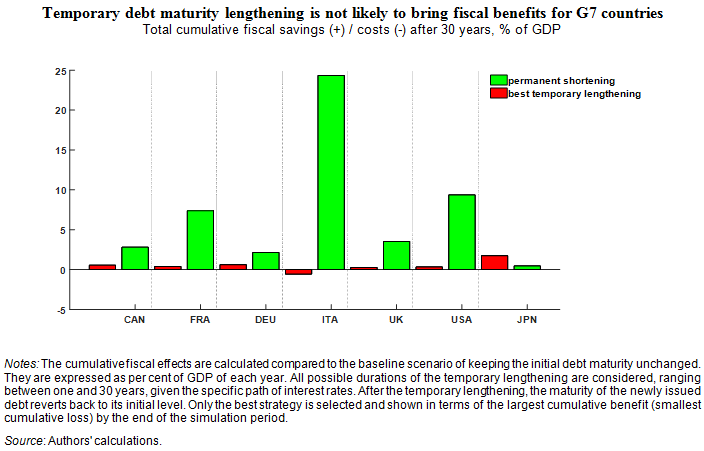

by Makoto Kasai and Łukasz Rawdanowicz, OECD Economics Department[1]

As discussed in the latest OECD Economic Outlook, the prolonged undershooting of inflation targets, despite massive monetary policy stimulus and stronger economic growth and lower unemployment, raises issues about the appropriateness of current inflation targeting frameworks in advanced economies. While the frameworks differ in detail and implementation, they are principally based on medium-term inflation objectives of 2%.

Various modifications of, and alternatives to, inflation targeting frameworks have been advocated to make monetary policy more effective and credible. While none of them is without drawbacks, and it is not clear if they would provide substantial improvements from those used at present, periodic reviews of current frameworks would be useful.

Raising the inflation target

Based on theoretical models with forward-looking expectations, raising the inflation target has been suggested as a way to boost inflation expectations and in turn inflation outcomes (Blanchard et al., 2010; Ball, 2014; Baker et al., 2017).

Higher inflation targets, if effective in raising actual inflation, are estimated to lower the probability of hitting an effective zero lower bound (ZLB) and thus reduce the potentially large economic costs of stagnations (Kiley and Roberts, 2017; Dorich et al., 2018; Ball, 2014). Although, in principle, the economic costs caused by the ZLB could be mitigated by adopting unconventional measures, the overall effectiveness of these measures remains debatable.

However, higher target and actual inflation could also entail economic costs, though estimating the level of inflation where costs start to dominate is difficult. Moreover, if a central bank changes its inflation target once, further revisions may be expected, leading to de-anchoring of inflation expectations and undermining the effectiveness of the inflation targeting framework.

While low inflation targets helped to reduce inflation in the 1990s (and its subsequent stabilisation), it is uncertain if the opposite would work. Indeed, Japan’s experience with increasing the inflation target from 1% to 2% in 2013 followed by massive quantitative and qualitative monetary policy easing, after the prolonged period of subdued inflation, demonstrates the practical challenges. Even if realised and expected inflation have indeed increased, they have remained below the target.

Price level targeting

Under price level targeting, a period of lower inflation should be followed by a period of higher inflation so as to neutralise the impact on the price level. In the current context, it is equivalent to committing temporally to a higher inflation target, but with the benefit of avoiding the cost of permanently higher inflation. As with raising inflation targets, the benefits of this framework depend on the ability of central banks to affect inflation expectations and outcomes. If this is the case, the framework will help to raise inflation expectations and avoid the ZLB in the future. If this is not the case, or if the economy experiences persistent positive supply-side shocks, it could result in prolonged periods of very easy monetary policy with risks to future financial stability.

Symmetric operation of inflation targeting

Central banks’ commitment to symmetric operation of monetary policy around their inflation targets is in a sense a milder variant of price level targeting. While the major central banks have symmetric price stability objectives in the medium term, some of them are perceived to have a bias in operating their monetary policy to maintain inflation close to but below their targets (Evans, 2017). This bias might have weakened their ability to raise inflation expectations and to achieve the target. This concern arguably prompted the US Federal Reserve and the ECB to emphasise the symmetric inflation goal in their communication (Draghi, 2016).

Nominal GDP level targeting

Nominal GDP level targeting, if effective, shares the advantages of price level targeting while it can avoid central banks’ overreacting to supply shocks (Bean, 2013). In spirit, it is similar to the dual mandate of the US Federal Reserve. It is expected to work well in the situation where maintaining short-term price stability is not enough to achieve stable growth of the economy in the medium to long run. Nominal GDP level targeting, however, shares drawbacks with the above propositions, and adds complications as nominal GDP is even more difficult to control than inflation. Moreover, GDP data tend to be revised substantially and are not available at a high frequency.

Inflation target range

An inflation target range with the upper band above 2% would have some similarity to the arrangements discussed above in the current context. This is especially the case with respect to the symmetric operation of inflation targeting, by signalling that higher inflation could be tolerated.

However, a framework with a target range allows the authorities to operate monetary policy more flexibly, reflecting the fact that monetary authorities have only a limited ability to predict inflation and control inflation expectations and outcomes (Andersson and Jonung, 2017). This flexibility is useful when the persistence and size of idiosyncratic shocks are uncertain or when changes in the monetary policy stance could aggravate financial stability risks. As long as inflation is expected to stay within the range, monetary authorities would not need to change their stance, while – as with point inflation targeting – they would be expected to act when inflation risks deviating from the range.

With a relatively narrow and low range, this framework could still be consistent with the price stability objective and would not involve negative welfare effects, justifying a less active monetary policy stance. Consequently, it might help to lower the risk of hitting the ZLB, as central banks over time could keep their powder dry. This framework could also improve central banks’ credibility, as there will be a higher probability of inflation staying within a range rather than at a point target. With the current frameworks, even small deviations of inflation from the target point tend to be interpreted as a failure of monetary policy and raise expectations of monetary authorities’ reacting.

On the other hand, the inflation targeting framework based on a range could potentially lower central banks’ influence on inflation expectations as it could be perceived as weakened commitment to price stability. The target range could make it difficult to understand the reaction function of central banks. Indeed, a point inflation target may be easier to communicate and may be more effective in influencing inflation expectations of households and businesses.

References

Andersson, F. N. G. and L. Jonung (2017), “How Tolerant Should Inflation-Targeting Central Banks Be? Selecting the Proper Tolerance Band – Lessons from Sweden”, Lund University Department of Economics Working Paper, No. 2017: 2.

Baker, D. et al. (2017), “Prominent Economists Question Fed Inflation Target”, letter to the Federal Reserve Board of Governors, The Center for Popular Democracy, June 2017. http://populardemocracy.org/sites/default/files/Rethink%202%25%20letter.pdf

Ball, L. (2014), “The Case for a Long-Run Inflation Target of Four Percent”, IMF Working Papers, No 14/92.

Bean, C. (2013), “Nominal Income Targets – An Old Wine in a New Bottle”, speech at the Institute for Economic Affairs Conference on the State of the Economy, London, February.

Blanchard, O., G. Dell’Ariccia and P. Mauro (2010), “Rethinking Macroeconomic Policy”, Journal of Money, Credit and Banking, 42(1), 199-215.

Dorich, J., N. Labelle, V. Lepetyuk and R. R. Mendes (2018), “Could a Higher Inflation Target Enhance Macroeconomic Stability?”, Bank of Canada Staff Working Paper, 2018-17.

Draghi, M. (2016), “Delivering a Symmetric Mandate with Asymmetric Tools: Monetary Policy in a Context of Low Interest Rates”, speech at the ceremony to mark the 200th anniversary of the Oesterreichische Nationalbank, Vienna, June.

Evans, C. L. (2017), “Low Inflation and the Symmetry of the 2 Percent Target”, Speech at UBS European Conference, London, November.

Kiley, M. T. and J. Roberts (2017), “Monetary Policy in a low interest rate world”, Brookings Papers on Economic Activity, March 2017.

OECD (2018), OECD Economic Outlook, Volume 2018 Issue 1: Preliminary version, OECD Publishing, Paris.

[1]. The opinions expressed and arguments employed are those of the authors and not necessarily of their respective institutions. Makoto Kasai currently works for the Bank of Japan.

by Hansjörg Blöchliger and Vassiliki Koutsogeorgopoulou, Lithuania Desk, OECD Economics Department

by Hansjörg Blöchliger and Vassiliki Koutsogeorgopoulou, Lithuania Desk, OECD Economics Department

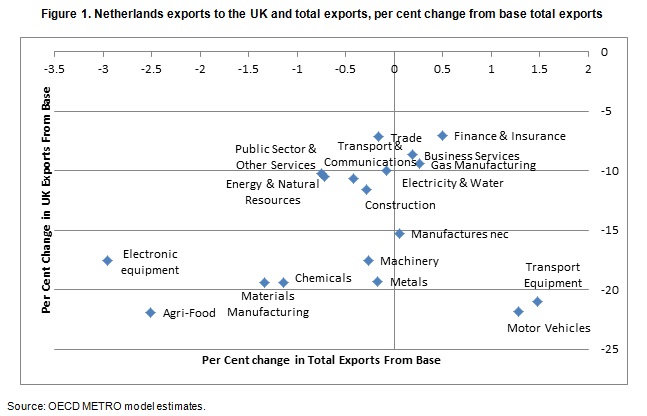

The Netherlands is likely to be one of the European countries that is going to be significantly affected by the United Kingdom’s planned departure from the European Union (Brexit). As an open economy with strong trade and investment links to the United Kingdom, the Netherlands is exposed to increases in barriers to trade between the United Kingdom and EU (Vandenbussche et al., 2017). New OECD simulations show the potential extent of this impact, as well as the different sectors of the Dutch economy likely to be affected.

The Netherlands is likely to be one of the European countries that is going to be significantly affected by the United Kingdom’s planned departure from the European Union (Brexit). As an open economy with strong trade and investment links to the United Kingdom, the Netherlands is exposed to increases in barriers to trade between the United Kingdom and EU (Vandenbussche et al., 2017). New OECD simulations show the potential extent of this impact, as well as the different sectors of the Dutch economy likely to be affected.

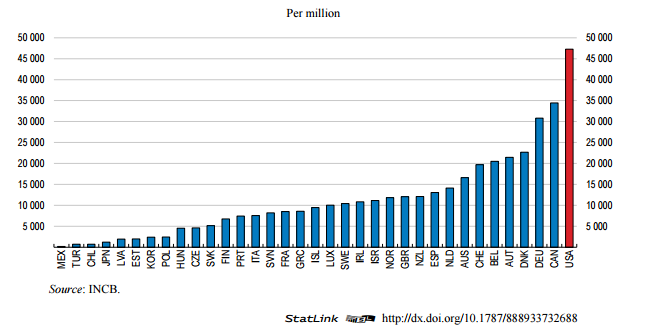

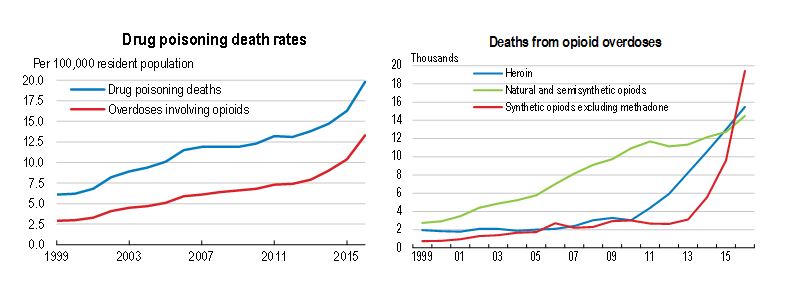

Opioids are far more commonly prescribed in the United States than elsewhere in the OECD. Between 1999 and 2014, opioid prescriptions in the United States quadrupled. This was compounded by relatively liberal policies on the number of opioids being prescribed, the long duration of treatment and aggressive marketing. Ultimately millions of individuals were exposed to addictive substances, either the intended patient or through unused drugs being taken by family members or others.

Opioids are far more commonly prescribed in the United States than elsewhere in the OECD. Between 1999 and 2014, opioid prescriptions in the United States quadrupled. This was compounded by relatively liberal policies on the number of opioids being prescribed, the long duration of treatment and aggressive marketing. Ultimately millions of individuals were exposed to addictive substances, either the intended patient or through unused drugs being taken by family members or others.