Italy’s justice system has quite a long road ahead but already scores better – The Italian View

by the Italian Ministry of Economy and Finance – Pier Carlo Padoan, Italy’s Minister of Finance, was OECD Deputy Secretary-General and Chief Economist from 2009-2014).

Italy’s justice system is gaining greater efficiency, thus gradually closing its paradoxical gap. On the one hand, the clearance rate (measured as the ratio of the number of resolved cases to the number of incoming cases) is 120% and Italy ranks second in the European Union after Slovakia. On the other hand, Italy ranks last for the average length of civil or commercial proceedings, because of the huge backlog that weighs on courts and slows down the wheels of justice. Disposition time decreased by 13% in two years, but it still is as high as 527 days compared with a European average of 248 days. In 60% of Italian courts 1 out of 5 cases has been pending for more than 3 years, thus exceeding the “reasonable time” envisaged in the Pinto law of 2001. As priority will be given to recent cases, disposition time in courts that have a bigger backlog will lengthen. The longer a legal case remains unsettled, the longer the court will take to reach final disposition. The total backlog of civil cases has decreased by 4% from 2015 to 2016 and by a significant 34% from 2009. Nonetheless, the total civil and commercial litigious cases backlog was still as high as 4,400 cases pending (1st instance/ per 100,000 inhabitants) in 2005, 2.6 times higher than the EU average. Court performance varies geographically. Sicilian courts have a backlog of cases 50% of which have been pending for more than three years and less than 10 or 15% of which have been pending for more than three years.

With €4.8 bn of public expenditure, Italy is still the third biggest spender in the EU after Germany (€9.6 bn ) and the UK (€6.6 bn). Despite the crisis, total expenditure increased by 4.2% a year from 2006 to 2016. Better performances are not just a matter of increasing staff levels. Evidence published by the CSM (Consiglio Superiore della Magistratura – the High Council of the Judiciary) shows no correlation between staff shortages and poor performance, at least in conditions of relative and temporary lack of resources. With 1,75 million new legal cases per year, litigation rates in Italy are now in line with the EU average.

Efficiency gains have been achieved thanks to the far-reaching reorganization of the Italian judicial system and the adoption of new best practices in case management. First, e-filing has continued since its introduction in 2014. E-filing of notices increased by 6.7% over 2016, increasing savings by 10% and speeding up the issuing of digital payment orders by over 50% in some districts. E- filing by lawyers and professionals increased by 12% last year (after a first +88% in 2014/15), increasing the average e-files stock by 50% over the last three years.

Alternative dispute resolutions (ADR) contributes to unburdening courts in terms of dispute settlements. ADR includes referral to arbitration, negotiation assisted by a legal counsel (outof- court settlement procedure) and civil mediation. On average around 186,000 civil mediation processes have been initiated each year since 2014. The last two years have seen an increase in filings, followed by more than 30% increase in the number of judgments pending. This has slowed down resolution time from 83 days in 2013 to 115 days in 2015, which remains considerably shorter than that of in-courts settlements; however, a further increase, would affect the effectiveness of the process. The most evident reduction has been observed in commercial litigation, whose disposition time decreased from 40 to 29 months. Figures show that the older and more complex cases are now being settled, thereby contributing to rendering the justice system fairer. Specialization also helps in better managing the workflow. Since their introduction in 22 provinces in 2012, business courts have performed well. They deal exclusively with cases involving industrial property, company law, public contracts and services and European Union public work contracts. The number of resolved cases increased from an initial 404 to over 5,600 at the end of 2016. The increase in registrations raised resolution time: in 2016 the percentage of disputes which took less than a year to be resolved fell to 57% from 74% in 2014. Predictable outcomes and the number of confirmed rulings remain high, which reflect the quality of pronouncements and the effectiveness of judges and prosecutors’ specialization. In Milan verdicts are confirmed in 70-80% of cases.

Alternative dispute resolution is accompanied by measures to discourage initiation of proceedings when unneeded (i.e. no more free appeal proceedings before Justices of the Peace after administrative sanctions have been imposed) and the introduction of a formula to determine attorney fees (together with the possibility of requesting quotes). These rules contributed to decrease the demand for judicial services (civil and commercial cases), from 4 to 2.5 (1st instance/ per 100 inhabitants) between 2010 and 2015. However, the drop may also be ascribed to the economic crisis (a low GDP means fewer filings).

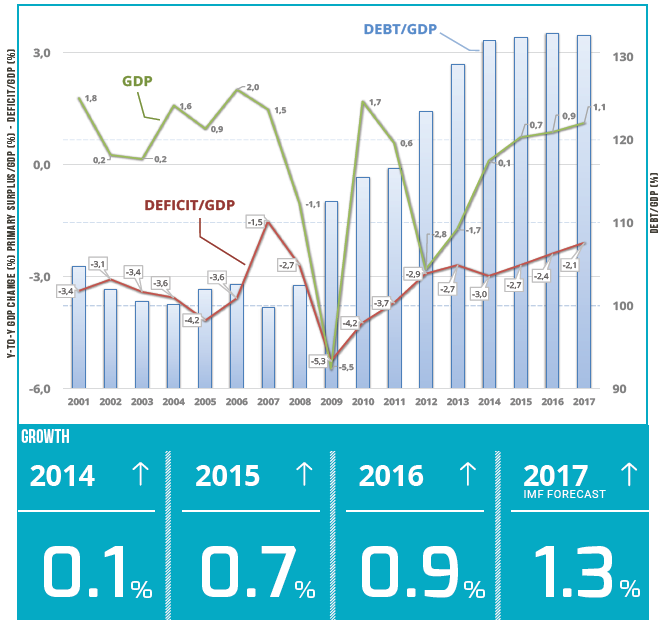

There is a positive correlation between economic growth and a healthy, efficient, fair judicial system. This is an even more important aspect especially during an upswing such as the one Italy is now experiencing. Lengthy proceedings and high enforcement create a climate of uncertainty and skepticism which affects the business environment and keeps investors away from opportunities. Given the same infrastructure and initial business conditions, evidence has shown that differences in the efficiency of judicial systems at provincial level can determine a difference in turnover of €31 K – or 8% of turnover – for an average Italian medium-sized company. A few years ago ECB President Mario Draghi stated that the cost of Italy’s slow judicial system accounts for over 1% of GDP. Gains in efficiency remain a top priority for the Government, which keeps working on reforms to speed up digitalisation and increase the overall effectiveness of the justice system.

It is common knowledge that – among other things – low productivity is one of the main causes of the poor performance of the Italian economy. Red tape, the relatively limited openness to competitiveness of some professional services, the tax burden, the limited size of SMEs, and the need to improve secondary education and the efficiency of the judicial system are – among other factors – affecting our ability to grow the economy.

It is common knowledge that – among other things – low productivity is one of the main causes of the poor performance of the Italian economy. Red tape, the relatively limited openness to competitiveness of some professional services, the tax burden, the limited size of SMEs, and the need to improve secondary education and the efficiency of the judicial system are – among other factors – affecting our ability to grow the economy.