Ensuring high but sustainable growth in Türkiye

By Sébastien Turban, Economist, OECD

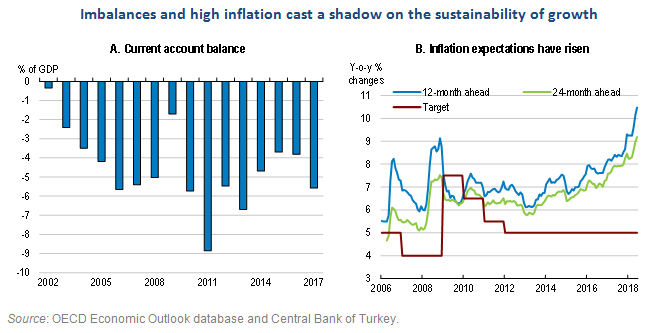

Türkiye has been one of the fastest-growing economies in the OECD over the past decade, leading to a significant improvement of labour market and social outcomes. However, the income gap with OECD countries remains large. In addition, growth had become unsustainable in the years following the Covid crisis since it relied excessively on domestic demand, which lead to large internal and external imbalances in 2022, notably very high inflation and a sizeable current account deficit.

In this context, the new 2025 OECD Economic Survey of Türkiye (OECD, 2025a) contains four main messages:

- Prudent macroeconomic policies are a pre-requisite for sustainable growth.

- Higher productivity gains are needed to speed up convergence towards other OECD economies.

- The economy would hugely benefit from a higher labour force participation of women.

- A greener economy requires more ambitious policies, notably transitioning away from coal.

Following the May 2023 elections, a more prudent macro-economic policy mix has been implemented. The Central Bank has gradually raised interest rates, and the government is planning a fiscal consolidation for the coming years. This policy has started to bear fruits, with a reduction of imbalances, including a gradual fall in inflation (Figure 1). Maintaining tight monetary policy and fiscal discipline will be essential until inflation is firmly under control. Over the long term, improving public finances will require structural reforms. This includes reducing the scope of reduced VAT rates, a broader income tax base (in particular by tackling informality), and targeting better social assistance to help reduce the high level of inequalities.

Productivity has increased faster in Türkiye than other OECD countries in the last decades, but potential GDP per worker remains relatively low. Higher productivity gains, in particular in services sectors, require supporting innovation, upskilling the labour force, and reducing barriers to the conduct of business activity. The Economic Survey discusses three important steps in this respect.

- Firstly, Türkiye could boost homegrown innovation by supporting collaborations between businesses and research to promote broader technology adoption.

- Secondly, the skills of the labour force could be improved to adapt to future challenges. Important skills mismatches remain and incentives for tertiary education institutions to offer courses more aligned with labour market needs could be further enhanced.

- Finally, business dynamism in Türkiye remains hampered by tighter regulations relative to other OECD countries (Figure 2). In particular, barriers in professional services could be lowered.

Boosting the participation of women in the labour force would hugely benefit the economy. This would increase the pool of talents the economy needs, especially as population is ageing, with a contribution to growth of working-age population set to decline. The labour force participation of women aged between 15 and 64 years old, at 40.9% in 2023, remains significantly below the OECD average of 66.7% (Figure 3). A combination of policies would help closing the gap between women and men on labour markets, such as expanding public investment in early childhood education and care (ECEC), introducing shareable paid parental leave, and increasing child-related benefits.

Finally, achieving the ambitious target of zero net emissions of carbon by 2053 will require more ambitious policies since greenhouse gas emissions are still growing. Türkiye has made recent progress in its climate change strategy by ratifying the Paris Agreement in 2021, updating its Nationally Determined Contribution in 2023 and documenting strategies and action plans thoroughly. However, current policies are likely to be insufficient to achieve the ambitious objectives. In particular, two important steps can be taken to bring the reduction in emissions forward. First, the effective carbon tax should be higher. Today, the effective price of carbon in Türkiye is EUR 8 per ton of CO2 equivalent, against EUR 62 in the OECD (OECD, 2023). Second, Türkiye will need to transition away from coal for energy supply as this polluting energy source still represents 26% of energy supply (against 12% in the OECD) and contributes to emissions of fine particulates with significant adverse health effects (OECD, 2025b).

References

OECD (2025a), OECD Economic Surveys: Türkiye 2025, OECD Publishing, Paris,

https://doi.org/10.1787/d01c660f-en.

OECD (2025b), Environment at a Glance Indicators, OECD Publishing, Paris,

https://doi.org/10.1787/ac4b8b89-en.

OECD (2023), Effective Carbon Rates 2023: Pricing Greenhouse Gas Emissions through Taxes and Emissions Trading, OECD Series on Carbon Pricing and Energy Taxation, OECD Publishing, Paris, https://doi.org/10.1787/b84d5b36-en.