Boosting business sector productivity in Canada

Katja Schmidt & Gilles Thirion, OECD.

Canada’s economy has shown resilience to crisis, including the recent Covid19-crisis. However, growth in per capita GDP has lagged in recent years. Business investment per worker in Canada has remained significantly below that of peer OECD countries, particularly in key areas such as information and communication technology (ICT), machinery and equipment, and intellectual property products. Moreover, the business innovation intensity remains comparatively low, despite the availability of various government support programmes. As a result, productivity growth has remained subdued (Figure 1). Between 2015 and 2023, labour productivity per hour worked grew by just 0.8% annually, below the OECD average and significantly behind the United States.

The Canadian economy is now facing new headwinds in the form of rising tariffs from its most important trading partner, the US. The effective tariff rate on US imports from Canada is expected to rise by about 13 percentage points, up from a near-zero effective bilateral tariff rate. Although the tariff exemptions under the United States-Mexico-Canada Agreement will help shield the Canadian economy from more severe impacts, the tariffs will still significantly weigh on economic growth. They could also further undermine productivity growth. However, if tariffs help to prompt structural reforms, particularly those weighing on productivity, this could help mitigate some of the negative effects of tariffs in the long-term.

In this context, the new 2025 OECD Economic Survey of Canada highlights four key priorities to strengthen business sector productivity:

- Reduce interprovincial barriers to trade and labour mobility to strengthen the efficiency and integration of the internal market;

- Enhance competition and support firm growth by removing remaining regulatory restrictions in network sectors, improving access to financing for young and innovative firms, and reinforcing competition policy;

- Scale up and streamline government innovation support schemes to increase accessibility;

- Ensure full utilisation of skills by addressing labour market mismatches, reducing underemployment, and improving pathways for credential recognition and upskilling.

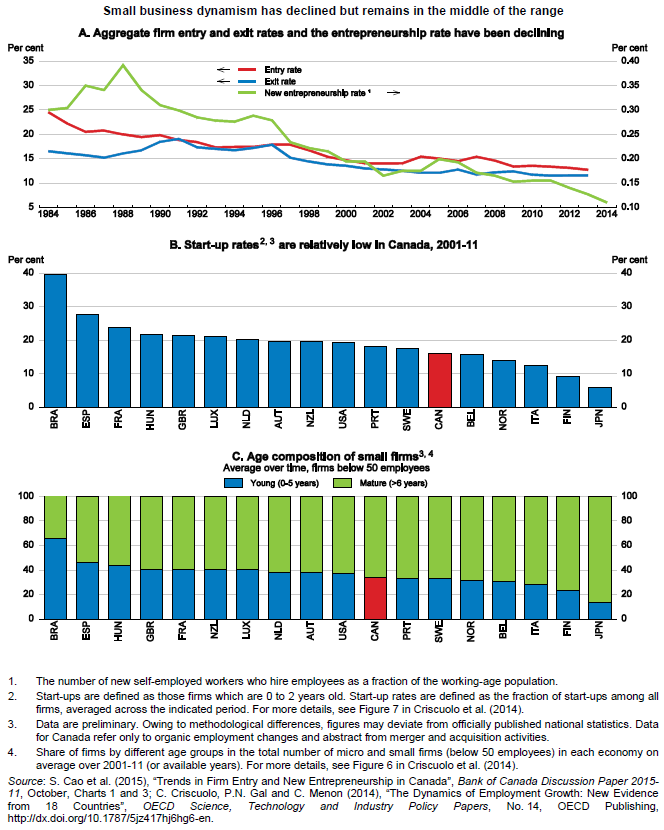

Canada’s interprovincial trade barriers have been widely recognised as undermining the efficient allocation of resources across the country and effectively reducing the size and integration of its internal market. These barriers span a range of areas, including occupational licensing, transportation and procurement regulations, and divergent technical standards. Accelerating the reduction of these barriers, such as by expanding the scope and enforcement powers of the Canadian Free Trade Agreement, would enhance market efficiency, foster competition, and support productivity growth.

Interprovincial barriers also constrain labour mobility, particularly in skilled trades and professional services. Differences in provincial certification requirements continue to hinder mutual recognition, limiting the ability of workers to move freely. Policy efforts should focus on further harmonising standards and expanding mutual recognition frameworks across provinces.

Policies to enhance competition and business dynamism span multiple policy domains. One possible area of reform is the removal of existing foreign entry restriction in some key network sectors, such as telecommunications. Another area is to support the growth of small and medium-sized enterprise (SME), which struggle to scale. Addressing this requires different tools, such as reviewing the preferential small business corporate tax rate; improving access to affordable financing; and strengthening managerial capabilities. In addition, ensuring a robust competition policy framework in digital markets is essential to foster innovation

Third, existing government support programmes for business innovation should be better coordinated and simplified, to increase Canada’s comparatively low business R&D spending (Figure 2). R&D incentives should be harmonised across small, medium-sized, and large firms to ensure neutrality. Additionally, there is scope to reallocate public R&D funding towards some more direct support instruments, which tend to be more targeted. The proposed Canada Innovation Corporation (CIC), envisioned as a new nationwide platform for supporting business R&D, represents a promising step toward streamlining and enhancing the effectiveness of R&D incentives.

Finally, the Survey highlights opportunities to better harness the potential of Canada’s highly educated labour force, notably by better integrating immigrants and enhancing female participation. Overqualification remains prevalent among immigrants. Expanding mutual recognition agreements for foreign qualifications could help mitigate the risk of skill underutilisation of immigrants. In addition, women continue to be under-represented in some key technical fields and leadership positions. Policy efforts should focus on continuing expanding access to affordable childcare, promoting equal parental leave, enforcing pay equity, and supporting flexible work arrangements.

Visit the OECD’s Canada Economic Snapshot page for further information.

References:

OECD (2025), OECD Economic Surveys: Canada 2025, https://doi.org/10.1787/28f9e02c-en, OECD Publishing, Paris.