Álvaro S. Pereira, Economista Jefe interino, Departamento de Economía de la OCDE

Después de un largo período de débil crecimiento, la economía mundial finalmente está creciendo alrededor del 4%, cercano al promedio histórico de las últimas décadas.

Esta es una buena noticia, y es aún mejor sabiendo que, en parte, el mayor crecimiento de la economía mundial está respaldado por una recuperación positiva de la inversión y del comercio mundial. Cabe destacar especialmente la recuperación de la inversión, ya que el futuro de la actual expansión dependerá en gran medida del buen comportamiento de la inversión.

Aunque se esperaba desde hace mucho tiempo, el repunte de la inversión sigue siendo más débil que en expansiones anteriores. Lo mismo ocurre con el comercio mundial, que se espera crezca a un ritmo aceptable, aunque no espectacular, a menos que se vea frenado por las tensiones comerciales.

Sin embargo, a diferencia de períodos anteriores, el crecimiento mundial del 4% no se debe al aumento de la productividad ni a un cambio estructural radical. Esta vez, el fortalecimiento de la economía se debe en gran medida al apoyo de la política monetaria y fiscal.

Durante muchos años, la política monetaria fue la única carta sobre la mesa. Durante la crisis financiera internacional, los bancos centrales recortaron de manera drástica los tipos de interés, inyectaron fondos en la economía y compraron activos a un ritmo récord en un intento por impulsar la economía.

En cambio, en la mayoría de los países, la política fiscal siguió siendo prudente o incluso se contrajo. No obstante, los tipos de interés históricamente bajos brindaron a los gobiernos la oportunidad de utilizar el espacio fiscal disponible para ayudar a fomentar el crecimiento, como firmemente argumentó la OCDE en 2016. Muchos gobiernos de la OCDE siguen ahora esta recomendación. En un principio, los recursos habilitados por la reducción de los pagos de intereses fueron utilizados por los gobiernos para evitar recortar gastos o aumentar los impuestos. Con la mejora de la situación económica, muchos gobiernos han comenzado a emprender una relajación fiscal adicional.

Ahora que la política monetaria está finalmente empezando a volver a la normalidad, los gobiernos están interviniendo para proporcionar apoyo con la política fiscal. Podemos decir que la política fiscal es la nueva carta que se añade a la partida: tres cuartas partes de los países de la OCDE están llevando a cabo una relajación fiscal. El estímulo fiscal en algunos países es muy significativo, mientras que en otros es menos ambicioso. No obstante, esta relajación fiscal tendrá importantes repercusiones para la economía mundial. A corto plazo, contribuirá al crecimiento. Sin embargo, los países que han experimentado expansiones más prolongadas podrían encontrarse con que este estímulo fiscal (en los casos en que es importante) también se sumará a las presiones inflacionarias a medio plazo. Sólo el tiempo dirá si las ganancias de corto plazo podrían verse compensadas por impactos negativos de medio plazo. Lo que importa es que, al tomar estas decisiones, los gobiernos sean plenamente conscientes del impacto a medio plazo de sus políticas, y no se centren únicamente en los beneficios de corto plazo de los estímulos fiscales.

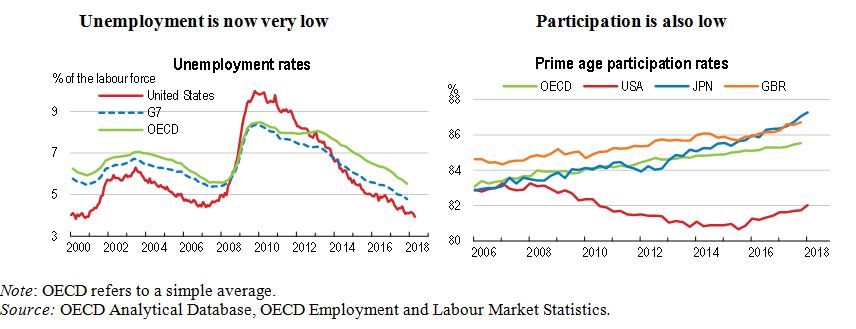

El fuerte crecimiento que estamos presenciando también está asociado a una fuerte creación de empleo en muchas economías. De hecho, es especialmente satisfactorio comprobar que en los países de la OCDE el desempleo va a alcanzar su nivel más bajo desde 1980, aunque en algunos países sigue siendo elevado. Gracias a esta sólida creación de empleo y a la consiguiente intensificación de la escasez de mano de obra, ahora se prevé un aumento de los salarios reales en muchos países, a pesar de que este aumento es todavía modesto. Sin embargo, hay señales claras de que los salarios están finalmente aumentando. Se trata de un acontecimiento importante, ya que la crisis mundial tuvo un grave impacto en los ingresos de los hogares, en particular de los trabajadores no cualificados y de bajos ingresos.

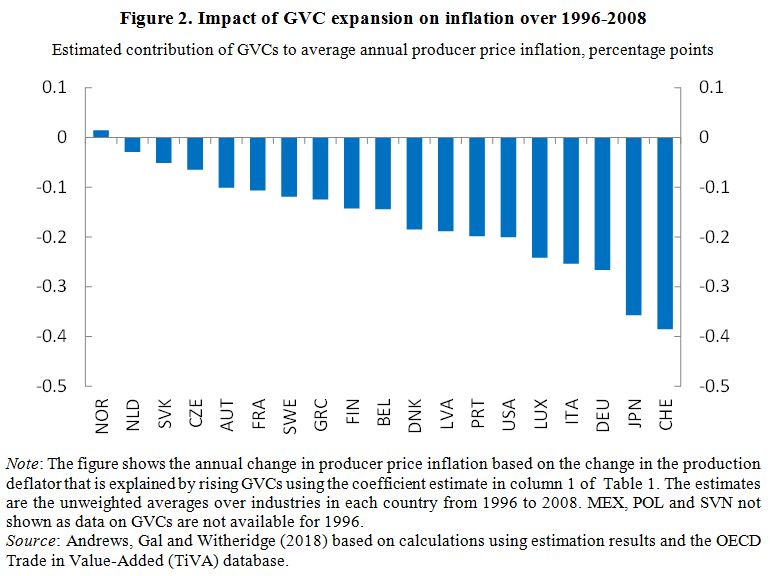

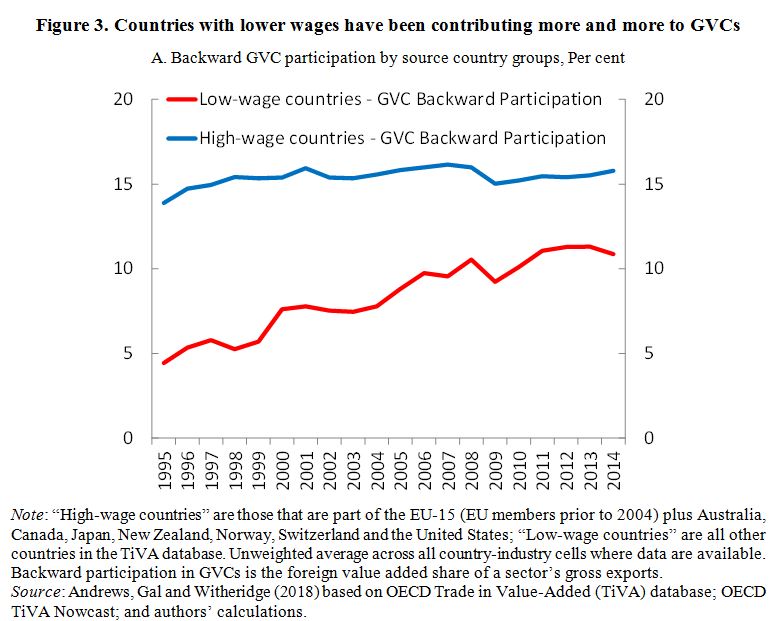

A pesar de todas estas buenas noticias, se advierten importantes riesgos en el panorama mundial. ¿Cuáles son estos riesgos? Ante todo, debe evitarse un aumento de las tensiones comerciales. Es importante recordar que, en parte, el aumento de las restricciones comerciales no es nada nuevo. Después de todo, los países del G20 han implementado más de 1.200 nuevas restricciones al comercio desde el inicio de la crisis financiera mundial en 2007. No obstante, como se señala en el Capítulo 2, dado que la economía mundial está mucho más integrada e interconectada hoy que en el pasado, una mayor escalada de las tensiones comerciales podría afectar significativamente la expansión económica y perturbar las vitales cadenas de valor mundiales.

Mirando hacia el futuro, otro riesgo importante está relacionado con el aumento de los precios del petróleo que han aumentado cerca del 50% en el último año. Esta persistente subida incrementará las presiones inflacionarias y agravará los desequilibrios externos en muchos países.

En los últimos años, los extremadamente bajos tipos de interés han alentado el endeudamiento de los hogares y las empresas en algunos países, y han dado lugar a la sobrevaloración de activos (por ejemplo, viviendas, acciones) en muchos otros. En este contexto, los crecientes los tipos de interés podrían ser un reto para los fuertemente endeudados países, familias y empresas. Además, esta subida de los tipos de interés se ha anticipado ampliamente y, por lo tanto, no debería causar ninguna perturbación importante. Sin embargo, si la inflación aumenta más de lo previsto y los bancos centrales se ven obligados a subir los tipos de interés a un ritmo más rápido, es probable que la confianza del mercado cambie bruscamente, dando lugar a una repentina corrección de los precios de los activos.

Una subida más rápida de los tipos de interés en las economías avanzadas también podría seguir provocando una depreciación significativa de la moneda y volatilidad en algunas economías emergentes (EMEs) ya que dependen en gran medida de la financiación externa y se enfrentan a desequilibrios internos o externos. Las tensiones geopolíticas también podrían contribuir a correcciones repentinas del mercado o a una nueva subida de los precios del petróleo. Brexit y la incertidumbre política en Italia podrían añadir presiones a la expansión en la zona del euro.

¿Qué significa todo esto para la política? Dado que la deuda pública y privada sigue siendo elevada en algunos países, la mejora de la productividad, la disminución de los niveles de deuda y la creación de amortiguadores fiscales son clave para fortalecer la resiliencia de las economías. Puesto que las políticas monetaria y fiscal no podrán sostener la expansión de manera permanente e incluso podrían acentuar los riesgos financieros, es absolutamente esencial que las reformas estructurales se conviertan en una prioridad. En los últimos dos años, pocos países han emprendido reformas estructurales sustanciales. La mayoría de los países que aplicaron reformas son grandes EMEs, como Argentina, Brasil e India. En las economías avanzadas, se introdujeron importantes reformas laborales en Francia, y se aplicó una amplia reforma fiscal en los Estados Unidos. Sin embargo, como señala la publicación de la OCDE Going for Growth, de 2018, éstas importantes excepciones no contradicen la regla de que los esfuerzos de reforma han sido rezagados.

¿Por qué es esto importante? Porque la única manera de mantener la expansión actual y hacer que el crecimiento funcione para todos es emprender reformas que aumenten la productividad. Como demuestran numerosos estudios de la OCDE sobre la revisión de políticas educativas (Education Policy Reviews) y las estrategias nacionales de la OCDE en materia de competencias (National Skills Strategies), es fundamental rediseñar los planes de estudio para desarrollar las competencias cognitivas, sociales y emocionales que permiten el éxito en el trabajo, y mejorar la calidad de la enseñanza y los recursos necesarios para impartir esas competencias de manera eficaz. En muchos países, la inversión en educación de calidad para la primera infancia, la formación profesional y los programas de aprendices revisten especial importancia. También son cruciales las reformas del mercado laboral que mejoren las habilidades. Las reformas para impulsar la competencia, mejorar los regímenes de insolvencia, reducir los obstáculos a la entrada en el sector de los servicios y reducir la burocracia también son fundamentales para hacer que nuestras economías sean más dinámicas, más incluyentes y más emprendedoras. La inversión en infraestructura digital también será esencial en esta era digital. Además, existen importantes oportunidades para reducir los costes del comercio de bienes y, en particular, de los servicios, impulsando el crecimiento y el empleo en todo el mundo.

A pesar de un crecimiento más fuerte, no hay tiempo para la autocomplacencia. Las reformas estructurales son vitales para mantener la expansión actual y mitigar los riesgos. Por lo tanto, en esta coyuntura de la economía mundial, es realmente crucial dar una oportunidad a las reformas. Después de que las políticas monetarias y fiscales hayan cumplido sus objetivos, es hora de que las reformas sostengan la expansión, mejoren el bienestar y hagan que el crecimiento funcione para todos.

Referencias

Perspectivas económicas OCDE, mayo 2018.

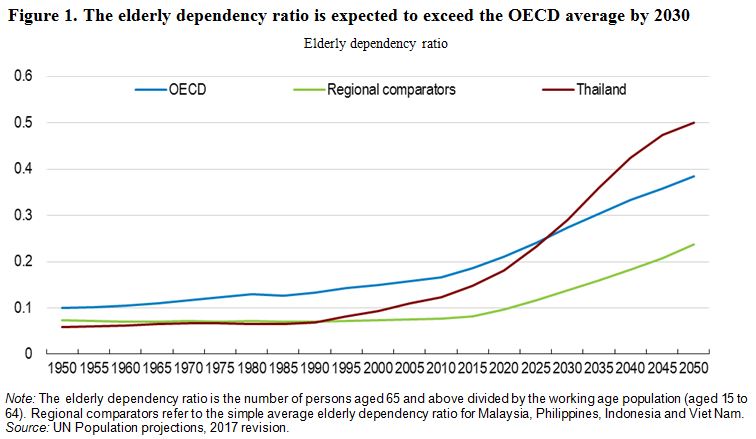

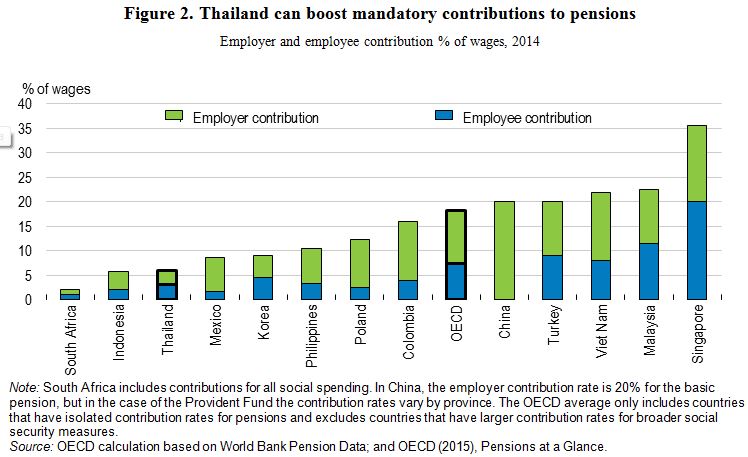

With a rapidly ageing population, the public burden to provide social pensions (which will need to increase to improve very low replacement ratios and safeguard against elderly poverty) and healthcare will grow considerably. Indeed, the Initial Assessment Report of the Multi-dimensional Review of Thailand notes that although Thailand’s current fiscal position is healthy, structural reforms to the pension and healthcare systems are needed to ensure fiscal sustainability (OECD, 2018).

With a rapidly ageing population, the public burden to provide social pensions (which will need to increase to improve very low replacement ratios and safeguard against elderly poverty) and healthcare will grow considerably. Indeed, the Initial Assessment Report of the Multi-dimensional Review of Thailand notes that although Thailand’s current fiscal position is healthy, structural reforms to the pension and healthcare systems are needed to ensure fiscal sustainability (OECD, 2018). In healthcare, Thailand should avoid near-term regressive and often ineffective blanket cuts to the health budget and instead implement targeted structural reforms that will be beneficial over the longer run. For example, to prevent overburdening of hospitals, Thailand should increase health provision through preventive and primary care by boosting the number of family physicians and general practitioners, particularly in rural areas. Healthcare financing should also be reformed by reducing the exemptions on co-payments and allowing greater private contributions from those able to afford it.

In healthcare, Thailand should avoid near-term regressive and often ineffective blanket cuts to the health budget and instead implement targeted structural reforms that will be beneficial over the longer run. For example, to prevent overburdening of hospitals, Thailand should increase health provision through preventive and primary care by boosting the number of family physicians and general practitioners, particularly in rural areas. Healthcare financing should also be reformed by reducing the exemptions on co-payments and allowing greater private contributions from those able to afford it.