By Laurence Boone, Mauro Pisu and Tim Bulman, OECD Economics Department

Also available in English

1. L’Italia ha attuato le raccomandazioni dell’OCSE per anni, ma l’economia rimane debole. L’Italia, non dovrebbe cambiare approccio?

L’Italia ha implementato alcune delle

raccomandazioni dei passati Raporti dell’OCSE sull’Italia e queste hanno prodotto

risultati. Per esempio:

- Precedenti Rapporti hanno raccomandato di ridurre i contributi previdenziali per aumentare l’occupazione. Tale riduzione è stata attuata su base temporanea dal 2015 e l’occupazione è aumentata di circa 3 punti percentuali. La crescita dell’occupazione ha iniziato a rallentare quando le riduzioni dei contributi previdenziali sono stati gradualmente eliminati.

- Precedenti Rapporti hanno raccomandato di rafforzare le politiche di innovazione e gli incentivi per gli investimenti innovativi. Il programma Industria 4.0 has introdotto incentivi fiscali per gli investimenti in tecnologie digitali, che da allora sono aumentati rapidamente.

- Precedenti Rapporti hanno raccomandato di migliorare gli appalti pubblici e combattere vigorosamente la corruzione. Le procedure di aggiudicazione degli appalti pubblici sono state ristrutturate e armonizzate in tutto il paese riducendo il numero delle stazioni appaltanti, con conseguenti notevoli risparmi; l’autorità anticorruzione (ANAC) ha assunto un ruolo di primo piano nella prevenzione della corruzione ed è ora un modello per altri paesi.

Ci sono molte aree in cui in Italia non ha seguito le raccomandazioni dell’OCSE. Ad esempio, i Rapporti precedenti hanno raccomandato di:

- Accelerare e snellire le procedure

fallimentari e facilitare la ristrutturazione delle imprese insolventi. Il

nuovo codice di insolvenza deve ancora essere approvato dal parlamento.

- Aumentare la spesa in R&S. La spesa

per R&S è ancora tra le più basse nei paesi OCSE (anche dopo aver tenuto

conto degli effetti del piano Industria 4.0).

- Aumentare i posti disponibili nelle

strutture per l’infanzia. L’Italia ha un numero esiguo di posti in asili nido e

questo è uno dei motivi per cui così poche donne lavorano in molte regioni.

- Aumentare gli investimenti pubblici,

che hanno continuato a diminuire.

- Aumentare la spesa per i centri per

l’impiego e ristrutturarli. Questo processo è appena cominciato.

- Rafforzare il sistema di apprendistato

introducendo standard minimi di qualità della formazione. Gli apprendistati

sono molto diffusi in Italia ma il loro contenuto educativo rimane limitato.

2. Qual è l’opinione dell’OCSE sul Reddito di Cittadinanza?

Il Rapporto sull’Italia accoglie con favore il forte aumento delle risorse per ridurre la povertà attraverso il Reddito di Cittadinanza. La misura è coerente con le precedenti raccomandazioni dell’OCSE e aiuterà a dirigere una quota maggiore di trasferimenti sociali verso le persone in condizioni di povertà.

Tuttavia, il Reddito di Cittadinanza potrebbe essere migliorato e contribuire maggiormente all’aumento dell’occupazione. Il suo livello attuale è elevato se comparato a simili programmi in altri paesi ed è superiore ai salari di molti posti di lavoro, specialmente nelle regioni più povere. Ciò scoraggerà i beneficiari dal lavorare nel settore formale dell’economia.*

Per affrontare questo problema, il Rapporto suggerisce di ridurre l’ammontare del Reddito di Cittadinanza del 30-40%, di ridurre gradualmente l’ammontare del trasferimento quando i beneficiari iniziano a lavorare e il loro reddito da lavoro cresce, d’introdurre un sistema di sussidi per i lavoratori a basso reddito in modo dal incrementare il loro salario netto.

Complessivamente, i cambiamenti proposti dall’OCSE per il Reddito di Cittadinanza, insieme ad altre modifiche riguardanti l’imposta sul reddito delle persone fisiche e le prestazioni sociali, costeranno circa 2,7 miliardi di euro in più rispetto a quanto già previsto dal governo per il Reddito di Cittadinanza. L’OCSE sta quindi raccomandando al governo italiano di spendere di più in misure per ridurre la povertà e aumentare l’occupazione rispetto a ciò che il governo ha pianificato di fare.

Il Rapporto accoglie inoltre con favore l’aumento della spesa per i centri per l’impiego prevista per il 2019-20. I centri per l’impiego sono di vitale importanza per garantire che coloro che ricevono il Reddito di Cittadinanza si impegnino in programmi di ricerca di lavoro e di formazione. Tuttavia, l’OCSE avverte, basandosi sull’ esperienze in altri, che il miglioramento dei centri per l’impiego richiede tempo. L’OCSE raccomanda di sviluppare un piano pluriennale di attuazione basato sul rafforzamento delle competenze del personale dei centri per l’impiego e ulteriori investimenti in IT e strumenti di profilazione.

3. Cosa c’è di sbagliato nell’incoraggiare il prepensionamento per liberare posti di lavoro per i giovani?

Il nuovo regime di prepensionamento

temporaneo (“quota 100”) introdotto con la legge di bilancio 2019

incoraggerà molti lavoratori a prendere la pensione anticipata, ma il suo costo

è elevato rispetto ai suoi benefici. Il nuovo regime aumenterà la spesa

pensionistica di 20 miliardi di EUR nel 2021 e di 40 miliardi di EUR entro il

2025. La spesa pensionistica italiana in percentuale del PIL è già una delle

più alta tra i paesi dell’OCSE. Questo ostacola la capacità dell’Italia di

espandere gli investimenti pubblici, compresa l’educazione.

Non vi è alcuna prova che gli schemi di prepensionamento liberino posti di lavoro per lavoratori più giovani. Tali schemi aggravano il problema già esistente in Italia dovuto all’invecchiamento della popolazione in quanto accelerano la contrazione della popolazione in età lavorativa. Le persone con lavori usuranti dovrebbero tuttavia essere protetti da un aumento dell’età pensionabile.

4. In che modo un salario minimo può creare posti di lavoro di qualità e buone condizioni di lavoro?

L’Italia ha molti salari minimi

specifici legati agli accordi collettivi di contrattazione. Un salario minimo

generale proteggerebbe i lavoratori meno qualificati in settori nei quali i

lavoratori hanno scarso potere contrattuale e ridurrebbe il rischio di povertà

lavorativa, che ha continuato a crescere in Italia durante la ripresa.

Il salario minimo dovrebbe essere

fissato ad un livello tale da non scoraggiare l’assunzione di lavoratori

scarsamente qualificati; inoltre dovrebbe riflettere le differenze di

produttività tra le regioni.

Inoltre, il livello del salario minimo dovrebbe essere deciso e rivisto mediante un processo trasparente e basato su considerazioni obiettive riguardanti il mercato del lavoro. Per proteggere i lavoratori a basso reddito e rendere il lavoro più remunerativo, il Rapporto OCSE consiglia di introdurre sussidi ai lavoratori a basso salario.

5. Che cosa consiglia il Rapporto sui flussi migratori?

Il potenziale contributo degli

immigrati all’economia e alla società italiana è enorme. Per garantire il

sostegno e l’accordo degli Italiani, sono essenziali politiche e dibattitti sui

temi migratori ben gestiti e basati su evidenze empiriche. È anche importante

garantire che gli immigrati possano accedere a corsi di formazione, in modo che

l’Italia tragga beneficio dalle capacità, dall’imprenditoria e dal dinamismo

che gli immigrati apportano.

L’emigrazione dall’Italia è aumentata notevolmente dall’inizio della crisi, specialmente tra i giovani. Ciò è una minaccia per la sostenibilità della crescita e lo standard di vita dell’intera popolazione. Politiche mirate a migliorare le prospettive di lavoro e i salari aumenteranno l’attrattività dell’Italia come luogo dove vivere e lavorare. Ciò contribuirà anche all’arrivo di immigrati qualificati dall’Europa e da altre parti del mondo.

6. Come può l’Italia diventare meno vulnerabile all’aumento dei tassi d’interesse?

Progettare e seguire una politica

fiscale credibile migliorerebbe la credibilità fiscale e abbasserebbe

ulteriormente i rischi di rifinanziamento del debito pubblico.

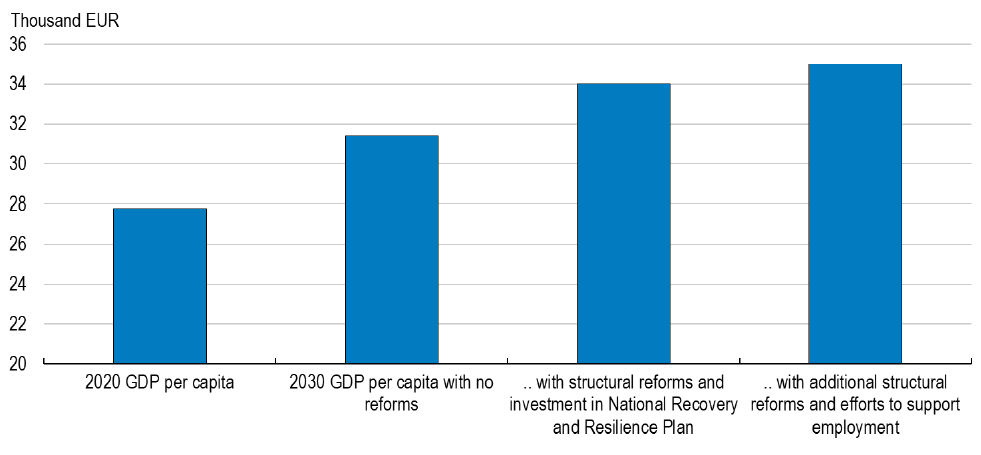

Attuando riforme strutturali e aumentando l’avanzo primario, il debito pubblico dell’Italia si avvierebbe su una traiettoria discendente. Ciò diminuirebbe il pagamento di interessi sul debito pubblico e libererebbe risorse per finanziare investimenti, che sono tanto necessari, e combattere la povertà e l’esclusione sociale.

7. Quanto sono vulnerabili le banche italiane?

Il settore bancario gode di una salute

molto migliore rispetto al 2017 quando è stato pubblicato il precedente Rapporto

OCSE sull’Italia:

- Lo stock di crediti in sofferenza sui

bilanci bancari è diminuito drasticamente e continua a ridursi.

- Gli interventi del governo nel sistema

bancario sono stati efficaci e sono costati molto meno che in altri paesi.

Ma c’è ancora molto da fare per

garantire che le banche possano continuare a sostenere le imprese, in

particolare le piccole imprese:

- La riduzione delle sofferenze è stata

più lenta per le banche di piccole e medie dimensioni.

- La riforma delle banche popolari e

cooperative è progredita, ma deve ancora essere pienamente attuata.

- Mantenere bassi i rendimenti dei titoli

di Stato salvaguarderà la stabilità delle banche e la loro capacità di fornire

credito.

8. Quali sono le previsioni economiche dell’OCSE per l’Italia?

La ripresa graduale dell’Italia si è

arrestata alla fine del 2018. Il Rapporto prevede una riduzione del PIL dello

0,2% nel 2019, prima di crescere dello 0,5% nel 2020. Ciò riflette in gran

parte il forte rallentamento verificatosi nel 2018 quando l’economia italiana

si è contratta dello 0,6% nel terzo trimestre e lo 0,4% nel quarto. L’OCSE prevede

che l’economia ricomincerà a crescere entro il secondo trimestre del 2019.

Il rallentamento dell’economia ha

riguardato le principali componenti della domanda, comportando una minore

crescita delle esportazioni, dei consumi privati e degli investimenti a causa

del rallentamento dei principali partner commerciali (in particolare la

Germania) e dell’incertezza riguardante le politiche economiche. Oltre

all’andamento ciclico sfavorevole, l’Italia continua a soffrire di una bassa

crescita potenziale, stimata tra lo 0 e lo 0,5% all’anno. Questo spiega anche

perché il tasso di crescita previsto per l’Italia sia inferiore rispetto quello

di molti altri paesi. Mentre gli altri “paesi starnutiscono, l’Italia prende la

febbre”.

La revisione al ribasso della crescita prevista per PIL aumenterà il disavanzo pubblico pronosticato dal 2,1% del PIL nel 2018 al 2,5% nel 2019. La differenza nelle previsioni di crescita spiega la maggior parte del divario tra le proiezioni del disavanzo presentate nel Rapporto sull’Italia e quelle del governo (2% del PIL nel 2019).

9. Come è stato preparato il Rapporto OCSE sull’Italia?

L’Italia è membro fondatore dell’OCSE,

che da oltre 50 anni lavora a stretto contatto con i governi italiani per

fornire suggerimenti e raccomandazioni di politica economica e sociale e

condividere buone prassi.

I Rapporti OCSE sono pubblicazioni

biennali che esaminano le tendenze e le performances economiche dei vari paesi

e forniscono raccomandazioni di “policy” in vari ambiti al fine di aumentare la

crescita e il benessere sociale. Tutti i paesi membri dell’OCSE e alcuni paesi

non membri sono soggetti a questo esercizio di monitoraggio.

Tutte i Rapporti OCSE sui paesi sono preparati dal Dipartimento di Economia dell’OCSE in collaborazione con le altre direzioni più specializzate. I Rapporti sono esaminati dai rappresentanti dei governi degli Stati membri dell’OCSE, riuniti nel Economic Development Review Committee (EDRC), compreso il paese in esame. L’EDRC è al centro del meccanismo di “peer review” dell’OCSE, il quale offre ai rappresentanti di tutti i 36 governi membri dell’OCSE e alla Commissione europea l’opportunità di scambiare opinioni su politiche economiche e le migliori prassi da applicare in vari contesti. Il Dipartimento di Economia rivede la bozza del Rapporto sulla base dei commenti ricevuti dall’EDRC. I delegati dell’EDRC approvano quindi la versione finale per la pubblicazione, garantendo un ampio consenso.

Questo processo consente un proficuo scambio di opinioni e la condivisione di esperienze tra governi, per migliorare le rispettive politiche economiche e sociali. Il prossimo Rapporto sull’Italia è previsto per il 2021.

* Il Rapporto non tiene pienamente conto di tutte le regole di attuazione del Reddito di Cittadinanza in quanto sono state definite solo di recente (Legge 26/2019). Alcune delle norme di attuazione incoraggiano l’assunzione dei percettori del Reddito di Cittadinanza, come il sussidio alle imprese che assumono lavoratori utilizzando i centri per l’impiego, altri lo scoraggiano, come la possibilità di rifiutare legittimamente offerte di lavoro con un salario inferiore al Reddito di Cittadinanza (per un singola persona) maggiorato del 10%.

Bibliografia

OECD (2019), OECD Economic Surveys: Italy 2019, OECD Publishing, Paris.

It is common knowledge that – among other things – low productivity is one of the main causes of the poor performance of the Italian economy. Red tape, the relatively limited openness to competitiveness of some professional services, the tax burden, the limited size of SMEs, and the need to improve secondary education and the efficiency of the judicial system are – among other factors – affecting our ability to grow the economy.

It is common knowledge that – among other things – low productivity is one of the main causes of the poor performance of the Italian economy. Red tape, the relatively limited openness to competitiveness of some professional services, the tax burden, the limited size of SMEs, and the need to improve secondary education and the efficiency of the judicial system are – among other factors – affecting our ability to grow the economy.