New OECD long-run scenarios focus on the trade-off between carbon mitigation and climate damage

Category: Climate,Environment,Uncategorized

written by oecdecoscope | September 8, 2025

by Yvan Guillemette, OECD.

Last week the OECD released the latest update of its long-term scenarios, which are designed to quantify some of the most important long-term macroeconomic trends and policy challenges facing the global economy. One central challenge is the need to accelerate the transition toward renewable energy sources to reduce greenhouse gas emissions and attenuate the impacts of climate change. How this might impact future output trajectories is the focus of this update.

The analysis considers two “business-as-usual” scenarios in which decarbonisation of the energy mix and improvements in energy efficiency continue along recent trends. The first is based on a median climate damage curve and the second on a high climate damage curve within the wide range found in the scientific literature. In the scenario with a median climate damage curve (scenario BAU1), global annual potential output growth is projected to moderate gradually from around 2.9% today to 2.7% in the first part of the 2030s, 2.1% in the early 2040s and remain at around 1.3% in the second half of the century. This moderation reflects declining working-age population growth and slowing trend labour efficiency growth in the emerging-market economies as their productivity levels get gradually closer to the frontier. China remains the world’s largest economy until the mid-2060s when it is surpassed by India.

Global annual potential output per capita growth slows by less than overall output, but still declines from about 2% today to 1¼ per cent by 2050, remaining broadly stable thereafter.

Insufficiently rapid progress on reducing greenhouse gas emissions implies continued global warming. The global average surface temperature anomaly – the increase in the global average temperature since pre-industrial times – continues to increase throughout the projection period and reaches 2½ °C in 2100. The reduction in global output associated with climate change, estimated to be approximately 1¾ per cent of global GDP today, rises to nearly 9% by 2100. With a steeper climate damage curve, at the high end of recent estimates, projected climate damages reduce global output by 36% by 2100 (scenario BAU2).

An illustration of the potential impacts of an accelerated energy transition on future output must consider two main impact channels. The first is faster carbon mitigation. This is a negative supply shock in the short to medium run (relative to a business-as-usual scenario), with the size varying across countries according to their current energy mixes and ease of substitutability. The second is the avoidance of climate-related damages, a positive supply shock in the medium to long run (again, relative to a business-as-usual scenario) that is also country specific. To highlight the uncertainty surrounding these channels, four energy transition scenarios are considered with differing assumptions about the pace at which carbon mitigation costs might decline over time and the steepness of the global climate damage curve.

With a median climate damage curve and a slow decline in mitigation costs (scenario ET1), global output remains lower in 2100 than in the corresponding business-as-usual scenario.

With a median climate damage curve and a quick decline in mitigation costs (scenario ET2), the energy transition becomes a net positive for global output around 2085.

With a high-damage curve and a slow decline in mitigation costs (scenario ET3), the energy transition becomes a net positive for global output in the mid-2050s.

With a high-damage curve and a quick decline in mitigation costs (scenario ET4), the energy transition becomes a net positive for global output in the mid-2040s. All 139 countries modelled individually are net beneficiaries by 2080.

The new long-term scenarios also incorporate several key improvements to the underlying projection framework: 1) the geographical coverage is now global, including 139 countries modelled individually; 2) the projection horizon has been extended from 2060 to 2100; 3) the approach for long-run productivity convergence across countries has been revised; and 4) the framework now allows for the impact of climate damages on output via a global climate damage curve and country-specific climate sensitivities that can be altered to consider different assumptions and scenarios.

Selected series for the scenarios are available on the OECD Data Explorer and additional data visualizations are available on this web page.

A heated issue: The unequal impacts of climate change and climate change mitigation

Category: Climate,Environment,Uncategorized

written by oecdecoscope | September 8, 2025

by Jule Hodok.

The direct impacts of climate change are unevenly distributed across countries, regions, and socioeconomic groups. Inaction will not only result in significant macroeconomic costs but also deepen existing inequalities (Intergovernmental Panel on Climate Change (IPCC), 2023). However, climate mitigation policies designed to reduce the emission of greenhouse gases (GHGs) also have distributional effects. A new report by the OECD Economics department reviews the distributional consequences of climate change and climate change mitigation as well as illustrates the trade-offs between equity, efficiency, and effectiveness in the design of climate policies.

Unequal impacts of climate change

The extent to which a specific group of people, regions and countries are affected by climate change is determined by their exposure and vulnerability:

“Exposure” is the presence of people, livelihoods, species, or ecosystems in places and settings that could be adversely affected by environmental degradation.

“Vulnerability” is the tendency to suffer from the adverse effects and/or the lack of capacity to cope or adapt after exposure to climate change (Intergovernmental Panel on Climate Change (IPCC), 2023).

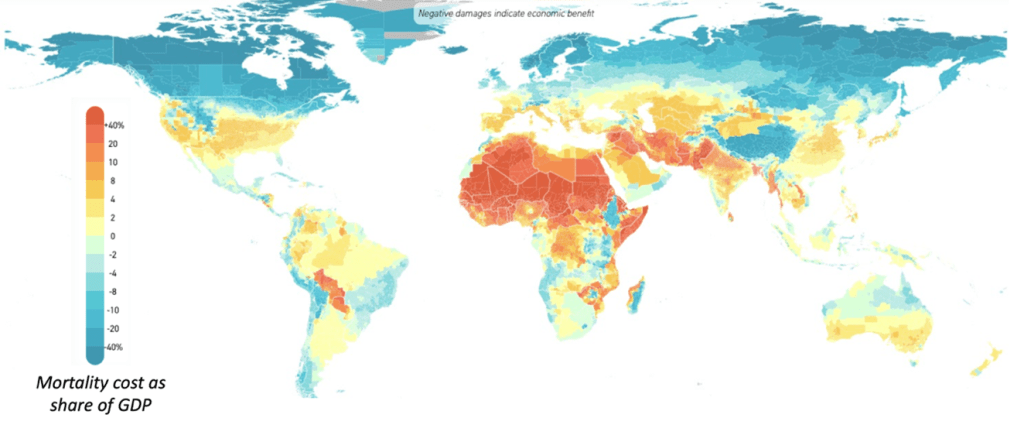

Developing countries are on average more exposed to climate change due to a combination of factors, such as often higher baseline temperatures, higher likelihood of droughts, and the reliance on climate-sensitive sectors, such as agriculture which is highly affected by temperature and precipitation levels (IPCC, 2023). They are also more vulnerable due to lower levels of adaptive capacity and resilience (Bilal & Känzig, 2024; Frankhauser, 2017) (Figure 1).

Figure 1. Predicted mortality cost as a share of GDP under a high emissions scenario

Notes: Estimates are based on a high emission scenario (RCP 8.5) for the end of the century (2080-2099). The methodology for estimating the mortality costs of climate change (temperature-related) derived from (Carleton, et al., 2022). Mortality costs are just one part of health-related impacts of climate change and account for an even smaller share of the overall costs of climate change. Source: (Climate impact Lab, 2024)

Within countries, drawing clear, general conclusions of the impact of climate change is more difficult. Still, for example, urban areas often face higher risks of extreme temperatures and flooding (Frankhauser & McDermott, 2016), while rural communities tend to be more vulnerable due to a stronger reliance on resource-based industries (OECD, 2021). Evidence also suggests that lower-income households tend to be disproportionately affected, as they often lack the resources to adapt to climate change, e.g. by not being able to afford adaptive technologies, or lower access to quality healthcare and insurance (Bijnens, et al., 2024; Islam & Winkel, 2017).

The distributional impacts of climate change mitigation

While mitigating climate change can, over the longer term, help alleviate some of the distributional concerns related to the direct impacts of climate change, climate policies themselves have distributional consequences, from both an income and consumption perspective.

From an employment and income perspective, the climate transition will trigger a reallocation of labour and capital, from “high-emission” sectors, firms, and activities to low carbon emitters. For example, research estimates that in response to a global tax of USD 50/tCO2, fossil fuel industries – which tend not to be large employers overall – would experience a decrease in employment and output, while the largest job gains would occur in low-carbon power generation (Chateau, Bibas & Lanzi, 2018) (see Figure 2 for an overview of sector-specific effects). However, as high-emission industries tend to be regionally clustered, such labour market effects are likely geographically concentrated, potentially widening regional inequalities within countries (OECD, 2021; OECD, 2023). Additionally, low-skilled workers and those with lower educational attainment are often most negatively affected as they tend to face higher barriers to reskilling and job mobility (OECD, 2023; Chateau, Bibas, & Lanzi, 2018).

Figure 2. Change in output, employment, and gross wage by sector in response to central scenario

Notes: a carbon tax of USD 50/tCO2 is applied in all regions of the world; percentage change w.r.t reference equilibrium, 2011; OECD ENV-Linkages computable general equilibrium (CGE) is used as a tool for the analysis. Source: (Chateau, Bibas, & Lanzi, 2018)

From a consumption perspective, policies that result in changes in relative prices will affect households differently if they have different consumption patterns. Four key findings emerge based on the review of existing literature:

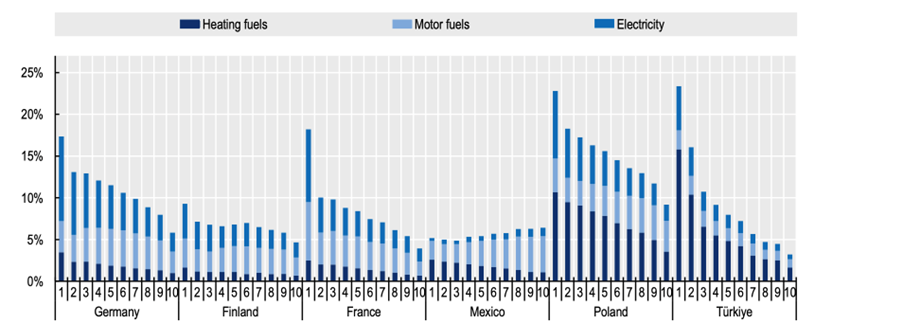

In advanced economies, carbon and energy taxation is mostly regressive (Flues & Thomas, 2015; Douenne, 2020; Immervoll et al., 2023). The regressivity often stems from the fact that food and some fuels are a necessity for many households making poorer households unable to reduce their consumption in response to higher prices (Figure 3) (Vandyck et al., 2023; Elgouacem, et al., 2024).

In developing countries, carbon and energy taxation often are progressive. This stems from the fact that a large subset of the population has low incomes and relatively limited fossil fuel energy use. Developing countries are therefore particularly confronted with the trade-off between energy affordability and addressing climate change as even a small increase in the price of energy may significantly aggravate energy poverty (Dorband et al., 2019; Steckel, et al., 2021).

The regressivity of policies depends on the specific policy in question and the type of fuel that is targeted. For example, transport fuel taxation is neutral in countries with higher GDP per capita and progressive in countries with lower GDP per capita (Flues & Thomas, 2015; Missbach et al., 2024). Additionally, other factors than income drive distributional effects. For example, most evidence shows that rural households are more vulnerable to carbon taxation, due to limited access to public transport (Causa et al., 2022).

Non-market-based policies – including bans, standards, and direct regulation – tend to disproportionately affect lower-income households and may result in equity concerns through possibly unaffordable replacement costs of the emission-intensive good (Elgouacem, et al., 2024). Limited research on subsidies and feed-in-tariffs (e.g. for electric vehicles, solar panels, or home insulation) suggests that they tend to primarily benefit higher-income households who have the required capital to invest in the low-carbon solution (Borenstein & Davis, 2016; Levinson, 2019).

Figure 3. Household expenditures on fuel and other energy, by income decile

Note: Groups 1-10 refer to income deciles. Domestic fuel includes expenditure on gas, liquified hydrocarbons, kerosene, and other liquid fuels, coal, and other solid fuels. Motor fuels includes expenditure on diesel and petrol for transportation. Source: (Elgouacem, et al., 2024), (Screenshot, Figure 5.5 in paper)

Overall, integrating equity and fairness considerations in the design of climate policies and broader climate strategies can help manage their distributional impacts and improve the social acceptability of a climate transition.

References

Bijnens, G., Anyfantaki, S., Colciago, A., De Mulder, J., Falck, E., Labhard, V., . . . Strobel, J. (2024). The Impact of Climate Change and Policies on Productivity. SSRN Electronic Journal. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4741442

Bilal, A., & Känzig, D. (2024). The Macroeconomic Impact of Climate Change: Global vs. Local Temperature. National Bureau of Economic Research, Cambridge, MA. doi:10.3386/w32450 https://www.nber.org/papers/w32450

Dorband, I., Jakob, M., Kalkuhl, M., & Steckel, J. (2019). Poverty and distributional effects of carbon pricing in low- and middle-income countries – A global comparative analysis. World Development, 115, 246-257. doi:10.1016/j.worlddev.2018.11.015 https://www.sciencedirect.com/science/article/pii/S0305750X18304212

Levinson, A. (2019). Energy Efficiency Standards Are More Regressive Than Energy Taxes: Theory and Evidence. Journal of the Association of Evironmental and Resource Economists, 6(S1), S7-S36. doi:10.1086/701186. https://www.journals.uchicago.edu/doi/full/10.1086/701186

Steckel, J., Dorband, I., Montrone, L., Ward, H., Missbach, L., Hafner, F., . . . Renner, S. (2021). Distributional impacts of carbon pricing in developing Asia. Nature Sustainability, 4(11), 1005- 1014. doi:10.1038/s41893-021-00758-8 https://www.nature.com/articles/s41893-021-00758-8

Vandyck, T., Della Valle, N., Temursho, U., & Weitzel, M. (2023). EU climate action through an energy poverty lens. Scientific Reports, 13(1). doi:10.1038/s41598-023-32705-2 https://www.nature.com/articles/s41598-023-32705-2

Reconciling housing and the environment: is it possible, and how?

Category: Environment,Housing

written by oecdecoscope | September 8, 2025

By Grace Alexander, Ioannis Tikoudis, Katherine Farrow and Walid Oueslati, OECD Environment Directorate

Ensuring widespread access to affordable housing constitutes a significant policy challenge in many countries. Increasing housing costs in urban areas push many to live in less accessible locations and to lower their living standards. This can reduce wellbeing, undermine social cohesion and eventually jeopardize political stability. At the same time, another policy challenge, equally urgent and multifaceted, emerges from climate change and environmental degradation in urban areas. The cost that climate change, air pollution and biodiversity loss impose on modern societies is significant: health, food systems and infrastructure are all affected, and the consequences will only grow if these issues are left unaddressed. Are the housing and environmental crises somehow interrelated? Do governments have the relevant tools to pursue affordability and environmental sustainability at the same time?

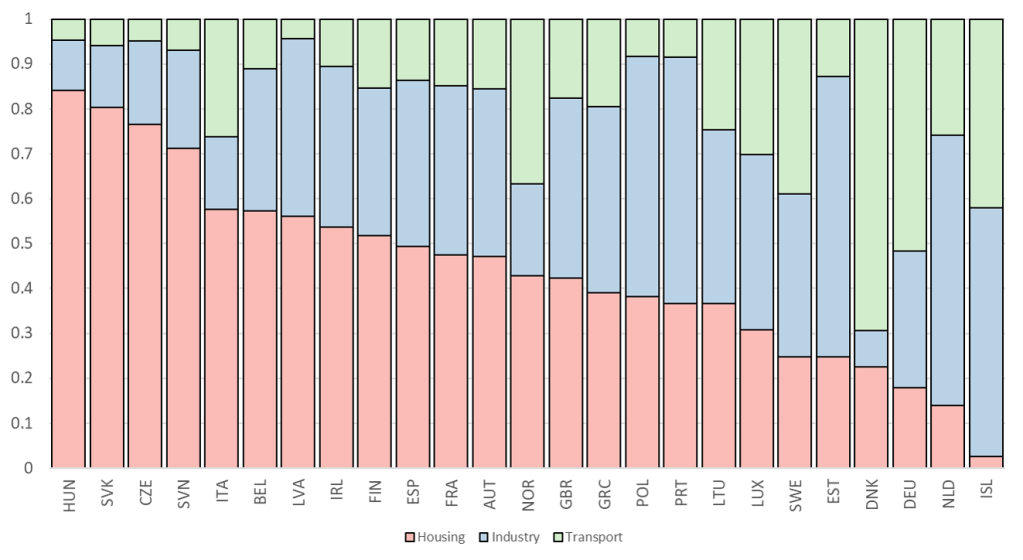

How we build our urban areas affects housing markets and comes with certain environmental costs. The residential sector accounts for a large share of fine particulate matter (Figure 1), an air pollutant associated with severe health impacts, with the sector responsible for 37% of the emissions of fine particulate matter globally. Limits on building height and density, applied widely around the world, reduce housing supply and contribute to observed house price surges. Similar regulations cause cities to spread outwards, causing irreversible changes on the natural areas surrounding cities and generating more greenhouse gas emissions per capita. The phenomenon of rapid suburban expansion, which has come to be known as urban sprawl, possessed tremendous momentum for decades and continues to be a focal issue in urban development today. Sprawled cities imply greater travel distances, make residents more dependent on their cars and tend to increase the cost of providing public transport services (OECD 2018).

Figure 1. Housing accounts for a large share of fine particulate matter

Source: Air emission accounts, OECD Environment Database

Reconciling housing and the environment, published in the OECD report “Brick by Brick”, provides an anatomy of such practices, and their long run social cost. The chapter explores ways to build our urban areas by balancing housing affordability and environmental quality. It is not only that housing policies affect the environment, the chapter reports, but also that urban environmental policies can have a significant impact on our house values. Reducing pollution and increasing green spaces increase the value of nearby housing stock. Although energy efficiency regulations may increase construction costs, they also add value to homes that are subject to such regulations. Importantly, the value that environmental regulations can add to the existing housing stock should not be confused with the rise in house prices caused by mechanisms causing artificial scarcity, such as regulatory constraints on housing supply.

Ultimately, the homes that we live in and the environment around us are crucial to our health and wellbeing. By considering the effect of the residential sector on the environment, and vice versa, the chapter outlines how we may be able to strike a sustainable balance between the two.

OECD (2021), Reconciling Housing and the Environment., Brick by Brick: Building Better Housing Policies, OECD Publishing, Paris, https://doi.org/10.1787/96aaa66a-en

President Biden pledges an ambitious climate strategy

Category: Environment,United States

written by oecdecoscope | September 8, 2025

By Patrick Lenain, OECD Economics Department

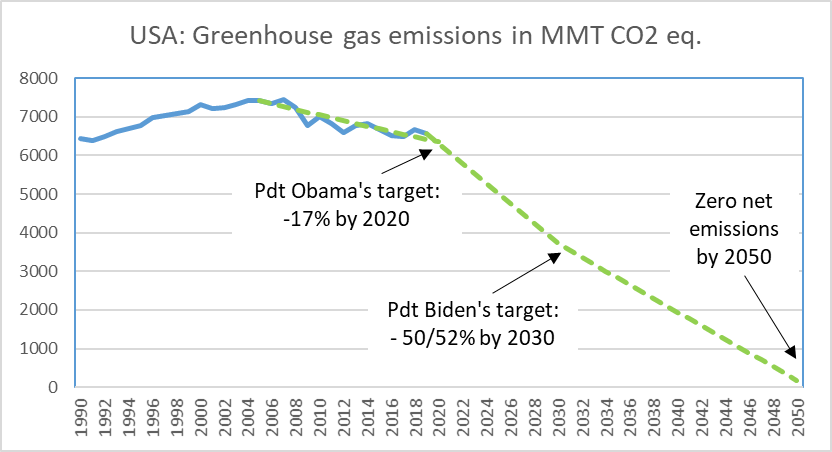

Ten years ago, the OECD published an in-depth analysis of U.S. greenhouse gas emissions (GHG) and urged the country to reverse gears (Carey, 2010). The analysis welcomed President Obama’s pledge in Copenhagen to cut the country’s emissions by 17% in 2020 from 2005 levels, but found that this would require new policy measures. As we approach the new climate summit in Glasgow (COP26), the United States can display progress: according to the latest data released by the Environment Protection Agency, GHG emissions have declined and President Obama’s target is within reach (Figure 1). President Biden has now pledged further progress with a target to cut GHG emissions by at least half in 2030 and achieve zero net emissions no later than 2050. These targets will imply to bend the curve and accelerate the pace of emission cuts.

Figure 1: A faster pace of emission reductions is required

Note: When published, 2020 data will show a sharp decline of emissions caused by the COVID19 recession, but emissions are likely to rebound in 2021 with the recovery of activity. Source: Environmental Protection Agency.

The United States has already achieved a welcome reduction in GHG emissions. At first glance, this seems surprising after policy changes made during the Trump Administration such as the repeal of the Clean Air Act, subsidies favouring fossil fuels, and curbs on state-level regulatory standards. The reasons for this progress is that a lot has happened in the energy market, at the subnational level, and with tax credits:

Electricity production has been gradually decarbonised thanks to the decline of coal, the rise of natural gas, and the emergence of renewable energy sources such as wind turbines and photovoltaic panels (Figure 2), which have been encouraged by subsidies and regulation.

Cap-and-trade carbon markets have encouraged this energy transformation at the regional level. The Regional Greenhouse Gas Initiative (RGGI) is an agreement between nine states that aim at curbing CO2 emissions in the electric power sector. RGGI helped to reduce emissions in 2020 by 47% relative to 2005 in these states. California and Quebec have also joined forces and maintain a multi-sector cap-and-trade market.

Several tax credits already encourage households, firms, and utilities to use clean energy and improve their energy efficiency: an investment tax credit partially pays for the cost of installing photovoltaic solar panels; a plug-in electric vehicle tax credit helps buyers of new electric vehicles; a producer tax credit subsidizes the use of renewable energy sources.

Many other policy interventions seek to curb emissions at the federal level (e.g. financial support to research in renewable energy), state level (e.g. California’s vehicle emission rules) and city level (e.g. Seattle’s ban of combustion engine cars by 2030). In addition, many U.S. firms have made net zero emission pledges, and financial institutions have plans to withdraw funding to the fossil fuel industry.

Figure 2: Coal is no longer favoured in electricity production

Source: OurWorldinData based on BP and Ember.

Despite past progress, much remains to be done in the United States, like in many other countries, to limit the rise in global temperature. The United States still emits the largest amounts of GHG and CO2 per capita among G20 countries, together with Australia and Canada. The effective pricing of energy-related carbon emissions in the United States is among the lowest in G20 and OECD countries: only 22% of these emissions are priced at €60 per ton of CO2 or more, the level considered as the minimum to reach the Paris climate targets (OECD, 2021a).

High energy prices are often favoured in terms of cost efficiency, but they would have a regressive impact on income distribution and are politically challenging. President Biden has therefore announced alternative measures to lower GHG emissions:

Tax credits will be further increased to decarbonise electricity production and encourage energy efficiency. Such tax credits can act like carbon taxes because they reduce the cost of renewable energy relative to fossil fuels. However, their impact is limited to specific sectors, unlike economy-wide carbon taxes, and their fiscal impact is negative because they reduce government tax revenue.

The purchase of plug-in electric carswill be encouraged by tax credits and public investment in battery recharging stations. Ownership of electric vehicles in the United States is one of the lowest in the OECD and G20 and the Administration plans to catch up with other countries.

More public investment will help the green transition. Investment will strengthen the nation’s electricity grid, and financial support will target the energy efficiency of buildings.

President Biden’s plans are a big step forward toward a low carbon future. The measures will help to decarbonise electricity generation and transportation, but questions remain about other large emitting sectors, especially industry and agriculture (Figure 3).

Figure 3: Transportation and electricity sectors are large GHG emitters, 2019

Source: Environmental Protection Agency.

References:

Carey, D. (2010), “Implementing Cost-Effective Policies in the United States to Mitigate Climate Change”, OECD Economics Department Working Papers, No. 807, OECD Publishing, Paris, https://doi.org/10.1787/5km5zrs4kc6l-en.

OECD (2021a), Effective Carbon Rates, Pricing Carbon Emissions through Taxes and Emissions Trading.

OECD (2021b, forthcoming), Assessing the economic impacts of environmental policies – Evidence from a decade of OECD research, OECD Publishing.

“Every breath you take”: Reducing exposure to environmental health risks in Poland

Category: Environment,Poland

written by oecdecoscope | September 8, 2025

by Paula Adamczyk, Priscilla Fialho, Antoine Goujard, OECD Economics Department

The COVID-19 crisis has spotlighted Poland’s environmental challenges, notably the heavy air pollution at which the Polish population is exposed, as it makes individuals more vulnerable to acute respiratory illnesses and to the ongoing sanitary crisis. As the government prepares its recovery plan to revive the economy in the aftermath of COVID-19, there is a unique opportunity to bring forward needed public investments into clean energy projects. “Green” investment projects would not only stimulate employment and aggregate demand, but also make growth more sustainable in the longer-term. The newly agreed “Next Generation EU” recovery plan will have dedicated funds to support the transition to climate neutrality and Poland should grasp the opportunity to enhance the resilience of its economy and society. The newly published 2020 OECD Economic Survey of Poland provides some advice on policies that could help supporting the transition to a greener and fairer economy.

Poland has made little progress to improve air quality. In many cities and regions, the level of atmospheric pollution remains well above the limits established in the European Union Air Quality Directive: an alarming 36 out of 50 most polluted European cities are located in Poland. The population exposure to fine particles is among the highest in the OECD (Figure 1), which causes a variety of adverse health outcomes and premature deaths (WHO, 2019).

CEEC is the average of Hungary and the Czech and Slovak Republics. Source: OECD (2020), OECD Green Growth Indicators (database).

The residential sector is responsible for high air pollution and levels of energy consumption. The burning of poor-quality coal, wood, or even waste, in old boilers used to heat individual houses is the main contributor for the high level of particulate matter in the air. The incomplete combustion of solid fuel in low-efficiency stoves and lamps used for cooking and lighting also releases a significant amount of fine particles. Moreover, a large share of the existing residential and commercial buildings date back from before 1990 and have poor thermal insulation. As a result, space heating requires a significant amount of energy and there is a lot of heat loss through the building envelope. In fact, the energy intensity of space heating in Poland is one of the highest among European Union (EU) countries.

The transport sector is another key driver of air pollution. In 2018, the average vehicle age in Poland was 14 years, compared to 11 years in the European Union. That same year, 80% of passenger cars in Poland’s roads were more than 10 years old (European Commission, 2019). The average CO2 emissions from new passenger cars sold in Poland are among the highest in Europe. In 2019, only 0.5% of newly registered passenger cars were electric vehicles, compared to an average of 3.6% in the European Union (International Council on Clean Transportation, 2020). Polish authorities have set welcome and ambitious targets to increase the fleet of electric vehicles in the coming years. These targets should be met. In June this year, the government made efforts in that sense and introduced Poland’s first fiscal incentive programme for the purchase of cleaner cars.

Progress to decarbonise electricity production in Poland has also stalled over the past few years. Coal still accounts for around 78% of gross electricity generation, compared to about 25%, on average, in other Visegrád countries and the OECD. Furthermore, most Polish coal-fired power plants are over 25 years old. The industry lags behind in terms of production efficiency and in the adoption of new technologies that could reduce the emission of pollutants.Coal mining is another source of air pollution as it releases fine particles in the air, such as dust, soot and smoke, which can be carried to nearby towns by the wind. Despite all the environmental challenges implied, Poland is still one of the largest coal producer in the world. The authorities have recently agreed to phase out coal mining by 2049, but plan to continue subsidising coal production until then (European Council for an Energy Efficient Economy, 2020).

Polish authorities need to step-up their efforts to improve air quality and reduce the health risks associated with ambient air pollution. The latest OECD Economic Survey of Poland establishes three policy priorities that can boost Poland’s transition to a greener economy and, in particular, bring the country on the path to meeting higher air quality standards:

Support building renovation to improve energy performance in the residential sector.

Two years ago, the government introduced a programme to offer means-tested financial grants and loans for the replacement of obsolete stoves and for thermal retrofits to single-family houses. However, the take-up rate has been far much lower than anticipated. Complex application procedures and low income-threshold for the highest grants have been pointed as possible reasons for the low take-up.

Polish authorities could consider extending nationwide the recently introduced anti-smog regulations in some regions (“voivodeships”) that aim at limiting the burning of fossil fuels in furnaces, as well as introducing fines for noncompliance. Continuing to simplify the administrative procedures associated with the loans and grants for replacing old heating and cooking equipment as well as easing access for low-income households would help to increase take-up. Expanding the use of smart meters would also contribute to reduce the energy consumption of the residential sector. Finally, improving the energy standards for new buildings (e.g. more stringent building energy codes, additional performance-based requirements or more demanding energy performance certificates) and imposing minimum requirements for the creation of reserve funds in multi-flat buildings dedicated to building renovation and thermal insulation, could significantly improve buildings’ energy efficiency.

Increase the effective tax carbon rate and the pricing of environmental externalities.

Tax rates on energy use in the residential sector and the electricity excise tax are low for international standards. Furthermore, there are several exemptions from energy taxes, such as from the tax on coal in the agricultural sector, from the tax on coal for households’ consumption, and from the coal and gas excise duties in some energy-intensive industries. Poland is also one of the very few OECD countries without a specific CO2-related vehicle tax and diesel is still taxed at a lower rate than petrol. Overall, this results in low carbon prices on road and non-road GHG emissions (Figure 2).

To encourage the takeup of greener technologies, the government should progressively phase out exemptions to energy taxes and gradually increase explicit carbon taxes, while using the generated revenues to support the transition of low-income households towards greener technologies and increase social adhesion.

Improve the regulatory environment surrounding the production and distribution of renewable energy.

Stringent regulation prevents the use of larger and more efficient turbines to generate electricity from onshore wind. The development of offshore wind, on the other hand, is held back by low energy transmission capacity, especially in the northern part of Poland. Frequent changes in regulations create a lot of uncertainty and reduce incentives for private investment in renewable energies.

A stable regulatory environment and further incentives to develop alternative sources of energy would help to reduce the reliance on coal for energy production. The renewable energy sector can quickly absorb capital investments and generate employment in both construction and manufacturing.

The global economy is facing unprecedented uncertainty as the evolution of the Covid-19 pandemic weighs heavily on the economic outlook. Nine months after the initial outbreak in Wuhan, it is still difficult to predict the path of the virus. Each country has been hit in a different way, and response strategies have varied. There is much we still do not know. Research for a vaccine is ongoing across the globe, but more needs to be done to prepare for mass-scale testing, manufacturing and distribution that will be required. It seems clear today that we will have to live with the virus for some time, with our principal defence being tigher hygiene standards and physical distancing measures.

Amid this unprecedented uncertainty, what we know is that the world will be much poorer than it would have been without the virus. If our central projection of a gradual recovery, after the rebound, materialises, global income will be USD 7 trillion lower by the end of 2021 than what we projected less than a year ago in November 2019. This is roughly equivalent to losing a year’s production from France and Germany combined.

The initial economic shock in the first part of 2020 was deep and profound. In the wake of national confinements, the global economy plunged 7.8% in the second quarter of this year, an unprecedented drop in peace time. The decline would have been harder had governments not put in place a wide safety net for firms and individuals. As economies began to reopen, activities that could operate with physical distancing rebounded strongly. But it would be imprudent to infer from this that the recovery is V-shaped and global income can rapidly return to pre-crisis levels. In some industries a rapid recovery will occur; those linked to digital activity for example, but others will not be able to fully recover for some time. Scheduled flights are still down around 50% on a year ago in September. Entertainment and tourism have been deeply affected. Overall, 13-20% of OECD employment is threatened.

Because developments are so varied across countries and uncertainty is so high, we have produced two scenarios around our central projection. On the upside, if businesses and households were to become more confident because a vaccine or treatment is in sight or only mild containment measures were required to contain virus outbreaks, world growth would be stronger (figure). The loss of global output would be around USD4 trillion by the end of 2021. On the downside, if confidence remains weak because outbreaks were to intensify or stricter containment measures were required, household spending and business investment would weaken and the recovery would slow, and the loss in output would be USD11 trillion.

Even if this crisis is strikingly different from others we have experienced and uncertainty is extremely high, we have seen that policy matters. In the confinement phase of the Covid-19 crisis, policymakers worldwide used a rich policy toolbox. These measures included short-term working schemes, furloughed employment, credit or grants to firms and tax holidays. This is pushing debt up by around 15 percentage points of GDP across the OECD, but was necessary, and will remain so for 2021. Central banks provided liquidity support, and low rates kept debt interest payments at lower levels.

Policy will continue to play an important role in the next phase of the crisis. We learnt from the aftermath of the Global Financial Crisis that tightening fiscal policy prematurely could impart a serious blow to an already weakened economy. Fiscal support will have to continue. We also learnt that policy can only temporarily prevent a rise in bankruptcies and unemployment. Support to firms must evolve to let non-viable firms go and encourage viable ones to grow. Equity instruments could be deployed for large firms, with state support, provided competition is preserved and a clear strategy for exit designed. However, it will require more creativity for SMEs, for example in the form of tax credits, with repayments occuring when firms sustainably return to profit.

Individuals in vulnerable sectors also need policy support.For sectors where the shock is seen as temporary, short-term working schemes may continue, with more flexibility to allow people to take on new activity. For other sectors, existing schemes to support individuals and firms need to be tailored to avoid maintaining support to unviable jobs and firms that blocks reallocation necessary for a strong and persistent recovery. Training and job placement should be supported by digital infrastructure and be tailor-made to individuals as a norm. Policymakers need to make an extra-effort to be sure support reaches those who need it most. Furthermore, the first phase of the crisis has shown that barriers to trade can be hugely disruptive for an efficient supply of goods and services. International cooperation must resume to ensure health goods and services can be delivered to all, but also that trade barriers do not rise further putting some firms and activities, and the associated jobs, at risk.

Looking further ahead, there is no way today to predict how people will behave after 18 months of a pandemic, how they will work and undertake leisure activities. We can sketch out how some trends will accelerate though. First, there will be a wider use of teleworking, although the limits of out-of-office work must be taken into consideration. Second, we will see more services move online and increased online retail sales. Third, there will be greater demand, and need, for crisis management preparation, including health, cybersecurity, energy security and protection against natural disasters. Fourth, as the crisis impacts more precarious workers, the essential workers who cannot telework, those living in crowded accomodation, those in poor health, public demand for greater access to essential goods and services including public health and education provision should prevail. Amid a background of public disapproval with the evolution of inequality, policies will need to improve on transparency, increasing competition and reducing collusion, and finding the means for a more efficient delivery of public services.

Policymakers have to aim higher than trying to restore our pre-pandemic living standards: they need to deal with pre-crisis trends that threaten our future and seize the opportunity for change. It is an opportunity to implement green recovery and a significant shift in the sustainability of our economies. Governments are spending a lot of money in the policy response to the pandemic, but not enough of this is focused on sustainable solutions. Some countries are taking measures, but the effort needs to be bolder. Still, over 50% of policy support for energy in recovery packages is going to ‘brown’ fossil fuels. As recovery plans will be at the heart of governments budget preparation for 2021, the opportunity to reboot the economy on a stronger, fairer and more sustainable footing should not be wasted.

Green swans: climate change risks, central banking and financial stability

Category: Environment,finance

written by oecdecoscope | September 8, 2025

by Luiz Awazu Pereira da Silva, Bank of International Settlements, drafted by Shashwat Koirala, OECD Economics Department

The Chief Economist Talks are part of the OECD’s high-level distinguished speaker series in which global economic leaders, top thinkers and decision makers are invited to discuss their perspectives on the world economy with the OECD Chief Economist. The talks aim to foster learning and inspiration and provoke meaningful discussions. Previous speakers have included: Claudio Borio (BIS), Peter Praet (ECB), Maurice Obstfeld (IMF), Penny Goldberg (World Bank), Debora Revoltella (EIB), Hal Varian (Google), Sergei Guriev (EBRD), Stefanie Stantcheva (Harvard), Emmanuel Moulin (Ministry of Economy and Finance, France), Philipp Steinberg (Ministry of Economic Affairs and Energy, Germany), and Jean Pisani-Ferry and George Papakonstantinou (EUI). Participation in these events are by invitation only and are aimed at OECD staff and the OECD Ambassadors and delegations. They are not open to the press.

The unprecedented challenge posed by climate change is well documented. The rising concentration of greenhouse gases in the atmosphere has profound environmental impacts (e.g. rising sea levels, extreme temperature events, etc.) that threaten the delicate balance of the planet’s natural systems. The human and societal consequences of the climate emergency are also massive, as environmental damages can exacerbate inequalities, food and water insecurity, and conflicts. Accounting for climate-related risks is, thus, indispensable for building resilient socio-economic-ecological systems.

There is an emerging recognition among central banks and financial regulators that climate-related risks are also a source of price and financial instability, and that there is a need to safeguard the financial system against these risks. This is complicated by a paradoxical tension between physical climate risks and transition risks. For example, on one hand, inaction towards the climate crisis means that climate-related accidents become more frequent and severe, threatening socio-economic systems and financial stability (i.e. physical risks). On the other hand, a rapid and aggressive decarbonisation effort can lead to sudden asset repricing (i.e. transition risks). This tension epitomises the fact that climate-related risks are transmitted through complex and inter-connected channels and have cascade effects. Treating these risks requires a departure from status quo thinking, as outlined by the following four key ideas.

First, while similar in some respects to “black swans”– highly unexpected events with severe far-reaching consequences (e.g. 2008 U.S. housing market crash) that can be best explained ex post – climate-related risks are distinct. They are not tail-risk events; scientific evidence suggests that climate-related shocks are virtually certain to occur, though the exact timing of these events is uncertain. Since the climate crisis poses an existential threat to humanity, climate-related risks are also more catastrophic than traditional systemic financial risks. Finally, as alluded to earlier, climate-related risks are much more complex. They are propagated non-linearly with destructive feedback loops and can cascade across sectors, countries and systems (see Figure 1 for a representation of chain reactions stemming from climate-related risks). Taking inspiration from the “black swan” moniker, climate-related events are termed “green swans”.

Second, a methodological shift in macroeconomic-climate modelling is required to better understand green swan events, and how they emerge, accumulate and cascade. Backward-looking and deterministic approaches (e.g. vector autoregressive models) that extrapolate historical trends do not suffice in capturing the complexity and radical uncertainty of climate-risks. Even current scenario-based forward-looking risks assessment mechanisms are unable to completely incorporate the broad range of chain-reactions associated with climate change. This, in tandem with the fact that these approaches lack granularity and there is uncertainty regarding approaches to climate-change mitigation, means that the current paradigm of models cannot fully elucidate the potential macroeconomic, sectoral and firm-level repercussions of climate change. Thus, an exploration of alternative approaches is needed, such as non-equilibrium models (instead of more sophisticated dynamic stochastic general equilibrium models), sensitivity analysis with more complex scenarios, and studies specific to countries, sectors and firms.

Third, given the intrinsic complexity of climate change, international co-ordination and co-operation is vital. While central banks play a critical role in mitigating climate-related risks, they do not possess a silver bullet to do so by themselves. Central banks and financial regulators have a role to play in identifying and managing climate-risks (e.g. integrating risks into prudential regulation), internalising externalities (e.g. incorporating environmental, social and governance considerations into their own portfolios), and enabling structural low-carbon transitions (e.g. reforming the international monetary and financial system). Nevertheless, many tools, such as green fiscal policy and carbon pricing, fall outside their purview, and uncoordinated actions from central banks would be insufficient and could potentially have unintended consequences. A systems-wide green transition necessitates buy-in and action from all stakeholders (i.e. governments, private sector, and civil society), and central banks need to contribute to coordinate on climate change by being more proactive on this front while continuing to fulfil their financial stability mandate.

Fourth, it is important to acknowledge that green swans have a tremendous negative redistributive impact, within and between countries. Not only do the physical risks stemming from climate change predominately affect lower-income countries, but also the costs of adaptation to climate-change (e.g. shift away from carbon-intensive industries) are higher for poorer households. This means that addressing climate change requires scaled-up mechanisms for redistribution and a redesign of societal safety nets and efforts to finance the green transition of low-income countries. Otherwise, a society-wide acceptance of actions on climate change will prove elusive.

The ecological and environmental stability of the planet is a prerequisite for price and financial stability. So, for central banks to fulfil their central mandate, they have an important role in contributing to a systems-wide climate-change effort. In a nutshell, this involves identifying and communicating the risks ahead, calling for bold actions from all stakeholders to ensure the resilience of the earth’s socio-ecological systems, and helping manage the risks within the bounds of their mandate.

Bibliography

Bolton, P., Despres, M., Pereira da Silva, L. A., Samana, F., & Svartzman, R. (2020). The green swan: Central banking and financial stability in the age of climate change. Bank for International Settlements.

Carbon tax, emissions reduction and employment: Some evidence from France

Category: Environment,France,Uncategorized

written by oecdecoscope | September 8, 2025

by Damien Dussaux, Economist, OECD Environment Directorate

To ensure this target is met, the French government developed a “National Low Carbon Strategy”, which acts as a roadmap for implementing a low-emission transition in each sector of the economy. For example, GHG emissions from industry account for almost one fifth of emissions in France, equivalent to total GHG emissions of Romania, and, under the proposed sectoral plan, will be reduced by a quarter within the next ten years.

France is currently employing two main carbon pricing mechanisms:

A carbon tax on fossil fuel consumption, starting at 7 euros per tonne of CO2 and now amounting to 45 euros per tonne, in place since 2014.

These increasingly stringent carbon pricing policies have taken place in a period of rising industrial energy costs generating concerns about their impact on the competitiveness of the manufacturing sector. At first glance, such concerns appear to be borne out. Recent trends show real output and total employment in the sector decreased by 5% and 26%, respectively, between 2001 and 2016.

However, a recent OECD report, shed another light on this issue. This study is the first to estimate the impact of energy prices and carbon taxes on the environmental and economic performance using data at the firm and industry level.

What does the OECD study tell us?

At the firm level, a 10% increase in energy costs results in a 6% decline in energy use, a 9% decrease in carbon emissions, and a 2% decrease in the number of full-time employees within one year. However, these jobs are not lost, but are reallocated to other firms.

At the industry level, there is no statistical link between energy prices and net job creation, indicating that jobs lost at affected firms are compensated by increases in employment in other firms operating in the same sector during the same year.

These effects vary both between industries and according to the size of the firm and their energy intensity: For example,

When facing the same increase in the energy cost, firms in the wearing apparel industry reduces their carbon emissions twice as much as firms producing non-metallic minerals.

Reallocation of workers in the food products industry is half the reallocation in the basic metals industry.

On average, large and energy intensive firms experience greater reduction in carbon emissions and greater job reallocation than smaller and energy efficient firms.

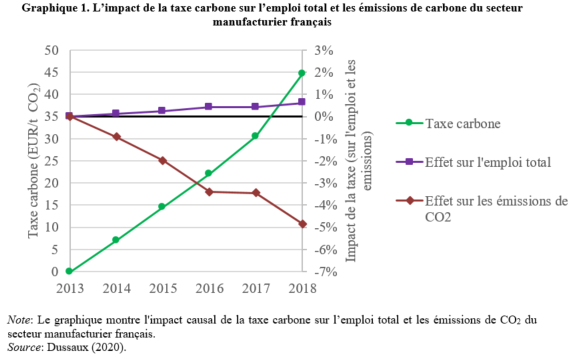

With this, the paper is able to measure the causal effect of the carbon tax on the aggregate manufacturing sector since its introduction in 2014. Figure 1 plots the carbon tax on the left axis (green line) together with the impacts of the carbon tax on the French manufacturing sector’s jobs (purple line) and carbon emissions (red line) on the right axis. In five years, the carbon tax decreased carbon emissions by 5%. The net effect on employment is much smaller in magnitude and even slightly positive at +0.8%.

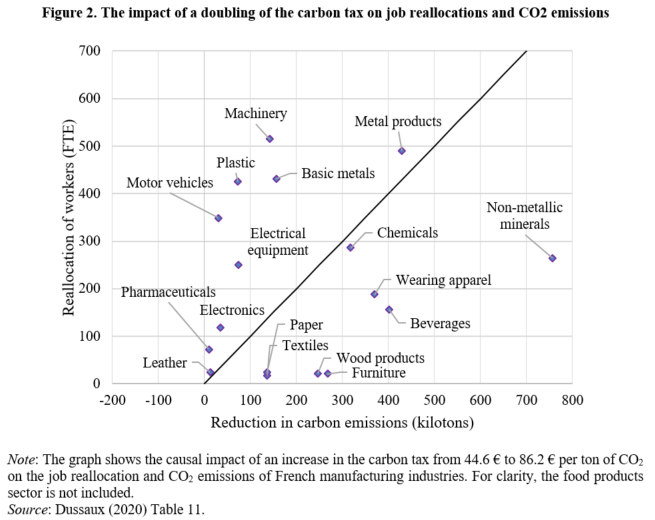

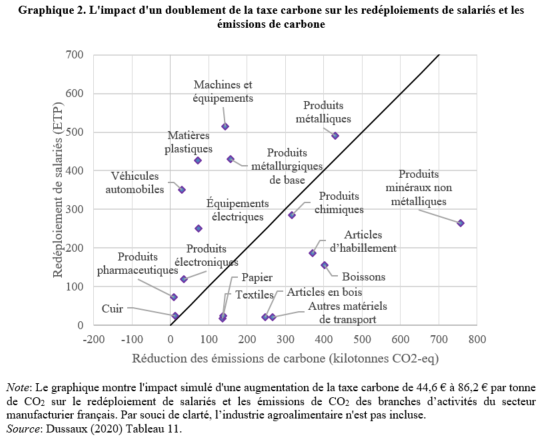

Finally, the paper considers a scenario where the carbon tax is doubled from its current rate of 45 € per tonne of CO2. Figure 2 shows the simulated effect of the tax increase on job reallocations and carbon emissions for each manufacturing industry. These job reallocations are not net job losses, but the number of people forced to change jobs (within the same industry or between industries).

A simulated doubling of the carbon tax highlights significant heterogeneity across sectors. Several industries such as furniture, wood products, paper, and textiles experience large reductions in carbon emissions with little job reallocation. On the contrary, the motor vehicles and the plastic industries experience larger job reallocations and smaller declines in carbon emissions. Other industries such as metal products experience large job reallocation and emissions reduction because of their size.

Higher energy prices and carbon taxes are effective at reducing carbon emissions, but costs of job reallocation must be considered…

Although the carbon tax enables the French manufacturing sector to meet its carbon budget and does not affect total employment negatively, it however generates non-negligible job reallocations in several industries. Because these reallocation effects have redistributive implications and generate costs for workers who are forced to change jobs, these results call for complementary labour market policies that minimise those costs on affected workers and ease between-firms adjustments in employment. Moreover, since these transition costs are typically highly localised in regions specialised in polluting activities, they can also translate into potentially significant regional effects and thus political costs.

References:

Dussaux, D. (2020), “The joint effects of energy prices and carbon taxes on environmental and economic performance: Evidence from the French manufacturing sector”, OECD Environment Working Papers, No. 154, OECD Publishing, Paris, https://doi.org/10.1787/b84b1b7d-en.

Taxe carbone : quel impact environnemental et économique dans le secteur manufacturier français ?

Category: Environment,France,Posts in French

written by oecdecoscope | September 8, 2025

par Damien Dussaux, Economist, Direction de l’environnement, OCDE

Afin d’atteindre cet objectif, le gouvernement français a élaboré une “Stratégie Nationale Bas-Carbone”, qui sert de feuille de route pour la transition vers de faibles émissions de carbone dans chaque secteur de l’économie. Par exemple, les émissions de GES de l’industrie – qui représentent près d’un cinquième des émissions en France, soit l’équivalent des émissions totales de GES de la Roumanie – devront être réduites d’un quart au cours des dix prochaines années selon le plan sectoriel proposé.

La France met actuellement en œuvre deux principaux mécanismes de tarification du carbone afin d’inciter les acteurs économiques à réduire leurs émissions. Le système européen d’échange de quotas d’émission (SEQE-UE), en place depuis 2005, couvre 75 % des émissions industrielles françaises. En 2014, la France a également introduit une taxe carbone sur la consommation de combustibles fossiles, qui a débuté à 7 euros par tonne de CO2 et s’élève désormais à 45 euros par tonne.

Ces politiques de tarification du carbone de plus en plus ambitieuses ont été mises en place dans un contexte de hausse des coûts énergétiques dans l’industrie et suscitent des inquiétudes quant à leurs impacts sur la compétitivité du secteur manufacturier français. À première vue, ces préoccupations semblent être justifiées par les tendances récentes, puisque la production et l’emploi total dans le secteur ont diminué respectivement de 5 % et 26 % entre 2001 et 2016.

Le rapport combine des données sur la consommation d’énergie et les émissions de carbone au niveau des entreprises provenant de l’enquête annuelle sur la consommation d’énergie dans l’industrie (EACEI) de l’Insee avec les données sur les performances financières et économiques de la Direction Générale des Finances Publiques. L’ensemble des données couvre 8 000 entreprises françaises observées annuellement sur une période de seize ans (2001 à 2016) et qui sont représentatives de l’ensemble du secteur manufacturier.

Que nous apprend l’étude de l’OCDE ?

Le premier enseignement de l’étude est qu’au niveau des entreprises, une augmentation de 10 % des coûts énergétiques entraîne à court terme une baisse de 6 % de la consommation d’énergie, une diminution de 9 % des émissions de carbone et une diminution de 2 % du nombre d’employés à temps plein. Toutefois, ces emplois ne sont pas détruits car les salariés concernés sont embauchés dans d’autres entreprises. Au niveau de l’industrie, l’étude ne trouve aucun lien statistique entre les prix de l’énergie et la destruction nette d’emplois, ce qui indique que les emplois détruits dans les entreprises touchées sont compensés par des embauches dans d’autres entreprises de la même branche d’activité au cours de la même année.

Deuxièmement, ces effets varient d’une industrie à l’autre et en fonction de la taille et de l’intensité énergétique des entreprises. Par exemple, face à une même augmentation du coût de l’énergie, les entreprises de l’industrie de l’habillement réduisent leurs émissions de carbone deux fois plus que les entreprises produisant des minéraux non métalliques. Le redéploiement des travailleurs dans l’industrie agroalimentaire est deux fois moins important que dans l’industrie métallurgique. En moyenne, les grandes entreprises à forte intensité énergétique réduisent davantage leurs émissions de carbone et redéployent davantage de salariés que les petites entreprises efficaces en énergie.

Le rapport est ainsi en mesure de quantifier l’effet causal de la taxe carbone sur le secteur manufacturier depuis son introduction en 2014. La Graphique 1 montre la taxe carbone sur l’axe de gauche (ligne verte) ainsi que les impacts de la taxe carbone sur l’emploi total du secteur manufacturier français (ligne violette) et ses émissions de carbone (ligne rouge) sur l’axe de droite. En cinq ans, la taxe carbone a permis de réduire les émissions de carbone d’environ 5 %. L’effet net sur l’emploi est beaucoup plus faible et même légèrement positif à +0,8 %.

Enfin, le rapport envisage un scénario dans lequel le taux de la taxe sur le carbone serait doublé par rapport à son taux actuel de 45 € par tonne de CO2. Le Graphique 2 montre l’effet simulé de l’augmentation de la taxe sur les redéploiements de salariés et les émissions de carbone pour chaque branche d’activité. Ces redéploiements de salariés ne sont pas des pertes nettes d’emplois, mais le nombre de personnes contraintes de changer d’emploi (au sein d’une même industrie ou entre industries).

La simulation du doublement du taux de la taxe carbone met en évidence une grande hétérogénéité entre les branches d’activités. Plusieurs secteurs, tels que l’ameublement, les produits du bois, le papier et le textile, connaissent de fortes réductions de leurs émissions de carbone, avec un faible redéploiement de salariés. Au contraire, les secteurs de l’automobile et du plastique connaissent des redéploiements de salariés plus importants et des diminutions plus faibles de leurs émissions de carbone. D’autres industries, telle que celle des produits métalliques, combinent une forte réaffectation des emplois et une réduction considérable des émissions en raison de leur taille importante.

La hausse des prix de l’énergie et de la taxe carbone permet de réduire les émissions de carbone, mais les coûts liés aux redéploiements de salariés doivent être pris en compte…

Si la taxe carbone permet au secteur manufacturier français de respecter son budget carbone et n’affecte pas négativement l’emploi total, elle génère cependant des redéploiements de salariés non négligeables dans plusieurs branches d’activité. Parce que ces redéploiements ont des impacts redistributifs et génèrent des coûts pour les travailleurs qui sont contraints de changer d’emploi, ces résultats mettent en évidence la nécessité de mettre en place des politiques complémentaires sur le marché du travail qui minimisent les coûts pour les travailleurs concernés et facilitent les ajustements en termes d’emplois entre les entreprises. En outre, comme ces coûts de transition sont généralement fortement localisés dans des régions spécialisées dans les activités industrielles énergivores, ils peuvent également se traduire par des effets régionaux potentiellement importants et donc par un coût politique élevé.

Référence:

Dussaux, D. (2020), “Les effets conjugués des prix de l’énergie et de la taxe carbone sur la performance économique et environnementale des entreprises françaises du secteur manufacturier”, OECD, No. 154, OECD Publishing, Paris, https://doi.org/10.1787/b8ca827a-fr.

Pollution Havens – just a delusion?

Category: Environment,Green growth,trade

written by oecdecoscope | September 8, 2025

by Christina Timiliotis, Junior Trade Policy Analyst, OECD Trade & Agriculture Directorate, and Tomasz Kozluk, Head of the Green Growth Workstream, OECD Economics Department

Governments in the OECD and elsewhere must intensify efforts to mitigate pollution levels, if the international agreement of the latest COP 21 – pledging to keep global warming below 2 degrees – is to be more than just a loose promise. Against this background, policy makers need to enforce environmental regulations that oblige firms to account for the impact their actions have on the environment, and increase the price of using the environment as a factor of production. While there is broad support for environmental goals in the first place, support dwindles when compliance with such regulations implies higher production costs.

Efforts to put a cost on pollution have indeed often provoked resentment and resistance by producers and workers who fear to be put at a disadvantage vis-à-vis foreign competitors that are located in jurisdictions with laxer environmental policies. The conventional wisdom that tougher environmental regulations ultimately entail a loss in competitiveness and thus encourage industries to relocate production to a more favorable business environment, is commonly referred to as the “Pollution Haven Hypothesis” (PHH). If real, it can make environmental policy making politically difficult due to voters resistance and ineffective due to leakage. However, in spite of the PHH’s popularity, the evidence behind it is fragmented and to a large extent anecdotal.

Scrutinising data across more and less pollution intensive industries in 23 OECD countries and six emerging economies since the 1990s, we find that countries with relatively stringent environmental laws do not suffer from lower exports as a result (see compare your country data viz) . There is however, a small effect on their relative competitiveness across different sectors in the economy. In countries with more stringent policies, exports of pollution and energy intensive sectors, such as steel-making or chemicals are lower than in the absence of stringent environmental policies (Figure 1). However, this is compensated by a corresponding increase in exports in “cleaner” industries like machinery or electronics. Moreover, both the positive and negative effects of environmental regulations on exports of different sectors have been small so far relative to the effects of other factors, such as market size, globalisation, national endowments or trade liberalisation.

Increase in domestic value added in exports 1995-2008, USD billions

Note: The figure shows exports from the three most stringent countries (Denmark, Germany, Switzerland) to BRIICS and vice versa, in billions USD. Pollution intensive sectors are defined according to methodology described in Kozluk and Timiliotis as ISIC rev. 3.1. 2325: Manufacture of coke, refined petroleum products and nuclear fuel; Manufacture of chemicals and chemical products; Manufacture of rubber and plastics products and 2000: Manufacture of wood and of products of wood and cork, except furniture; manufacture of articles of straw and plaiting materials. Less pollution intensive sectors are defined as 2933: Manufacture of machinery and equipment n.e.c.; Manufacture of office, accounting and computing machinery; Manufacture of electrical machinery and apparatus n.e.c.; Manufacture of radio, television and communication equipment and apparatus; Manufacture of medical, precision and optical instruments, watches and clocks; 3637: Manufacture of furniture; manufacturing n.e.c.; Recycling.

In its preface to the General Theory, Keynes said that “the difficulty lies not so much in developing new ideas as in escaping old ones.” A myriad of ideas on how to credibly reduce the incentives to pollute in the long-term already exists. It remains to escape the archaic belief that ensuring environmental protection while maintaining a strong market position is infeasible. Governments must stand up to the environmental challenge and focus on the good design of environmental policies, accompanying framework policies and on the edge they can get from innovation – in order to secure both good environmental and economic outcomes.