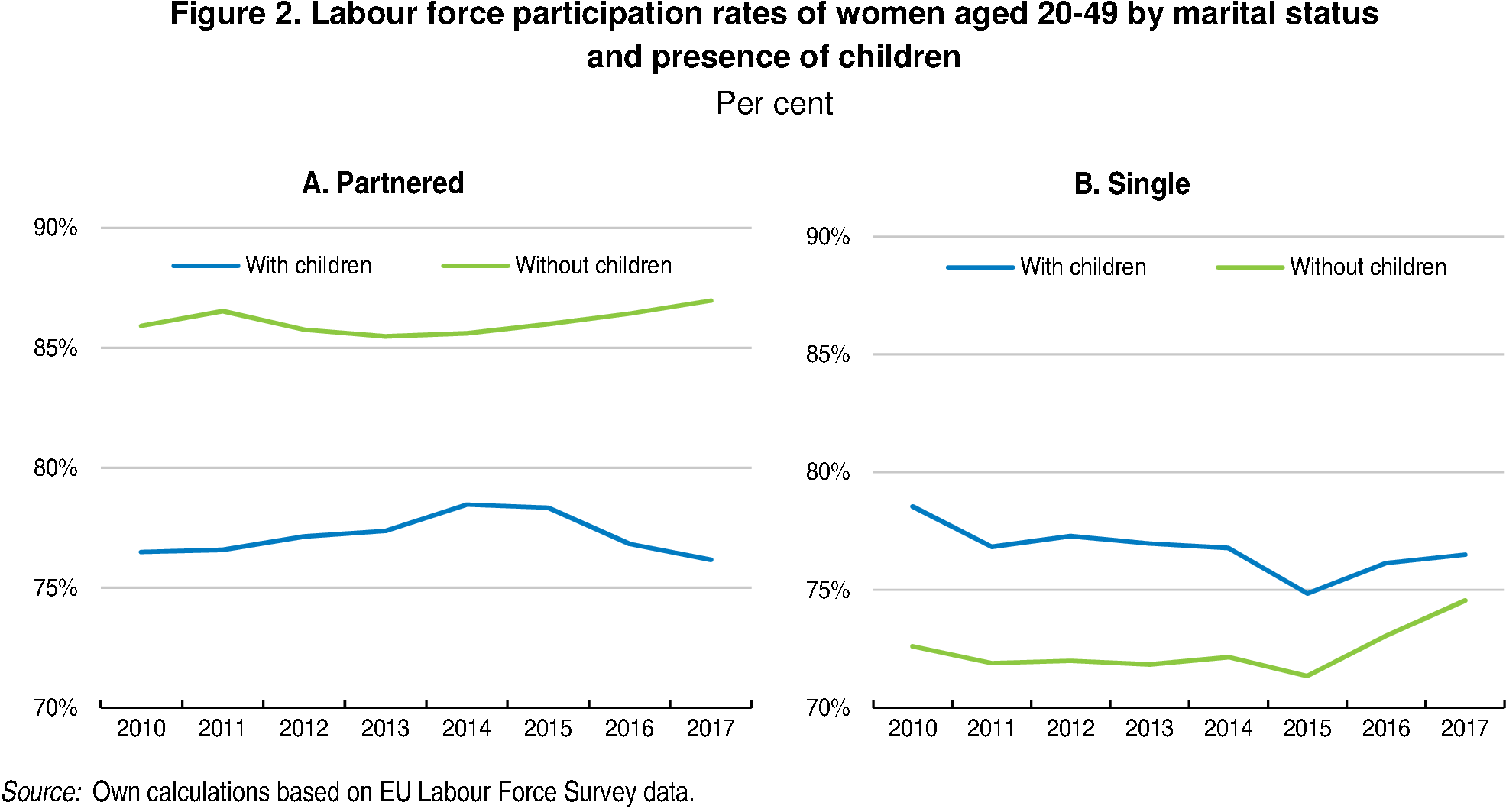

Joint research by the Institute for Structural Research (IBS) in Warsaw and the OECD finds that the introduction of the child benefit has indeed had a negative effect on labour force participation and employment of mothers. The study compares labour force participation trends for mothers of up to two children and childless women, differentiating between single and partnered women, as female labour supply is thought to be influenced by the presence of a partner. Figure 2 shows that while in each subgroup labour force participation trends were similar for mothers and childless women prior to the introduction of the child benefit, they started to diverge markedly after that. For partnered mothers, labour force participation actually fell.

A more formal econometric analysis comparing labour force participation trends across these groups based on a difference-in-differences approach suggests that for both single and partnered mothers labour force participation might have been almost 3 percentage points higher in the absence of the child benefits in the first half of 2017. The analysis also reveals that the effect is strongest for relatively low-qualified mothers with basic vocational education or less.

While this research does imply that large child benefits can affect female labour force participation negatively, there is reason to believe that context and design matter. For example, by withdrawing the benefit for the first child more gradually the government could mitigate negative effects on labour supply. Another solution would be to make the benefit income-dependent for all children, but with a much higher eligibility ceiling as higher-earning mothers’ labour supply seems to be less affected by the benefit. Stepping up efforts to quickly extend access to affordable childcare is also likely to reduce any undesirable side effects on female labour supply.

Further reading

OECD (2018), OECD Economic Surveys: Poland 2018, OECD Publishing, Paris. http://dx.doi.org/10.1787/eco_surveys-pol-2018-en

Magda, I., A. Kielczewska and N. Brandt (2018), The impact of large child benefits on female labour force supply – the case of Poland’s “Family 500+” programme.

Brainerd, E. (2014), “Can government policies reverse undesirable declines in fertility?”, IZA World of Labor ; vol. 23, doi: 10.15185/izawol.23.

Haan, P. and K. Wrohlich (2011), “Can child care policy encourage employment and fertility?: Evidence from a structural model. Labour Economics”, vol. 18, pp. 498-512.

Schirle, T. (2015), “The effect of universal child benefits on labour supply”, Canadian Journal of Economics/Revue canadienne d’économique, Vol. 48, No.2, pp. 437-63.