Positive economic outlook for the main economies in Latin America but downward risks have intensified

Alvaro S. Pereira (Director) and Latin American desks, Economics Department, Country Studies Branch, OECD

The global economy is navigating rough seas. Global GDP growth is strong but it has peaked. In many countries unemployment is well below pre-crisis levels, labour shortages are biting and inflation remains tepid. Yet, global trade and investment have been slowing on the back of increases in bilateral tariffs while many emerging market economies are experiencing capital outflows and a weakening of their currencies. The global economy looks set for a soft landing, with global GDP growth projected to slow from 3.7% in 2018 to 3.5% in 2019-20. However, downside risks abound and policy makers will have to steer their economies carefully towards sustainable, albeit slower, GDP growth.

The economic recovery in the Latin American economies has become dissimilar. While in some countries, growth has been revised downwards, in others it has been revised upwards. This disparity is closely linked to how these economies have evolved in the face of the financial stress and increased financial volatility in recent months. The region’s economies with the best macroeconomic fundamentals, independent central banks, countercyclical monetary policies, sound fiscal policy framework and no major currency mismatches in corporate or sovereign debt, were better able to sail the adverse global financial conditions that led to capital outflows, weakening their currencies.

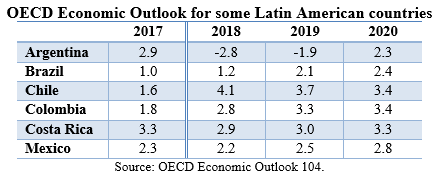

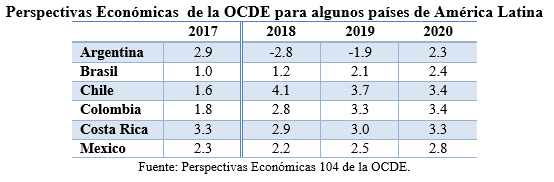

While Chile and Colombia have gained momentum, Brazil has shown lower growth and Argentina has fallen into recession. Mexico and Costa Rica have also experienced less momentum than expected. Growth in Argentina, Brazil, Chile, Colombia, Costa Rica and Mexico, countries covering about 85% of Latin America’s GDP, is expected to be around 1.4% this year and to accelerate to 2.0% in 2019 and 2.7% in 2020 (weighted average) (see Table). However, downside risks abound while the region is vulnerable to the global context. Several indicators, such as the fiscal and current account deficits have been accentuated in the last decade in most of these economies (Figure), suggesting that the region is still vulnerable. Needs to be noted that the situation is uneven and a broader list of indicators should be analysed.

An accumulation of risks could create the conditions for a harder-than-expected landing. First, further trade tensions would take a toll on trade and GDP growth, generating even more uncertainty for business plans and investment. Second, tightening financial conditions could accelerate capital outflows from the region and depress demand further. Third, a sharp slowdown in China would hit Latin America and other emerging economies, but also advanced economies if the demand shock in China triggered a significant decline in global equity prices and higher global risk premia.

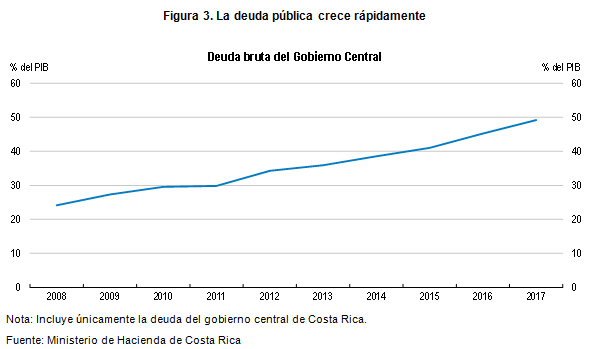

Looking ahead, it will be necessary to strengthen the macroeconomic policy framework to reduce vulnerabilities where necessary. Most of the region’s economies are starting, or will start in the near future, more restrictive monetary policies, while also undertaking fiscal consolidation. Depending on each country, it will be important to find a balance between the needs for social spending and public investment, with the need to put debt on a sustainable path. In Chile, Colombia and Mexico, this consolidation can be done gradually, but Argentina, Brazil and Costa Rica need to do it more urgently. Pension or tax reforms will be necessary in this regard.

Given the limited scope for countercyclical policies, in the face of external risks and a more pronounced slowdown, the time to promote the necessary structural reforms is now to guarantee a future with a sustained increase in productivity and greater inclusion. Many countries in the region have scope to reform the tax system and make it more effective in improving investment incentives and raising more resources. Depending on the characteristics of each country, possible measures may include limiting the use of tax exemptions and reduced rates, particularly in VAT, but also in corporate taxes, extending the tax base by including more people in personal income taxes, reducing evasion or making greater use of property, inheritance or environmental taxes. Other priorities should focus on export promotion and diversification, which would help reduce current account deficits. Investing in quality and innovative human capital, closing infrastructure and logistical gaps, and curbing corruption would support exports and their diversification, strengthening growth. Encouraging women’s participation in the labour force, reducing precariousness and informality in the labour market, as well as pension reforms are also urgent in several countries of the region and necessary to increase productivity and reduce inequalities.

Argentina: A combination of massive fiscal and monetary tightening will keep the economy in recession during 2018 and 2019. Private consumption and investment will remain depressed due to lower real incomes and high interest rates, and unemployment will rise. However, a better harvest and a lower real exchange rate will support stronger exports.

Brazil: Growth will gain momentum during 2019 and 2020 as private consumption, supported by improvements in the labour market, will increase. Recovering credit and greater policy certainty as a new administration takes office will buttress the recovery. Political uncertainty around the implementation of reforms remains significant and could derail the recovery, but if uncertainty fades and reforms advance as assumed, investment will become stronger.

Chile: Growth is projected to remain strong over the next two years. With an uncertain external environment, solid domestic demand will underpin growth, aided by a stable inflation environment, public infrastructure projects and a tax reform. Inequality, though decreasing, remains high, as informality and unemployment remain high and social transfers low.

Colombia: Growth is projected to pick up as infrastructure projects, lower corporate taxes and higher oil prices will boost investment. Improving confidence and financing conditions will support consumption. As growth gains traction, unemployment will edge down. Social indicators are improving but informality and inequality remain high.

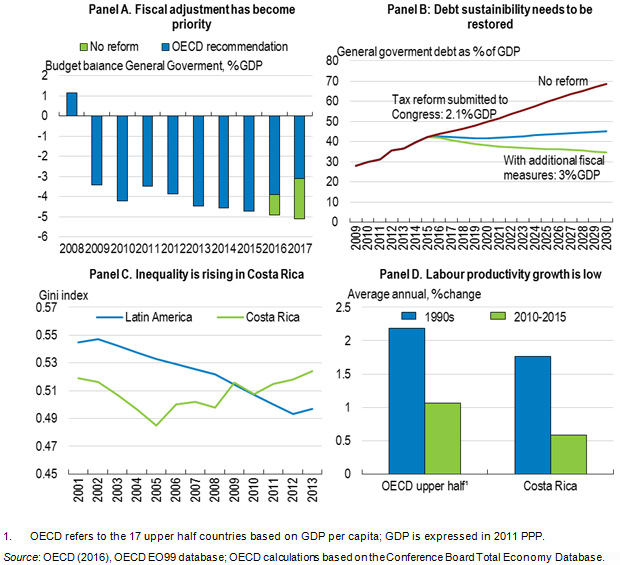

Costa Rica: Growth is projected to recover to around 3¼ per cent in 2020 and be broad-based, underpinned by both domestic and external demand. However, uncertainty, particularly surrounding the planned fiscal reforms, is weighing on growth in the near term. The projections are based on the assumption that the fiscal reforms will be implemented from 2019, with modest fiscal tightening holding back growth in 2019 and 2020.

Mexico: Growth is projected to pick up to 2¾ per cent in 2020. Low unemployment, strong remittances and the recovery of real wages will support household consumption. Investment, which has been persistently low, will strengthen on the back of announced public investment plans and increased confidence associated with the US-Mexico-Canada trade agreement. Exports will decelerate owing to less favourable global conditions, especially in the United States. Inflation has been pushed up by rising energy prices, but expectations and core inflation remain anchored and within the central bank’s target band. Informality is slowly declining but remains elevated, contributing to persistently high inequalities and low productivity.

To read more about the Economic Outlook and the main structural challenges visit the english and spanish/portuguese version (it includes OECD forecasts and a chapter on decoupling of wages and productivity and the implications for public policy).

References:

OECD (2018), OECD Economic Outlook, Volume 2018 Issue 2: Preliminary version, OECD Publishing, Paris, https://doi.org/10.1787/eco_outlook-v2018-2-en.

Por Sonia Araujo y Lisa Meehan, Sección de Costa Rica, Departamento de Economía de la OCDE

Por Sonia Araujo y Lisa Meehan, Sección de Costa Rica, Departamento de Economía de la OCDE